Swiss Franc saw a significant rebound in European session, driven by stronger-than-expected inflation figures for April. Despite this upside surprise, inflation remained within SNB’s target range of 0-2% for the eleventh consecutive month. Currently, economists are still largely anticipating a further 25 basis point rate cut by SNB in June, which would adjust the policy rate to a more neutral level of 1.25%. However, these expectations could be subject to change should inflation figures for May indicate acceleration again.

Meanwhile, Japanese Yen continues to dominate as the strongest currency for the week, bolstered by significant spikes on Monday and Wednesday. Despite Japan’s top currency diplomat Masato Kanda refraining from confirming any market interventions, reports suggest that as much as JPY 3.5T may have been deployed in market operations on Wednesday. This speculation has solidified 160 mark as a firm ceiling for USD/JPY for now. We’re are now keenly waiting to see if upcoming US non-farm payroll data tomorrow might trigger further pullback in USD/JPY.

In other parts of the currency markets, Swiss Franc trails only behind the Yen in strength for the week, with Sterling ranking third. On the flip side, Canadian Dollar is lagging as the weakest performer, followed by New Zealand Dollar and Australian Dollar. Dollar and the Euro are positioned in the middle.

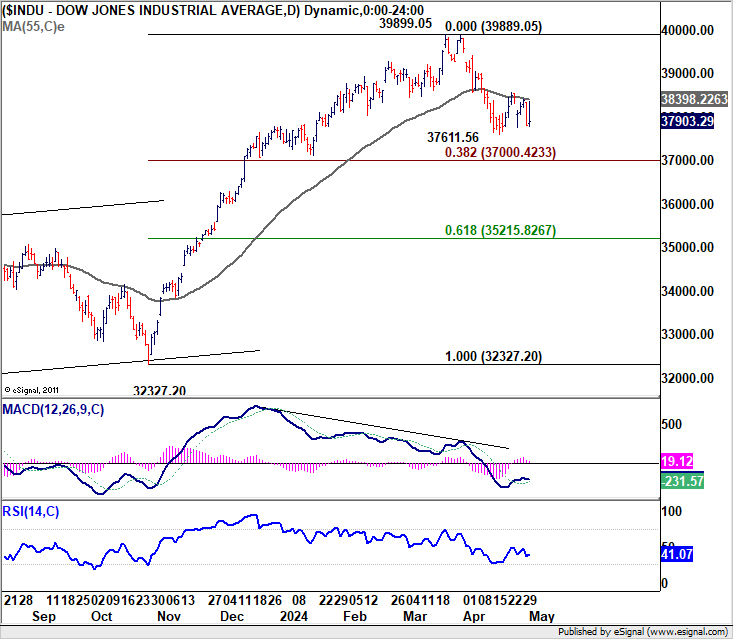

Technically, near term outlook in DOW remains bearish as it’s firmly capped by 55 D EMA. The first question for the rest of the week would be on whether correction from 39899.05 would resume through 37611.56. The second question is, if #1 realizes, how would DOW reaction to 38.2% retracement of 32327.20 to 39889.05 at 37000.42. That would set the tone on risk sentiment for the rest of the quarter.

In Europe, at the time of writing, FTSE is up 0.45%. DAX is up 0.18%. CAC is down -0.63%. UK 10-year yield is down -0.0398 at 4.334. Germany 10-year yield is down -0.009 at 2.577. Earlier in Asia,Nikkei fell -0.10%. Hong Kong HSI rose 2.50%. China was on holiday, Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.0101 to 0.906.

US initial jobless claims unchanged at 208k, vs exp 212k

US initial jobless claims was unchanged at 208k in the week ending April 27, lower than expectation of 212k. Four-week moving average of initial claims fell -3.5k to 210k. Continuing claims was unchanged at 1774k in the week ending April 20. Four-week moving average of continuing claims fell -4k to 1779k.

Also released IS trade deficit widened slightly from USD -68.9B to USD -69.4B, versus expectation of US -69.3B. Nonfarm productivity rose 0.3% in Q1, versus expectation of 0.8%. Unit labor costs rose 4.7% in Q1 versus expectation of 3.2%.

