Yen volatility remains a key theme in Asian session today. Stronger-than-expected Japanese inflation data provided further justification for BoJ’s ongoing policy normalization, reinforcing speculation that the central bank may hike rates sooner than previously anticipated.

However, Yen’s rally lost momentum after Japan’s 10-year JGB yield pulled back sharply. This dip in yield came after BoJ Governor Kazuo Ueda told parliament that the central bank is ready to step in to stabilize markets if yields rise too sharply, hinting at possible intervention in the bond market to smooth fluctuations.

Despite this pullback, there are no clear signs of reversal in both JGB yields and Yen. Market participants may continue to position for an earlier BoJ rate hike, given the persistent inflationary pressures and rising wage expectations in Japan.

Meanwhile, Dollar plunged to a two-month low overnight before stabilizing slightly. The previous Dollar rally was fueled by expectations that US President Donald Trump’s trade policies would quickly escalate into a broader tariff war. However, progress on tariff implementation has been much slower than expected, with the only concrete measure so far being a 10% additional tariff on Chinese imports. As a result, some traders have begun closing long dollar positions, leading to its this week’s weakness.

For the week so far, Dollar is currently the worst performer, followed by Loonie and then Euro. Yen is still leading gains, with Aussie and Sterling also holding firm. Kiwi and Swiss Franc are positioning in the middle. Market focus now shifts to PMI releases from the UK, Eurozone, and the US, which could provide fresh directions.

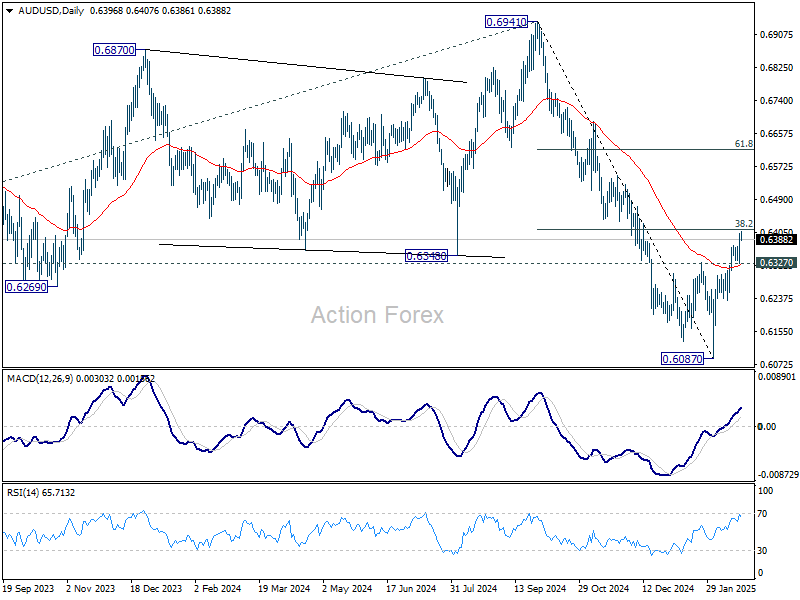

Technically, some attention is now on AUD/USD as it’s in proximity to key near term fibonacci resistance of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Rejection from this resistance is still expected, and break of 0.6327 support will argue that the corrective rebound from 0.6087 has completed. However, firm break of 0.6413 will pave the way to 61.8% retracement at 0.6615, even still as a correction.

In Asia, at the time of writing, Nikkei is up 0.17%. Hong Kong HSI is up 3.02%. China Shanghai SSE is up 0.66%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is down -0.0237 at 1.427. Overnight, DOW fell -1.01%. S&P 500 fell -0.43%. NADSAQ fell -0.47%. 10-year yield fell -0.035 to 4.500.

BoJ’s Ueda pledges action against sharp JGB yield rise, Yen tumbles

Yen pulled back sharply from its recent rally, along with steep fall in 10-year JGB yield from its 15-year high. The move came after BoJ Governor Kazuo Ueda reminded markets of the central bank’s commitment to curbing excessive yield volatility.

In parliamentary comments, Ueda stated, “We expect long-term interest rates to fluctuate to some extent.”

However, he cautioned that “when markets make abnormal moves and lead to a sharp rise in yields, we are ready to respond nimbly to stabilize markets.”

