Both Sterling and Japanese yen are among the weakest-performing currencies today, following their respective central banks meetings. BoE left rates unchanged at 4.75%, but the surprise came from a dovish shift in the MPC, with three members voting for a cut. While BoE reiterated that a “gradual approach” to easing remains appropriate, rising concerns over economic stagnation suggest the Committee may be ready to expedite rate cuts once the full impact of the Autumn Budget and potential US trade policies becomes clear.

Yen fared even worse after BoJ maintained its policy stance without offering any signals on the timing of future rate hikes. Governor Kazuo Ueda highlighted external risks, particularly stemming from US trade policies, which he described as a significant source of uncertainty for global and Japanese economies. Ueda stressed the need to carefully evaluate the impact of these risks on Japan’s economic outlook before moving on with policy normalizations.

As for the week so far, Dollar remains the runaway leader, supported by Fed’s hawkish guidance, including slower pace of easing in 2025 and the prospect of a higher terminal rate. Despite today’s pullback, Sterling remains the second-strongest performer, while Swiss franc holds third place.

At the weaker end, Yen continues to struggle, weighed down further by rising US Treasury yields. New Zealand dollar is the second worst, pressured by weak GDP data that has fueled speculation of a lower terminal rate in RBNZ’s easing cycle. Australian Dollar follows, with Euro and Canadian Dollar mixed in the middle of the pack.

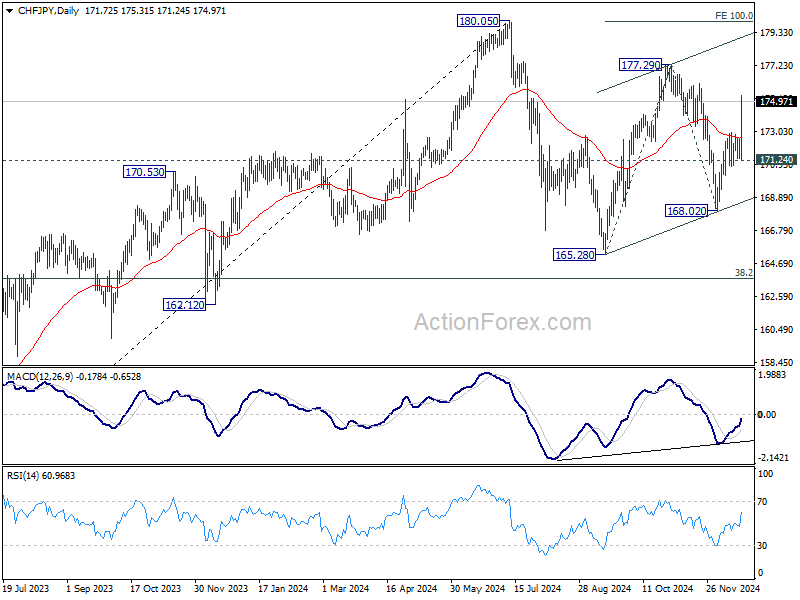

Technically, CHF/JPY’s outlook is cleared alongside many Yen crosses with the strong rally, and firm break of 55 D EMA today. Corrective pattern from 165.28 is still extending with rise from 168.02 as the third leg. Further rally is expected as long as 171.24 support holds. Next target is 177.29 and break there will target 100% projection of 165.28 to 177.29 from 168.02 at 180.03, which is close to 180.05 high.

In Europe, at the time of writing, FTSE is down -1.02%. DAX is down -0.99%. CAC is down -1.14%. UK 10-year yield is up 0.024 at 4.587. Germany 10-year yield is up 0.0580 at 2.305. Earlier in Asia, Nikkei fell -0.69%. Hong Kong HSI fell -0.56%. China Shanghai SSE fell -0.36%. Singapore Strait Times fell -0.44%. Japan 10-year JGB yield rose 0.0194 to 1.086.

US initial jobless claims fall back to 220k

US initial jobless claims fell -22k to 220k in the week ending December 14, below expectation of 240k. Four-week moving average of initial claims rose 1k to 224k.

Continuing claims fell -5k to 1874k in the week ending December 7. Four-week moving average of continuing claims fell -6k to 1880k.

BoE stands pat with dovish 6-3 vote

BoE held its Bank Rate steady at 4.75%, in line with expectations, but the vote leaned more dovish than before. Three MPC members—Swati Dhingra, Dave Ramsden, and Alan Taylor—voted for a rate cut.

BoE reaffirmed that a “gradual approach to removing monetary policy restraint remains appropriate” and emphasized the need to maintain restrictive policy “for sufficiently long” to ensure inflation sustainably returns to 2% target. Decisions on the degree of restrictiveness will be made on a meeting-by-meeting basi.

The statement acknowledged that headline CPI inflation rose to 2.6% in November, slightly above prior expectations, while services inflation remained persistently high. Inflation is expected to rise slightly in the near term.

Meanwhile, indicators of near-term activity have weakened, and staff now expect GDP growth to fall short of projections from the November Monetary Policy Report, although the labor market is seen as broadly balanced.

BoE also flagged uncertainties arising from global inflationary shocks, geopolitical risks, trade policy developments, and measures in the Autumn Budget, all of which could impact growth and inflation.

German Gfk consumer sentiment improves slightly but remains fragile

Germany’s GfK Consumer Sentiment Index for January rose to -21.3, improving from December’s -23.1.

December’s subindices reflected mixed dynamics: economic expectations moved into positive territory at 0.3, up from -3.6, and income expectations increased to 1.4 from -3.5. Willingness to buy also ticked higher to -5.4 from -6.0, while willingness to save fell sharply to 5.9 from 11.9.

