Dollar traded broadly higher in Asian session, trying to stage a comeback after a failed rally attempt overnight. Renewed focus on tariffs appears to be driving some of the greenback’s momentum. Meanwhile, broader market sentiment is just steady following Nvidia’s strong earnings report, with lingering concerns over competition from China’s DeepSeek AI continue to weigh.

Tariffs are back in headlines after US Commerce Secretary Howard Lutnick revealed that the “big transaction” involving reciprocal tariffs is set for April 2. The date was pushed from April 1, as US President Donald Trump—citing superstition—chose to avoid making major policy moves on that day.

Lutnick also noted that Canada and Mexico could avoid the planned 25% tariffs if they can demonstrate sufficient progress on border security and fentanyl control. However, he added that Trump would ultimately decide whether to pause again or proceed with the tariffs.

Despite Nvidia reporting an impressive 78% year-over-year sales increase and a 93% jump in data center revenue, its struggle to rebound with momentum. The company has yet to fully recover from its 17% drop on January 27—its worst single-day decline since 2020—amid growing concerns about China’s emerging AI competitor, DeepSeek.

Elsewhere, Aussie is struggling despite comments from a top RBA official suggesting that rate cuts are not on auto-pilot and that further easing would require more disinflation evidence. This cautious stance should have provided some support for the Aussie, but broader risk-off sentiment is keeping the currency under pressure.

For now, Aussie is sitting at the bottom of today’s performance chart. Kiwi is also underperforming, while Swiss Franc is the third worst performer of the day so far. At the top of the performance table, Dollar leads, followed by Yen and Loonie. Euro and British Pound are positioning in the middle.

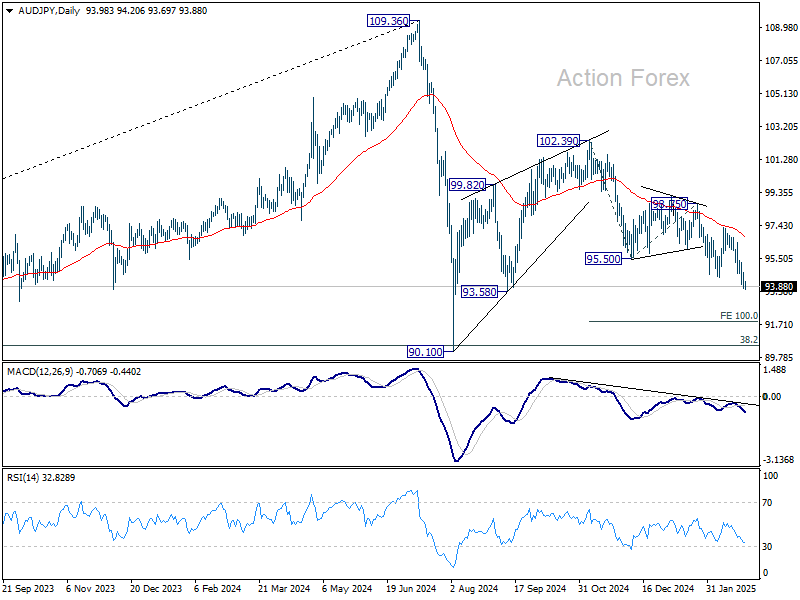

Technically, AUD/JPY’s fall from 102.39 resumed this week and further fall should now be seen to 100% projection of 102.39 to 95.50 from 98.75 at 91.86. As this decline is seen as the second leg of the corrective pattern from 90.10, strong support should be seen around there to bring reversal. But risk will continue to stays on the downside as long as 55 D EMA (now at 96.74) holds, in case of recovery.

In Asia, at the time of writing, Nikkei is up 0.14%. Hong Kong HSI is down -0.76%. China Shanghai SSE is down -0.49%. Singapore Strait Times is down -0.13%. Japan 10-year JGB yield is up 0.036 at 1.402. Overnight, DOW fell -0.43%. S&P 500 rose 0.01%. NASDAQ rose 0.26%. 10-year yield fell -0.049 to 4.249.

RBA’s Hauser: Global uncertainty justifies rate cut, but more easing depends on disnflation evidence

RBA Deputy Governor Andrew Hauser told the parliament today that mounting global uncertainty had a chilling effect on economic activity, which played a role in the board’s decision to cut the cash rate by 25 bps this month.