The pledge to increase bond purchases, if necessary, knocked the 10-year JGB yield off its 15-year high

Ueda declined to specify when BoJ might conduct emergency bond market operations, stating only that the central bank would closely monitor the market for signs of destabilization.

Japan’s core CPI jumps to 3.2% in Jan, above expectations

Japan’s inflation accelerated in January, with core CPI (ex-food) rising from 3.0% yoy to 3.2% yoy, surpassing expectations of 3.1% yoy and marking the fastest pace in 19 months, driven by higher rice and energy costs.

This was also the third consecutive month of acceleration, with core CPI rebounding sharply from 2.3% yoy in October. Inflation has now remained at or above BoJ’s 2% target since April 2022.

Core-core CPI (ex-food and energy) climbed to 2.5% yoy, up from 2.4% yoy, signaling broader price pressures beyond energy and food. Food prices, excluding perishables, surged 5.1% yoy, up from 4.4% yoy, driven by a 70.9% yoy spike in rice prices, the largest increase since data collection began in 1971. This sharp rise was attributed to supply shortages and higher production and transportation costs.

Energy prices also saw a notable increase of 10.8% yoy, up from 10.1% yoy in December, as gasoline costs rose following government subsidy reductions. Meanwhile, services inflation slowed slightly to 1.4% yoy from 1.6% yoy.

Headline CPI surged from 3.6% yoy to 4.0% yoy, a two-year high.

Japan’s PMI improves, but business confidence hits lowest since 2021

Japan’s PMI data for February showed slight improvements, with PMI Manufacturing rising from 48.7 to 48.9. Meanwhile, PMI Services edged up from 53.0 to 53.1. Composite PMI increased from 51.1 to 51.6, the highest in five months.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, the “modest improvement” was driven by sustained growth in services, with firms crediting business expansion plans and improved sales.

However, optimism about future business activity weakened, with confidence dropping to its lowest level since January 2021. Companies cited labor shortages, persistent inflation, and weak domestic economic conditions as major concerns.

Employment growth slowed to its weakest pace in over a year, reflecting businesses’ caution about hiring amid economic uncertainty. Additionally, input price inflation remained elevated, similar to January’s historically high levels.

RBA’s Bullock: More rate cuts possible, but patience needed

At a parliamentary committee hearing today, RBA Governor Michele Bullock explained that this week’s 25bps rate cut was based on better-than-expected inflation data, weaker private demand, and wage growth aligning with forecasts.

Also, she acknowledged that the board is mindful of timing, stating, “What’s also playing on the board’s mind is that the board also doesn’t want to be late, and arguably we were late raising interest rates on the way up.”

While further easing remains on the table, Bullock emphasized the need for caution. “We are not pre-committed. We’re going to be data-driven on this and I think people just have to be patient,” she added.

Deputy Governor Andrew Hauser echoed this sentiment, reinforcing the RBA’s wait-and-see approach. He remarked, “If we’re wrong and inflation moves more quickly downwards, you could celebrate that fact and policy will need to respond, but we’d rather wait and see than assume that’s what’s going to happen.”

Australia’s PMI composite hits 6-month high, but business confidence dips

Australia’s PMI data for February showed continued expansion in private sector activity, with Manufacturing PMI rising to from 50.2 to 50.6, its highest level in 27 months. Meanwhile, Services PMI edged up from 51.2 to 51.4, and Composite PMI ticked up from 51.1 to 51.2, both reaching six-month highs.

According to Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, the latest figures indicate a “modest” but steady improvement in economic conditions, while growth was broad-based.

However, business sentiment weakened to its lowest level since October 2024. This caution also affected pricing strategies, with businesses reluctant to fully pass on cost increases, leading to a slowdown in selling price inflation.

RBNZ’s Conway: 50bps cut the clear choice, signs of economic turnaround emerging

RBNZ Chief Economist Paul Conway revealed in a Reuters interview that the central bank considered both 25bps and 75bps rate cuts ahead of this week’s policy decision. But the bank ultimately concluded that a 50bps reduction “was the way to go” given the state of the economy and inflation.

Conway pointed to recent data in manufacturing and services, indicating that some businesses may already be “starting to feel a bit of a turnaround.” However, he acknowledged that companies remain cautious.