Canada trade balance recorded CAD -2.3B deficit, versus expectation of USD 1.0B surplus.

Eurozone PMI manufacturing finalized at 45.7, deepens recession despite bright spots in Spain and Netherlands

Eurozone’s manufacturing sector remains entrenched in recession as April’s PMI figures highlight ongoing challenges and disparities within the region. The overall Manufacturing PMI for the Eurozone was finalized at 45.7, a slight decrease from March’s 46.1.

Among the member states, Greece led with a PMI of 55.2, though it marked a three-month low for the country. Spain and the Netherlands exhibited positive trends, with Spain reaching a 22-month high at 52.2 and the Netherlands achieving a 20-month high at 51.3. Conversely, major economies like Germany, France, and Italy continued to struggle. Germany’s PMI slightly improved to a two-month high of 42.5, and France’s was a three-month low at 45.3, despite a slight uptick from the flash estimate.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted the manufacturing sector is prolonging its drawn-out recession into April.” He highlighted the significant downturn in new orders, which he described as “a rapid decline unmatched in speed over the past four months and devoid of international support.” De la Rubia also pointed out the concerning trends in the capital goods sector, which is usually a bellwether for broader industrial health but has been “hit particularly hard” in the current cycle.

Spain stands out as an anomaly within the Eurozone, continuing to demonstrate economic resilience with sustained growth in its manufacturing sector. This divergence is notable, especially against the backdrop of more subdued economic performances in other major Eurozone economies like Germany, France, and Italy, which have failed to gain similar momentum.

Swiss CPI rises to 1.4% yoy in Apr, above expectations

Swiss CPI rose 0.3% mom in April, above expectation of 0.2% mom. CPI core (excluding fresh and seasonal products, energy and fuel) rose 0.4% mom. Domestic products prices rose 0.1% mom. Import products prices rose 1.1% mom.

Over the 12 month period, CPI accelerated from 1.0% yoy to 1.4% yoy, above expectation of 1.1% yoy. CPI core increased from 1.0% yoy to 1.2% yoy. Domestic products price growth rises from 1.7% yoy to 2.0% yoy. Imported products prices contraction lessened from -1.3% yoy to -0.4% yoy.

Also from Switzerland, retail sales fell -0.1% yoy in March, versus expectation of 0.2% yoy rise. PMI manufacturing fell sharply from 41.4, well below expectation of 45.8.

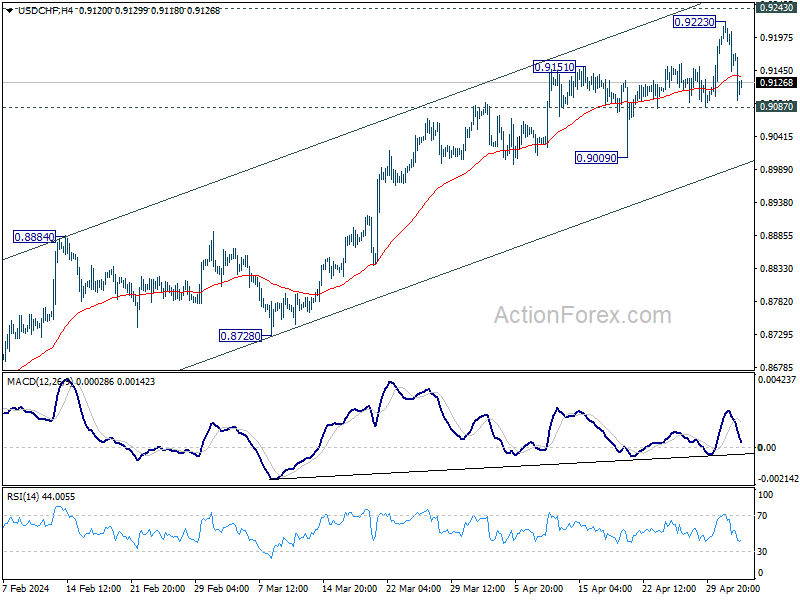

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9128; (P) 0.9176; (R1) 0.9207; More….