According to Rolf Bürkl, consumer expert at NIM, the improvement comes after a steep decline the prior month, partially reversing earlier losses. However, Bürkl noted that at -21.3 points, consumer sentiment remains at a very low level, highlighting a trend of “stagnation since mid-2024.”

He warned that a sustained recovery is “not yet in sight” due to persistent challenges. High food and energy prices, alongside growing concerns about job security in key sectors, continue to weigh heavily on sentiment.

BoJ stand pat, highlights wage and global risks

BoJ kept its uncollateralized overnight call rate unchanged at 0.25%, as widely anticipated, with an 8-1 vote in favor. Naoki Tamura dissented, advocating for a rate increase to 0.50%.

Governor Kazuo Ueda, speaking at the post-meeting press conference, reiterated that rate hikes would proceed cautiously. He noted, “If the economy and prices move in line with our forecast, we will continue to raise our policy rate,” but emphasized the need to carefully assess data before adjusting the level of monetary support.

The gradual pace of tightening, he explained, is due to the “moderate” rise in underlying inflation, which lacks the strength to warrant aggressive moves.

Ueda highlighted the importance of monitoring wage dynamics, particularly in the context of next year’s wage negotiations, to gauge the strength of Japan’s wage-inflation cycle.

He also pointed to uncertainties in the global economic outlook and the impacts of policy decisions under the incoming U.S. administration, despite the overall resilience of the US economy.

New Zealand’s GDP contracts -1% qoq in Q3, broad economic weakness

New Zealand’s economy contracted by -1.0% qoq in Q3, significantly worse than market expectations of -0.2%. The previous quarter’s GDP figure was also revised down sharply, from -0.2% to -1.1%, painting a grimmer picture of the country’s economic performance.

The decline was broad-based, with activity falling in 11 out of 16 industries, including significant contractions in manufacturing, business services, and construction. While primary industries posted gains, both goods-producing and service industries experienced declines.

On a per capita basis, GDP dropped -1.2% qoq, marking the eighth consecutive quarterly decline. The expenditure measure of GDP also contracted by -0.8% qoq. Notably, household consumption expenditure decreased by -0.3% qoq, with reductions in spending on essentials such as grocery food and electricity, highlighting the strain on consumer budgets.

NZ ANZ business confidence falls to 62.3, demand recovery offers glimmers of hope

New Zealand’s ANZ Business Confidence Index fell to 62.3 in December, down from 64.9. However, some subindices showed encouraging signs of recovery. The own activity outlook improved to 50.3 from 48.0, while profit expectations rose significantly to 31.1 from 26.5. Investment intentions also jumped to 21.5 from 18.0, signaling increased business willingness to allocate resources despite a challenging environment.

However, labor market metrics were mixed, with employment intentions slipping slightly from 14.7 to 14.3. At the same time, cost pressures intensified sharply, as cost expectations surged to 70.1 from 62.9, and wage expectations jumped from 75.5 to 79.2. Price intentions remained steady at 42.7, slightly up from 42.2, while inflation expectations ticked higher to 2.63%, up from 2.53%, reflecting ongoing pricing pressures.

ANZ noted that while the survey results indicate signs of recovering demand, they come against the backdrop of this morning’s weak Q3 GDP figures, which showed a sharp contraction. The low bar set by the GDP downturn provides room for optimism if demand continues to improve. However, rising cost and wage pressures could complicate the outlook, especially for inflation management.

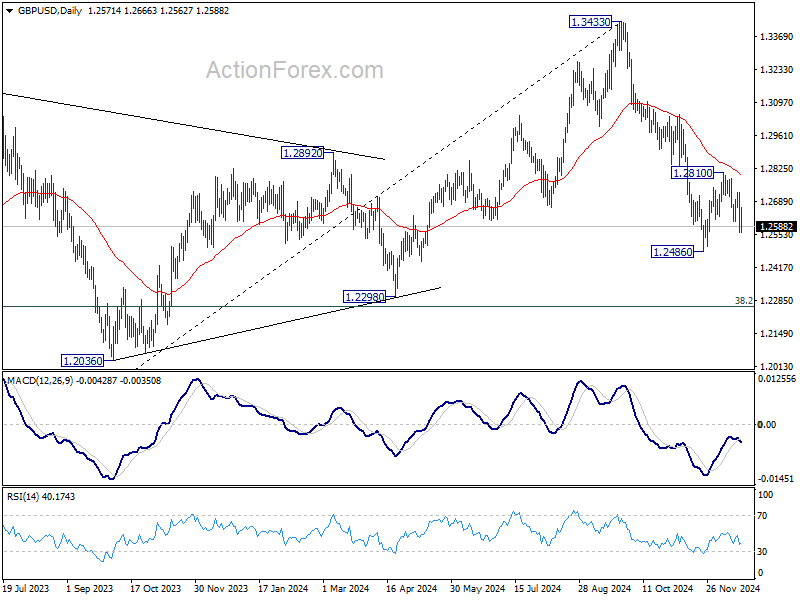

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2513; (P) 1.2621; (R1) 1.2679; More…

Intraday bias in GBP/USD remains on the downside despite some volatility during today. Recovery from 1.2486 should have completed at 1.2810. Retest of 1.2486 should be seen next. Firm break there will resume the fall from 1.3433 and target 1.2298 cluster support zone. Nevertheless, break of 1.2728 minor resistance will turn bias to the upside for 1.2810 and above instead.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.