Regarding the labor market, Conway noted that employment trends typically lag economic activity. He added that”businesses need to have confidence that growth is returning and that growth will be sustained into the future before they start to think about employing someone.”

Fed’s Kugler supports holding rates for some time

Fed Governor Adriana Kugler said overnight that it’s “appropriate to hold the federal funds rate in place for some time”, citing the current balance of risks in the economy.

Kugler acknowledged that inflation still has “some way to go” before reaching 2% target. She highlighted that while the labor market remains strong and risks of a downturn have eased, “upside risks to inflation remain.”

Regarding the potential impact of new tariffs, Kugler stated that while they could contribute to higher prices, the extent of their effect remains uncertain. She emphasized that policymakers will need to “wait” for more data to assess how trade policy shifts might influence inflation and broader economic conditions.

Fed’s Musalem warns of inflation expectations unanchoring

St. Louis Fed President Alberto Musalem raised concerns overnight about inflation expectations becoming “unanchored”, emphasizing that the risk is higher when the economy is running without slack and after a period of elevated inflation.

Musalem pointed out that market and survey data show a notable rise in near-term inflation expectations over the past three months, reinforcing worries that inflation might remain above the Fed’s 2% target for longer than anticipated.

He warned that if inflation remains stuck at elevated levels or expectations continue to rise, “a more restrictive path of monetary policy relative to the baseline path might be appropriate.”

Fed’s Bostic sees two rate cuts in 2025 but flags significant uncertainty

Atlanta Fed President Raphael Bostic noted his baseline expectation for two 25bps rate cuts later this year, but cautioned that “the uncertainty around that is pretty significant”, with multiple factors that could shift the outlook in either direction.

He acknowledged growing concerns from businesses regarding the potential impact of new tariffs, immigration policies, and regulatory changes on economic conditions.

He noted that there is both enthusiasm and “widespread apprehension” among business contacts regarding these policy shifts. Specifically, he warned that tariffs could push up costs, adding, “Many feel confident that if that happens, then they can pass along higher costs in their prices.”

Looking ahead

UK retail sales and PMIs, as well as Eurozone PMIs will be released in European session. Later in the day, Canada will release retail sales. US will release PMIs and existing home sales.

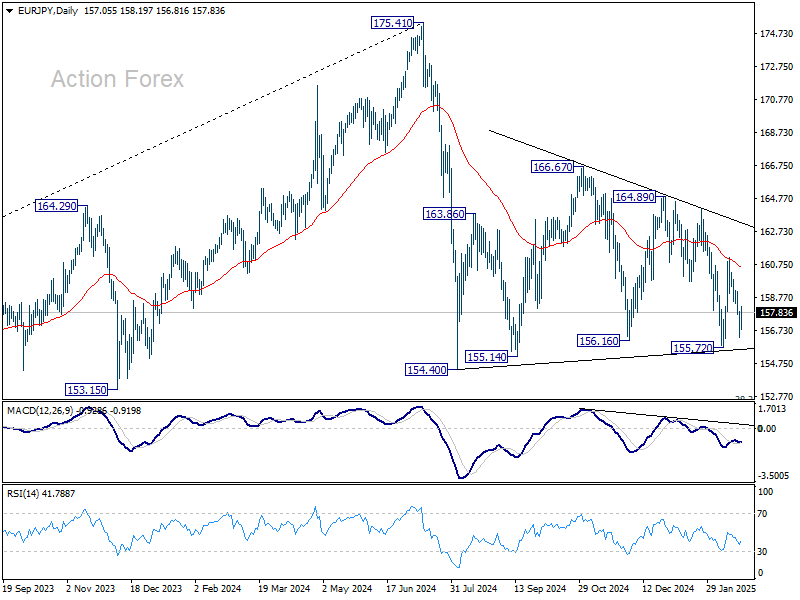

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.30; (P) 157.15; (R1) 157.98; More…

EUR/JPY recovered ahead of 155.72 support and intraday bias is turned neutral again. Overall outlook is unchanged that consolidation pattern from 154.40 might extend further. Above 185.35 minor resistance will bring stronger rebound to 161.17. Nevertheless, firm break of 155.72 support will be a strong sign that whole fall from 175.41 is resuming. Retest of 154.40 support should be seen next and firm break there should confirm.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.