Intraday bias in USD/CHF remains neutral for the moment. Further rally is still in favor as long as 0.9087 support holds. On the upside, above 0.9223 will resume larger rally to 0.9243 resistance. Decisive break there will carry larger bullish implication. However, firm break of 0.9087 will indicate rejection by 0.9243 and turn bias back to the downside 0.9009 support instead.

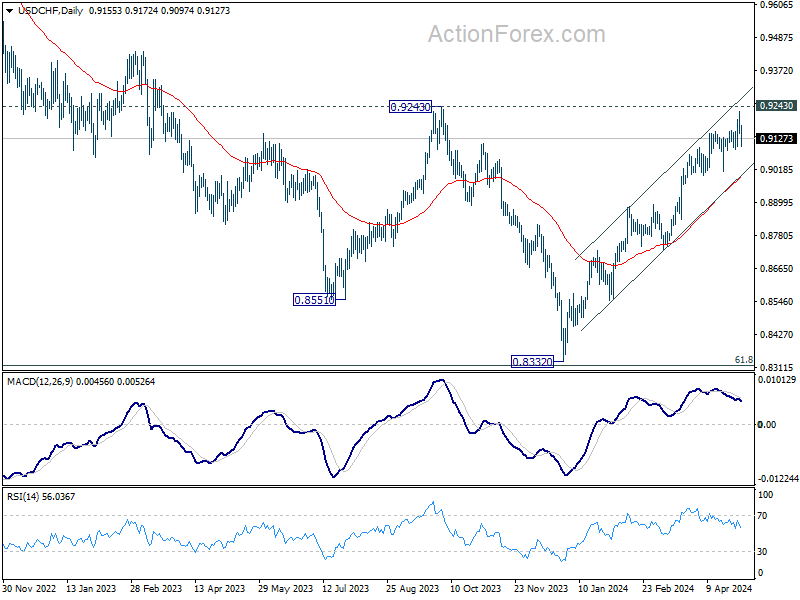

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8884 resistance turned support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | -0.20% | 14.90% | 15.90% | |

| 23:50 | JPY | Monetary Base Y/Y Apr | 2.10% | 1.70% | 1.60% | |

| 23:50 | JPY | BoJ Meeting Minutes | ||||

| 01:30 | AUD | Building Permits M/M Mar | 1.90% | 3.20% | -1.90% | -0.90% |

| 01:30 | AUD | Trade Balance (AUD) Apr | 5.02B | 7.37B | 7.28B | 6.59B |

| 05:00 | JPY | Consumer Confidence Apr | 38.3 | 39.5 | 39.5 | |

| 06:30 | CHF | Real Retail Sales Y/Y Mar | -0.10% | 0.20% | -0.20% | |

| 06:30 | CHF | CPI M/M Apr | 0.30% | 0.20% | 0.00% | |

| 06:30 | CHF | CPI Y/Y Apr | 1.40% | 1.10% | 1.00% | |

| 07:30 | CHF | Manufacturing PMI Apr | 41.4 | 45.8 | 45.2 | |

| 07:45 | EUR | Italy Manufacturing PMI Apr | 47.3 | 49.8 | 50.4 | |

| 07:50 | EUR | France Manufacturing PMI Apr F | 45.3 | 44.9 | 44.9 | |

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 42.5 | 42.2 | 42.2 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 45.7 | 45.6 | 45.6 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | -3.30% | 0.70% | ||

| 12:30 | CAD | Trade Balance (CAD) Mar | -2.3B | 1.0B | 1.4B | |

| 12:30 | USD | Trade Balance (USD) Mar | -69.4B | -69.3B | -68.9B | |

| 12:30 | USD | Initial Jobless Claims (Apr 26) | 208K | 212K | 207K | 208K |

| 12:30 | USD | Nonfarm Productivity Q1 P | 0.30% | 0.80% | 3.20% | |

| 12:30 | USD | Unit Labor Costs Q1 P | 4.70% | 3.20% | 0.40% | |

| 14:00 | USD | Factory Orders M/M Mar | 1.60% | 1.40% | ||

| 14:30 | USD | Natural Gas Storage | 68B | 92B |