He noted that businesses are becoming increasingly cautious, delaying investment projects and expansion plans as they wait for clearer economic signals, “just to see how things pan out.”

This hesitation, he suggested, made a slight easing of monetary policy a “sensible” response to support economic stability.

However, Hauser emphasized that further rate cuts are not guaranteed and will depend on incoming inflation data. Policymakers remain optimistic about further disinflation but need to see clear evidence before committing to additional policy easing.

NZ ANZ business confidence rises to 58.4, on the path to recovery

New Zealand’s ANZ Business Confidence rose from 54.4 to 58.4 in February. However, the Own Activity Outlook, slipped slightly from 45.8 to 45.1, highlighting that while sentiment is improving, actual activity remains uncertain.

Pricing and cost indicators painted a mixed picture. Inflation expectations for the next year eased from 2.67% to 2.53% and cost expectations fell from 73.6 to 71.3. But wage expectations remained elevated at 79.2 despite fall from 83.1, and pricing intentions ticked up from 45.7 to 46.2.

ANZ noted that the economy is on the “path to recovery,” supported by lower interest rates and stronger-than-expected commodity export prices. However, the bank cautioned that the next phase of growth remains “a point of debate.”

The pace of expansion will depend on how households perceive current interest rates, the extent to which global uncertainty influences business investment, and whether firms push forward despite challenges. Additionally, potential labor shortages could emerge as a key constraint on further growth.

BoE’s Dhingra: Orderly trade fragmentation unlikely to require monetary policy response

BoE MPC member Swati Dhingra suggested that the inflationary impact of rising global tariffs could be tempered by weaker economic growth.

She added that if the global economy undergoes a “fragmentation in an orderly way,” monetary policy might not need to react immediately as prices readjust to new geopolitical shifts.

However, she cautioned that in an “extreme scenario” where multiple major economies erect significant trade barriers similar to those proposed by the US, “severe strain on a few sources of supply” could lead to sharp price spikes, reminiscent of those seen following Russia’s 2022 invasion of Ukraine.

Despite the risks, Dhingra downplayed the likelihood of a severe disruption, noting that “the world economy seems to be moving closer to an orderly fragmentation.”

Looking ahead

Swiss GDP, Eurozone M3 monthly supply will be released in European session. ECB will publish meeting accounts.

Later in the day, US will release GDP revision, durable goods orders and pending home sales.

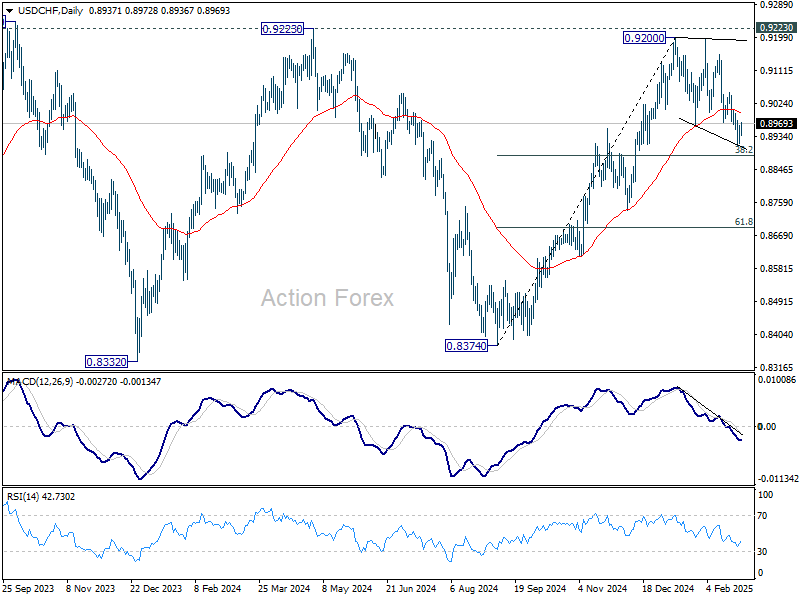

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8920; (P) 0.8943; (R1) 0.8969; More…

USD/CHF recovered notably but stays below 0.9053 resistance and intraday bias remains neutral. The corrective pattern from 0.9200 could still extend lower. But strong support should be seen from 38.2% retracement of 0.8374 to 0.9200 at 0.8884 to complete it, and bring larger rise resumption. On the upside, above 0.9053 will bring retest of 0.9200 resistance. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.