Dollar steadied after yesterday’s selloff, recovering slightly as markets braced for the non-farm payroll report. Traders appear increasingly confident about a December rate cut, shifting the focus of today’s employment data toward its implications for January’s FOMC meeting. While the report may still trigger some market volatility, many participants seem inclined to look past this release, awaiting key indicators like next week’s CPI or January’s NFP for more decisive cues.

Meanwhile, Australian and New Zealand Dollars remained under pressure, showing weakness despite the absence of a clear risk-off sentiment. Global equity markets are holding up well, with US indices near record highs and Germany’s DAX extending its powerful record-breaking rally. Australian stocks also hit new highs, albeit with slower momentum. The Antipodean currencies’ weakness could reflect rising concerns about the escalation of US-China tariff tensions under the incoming US administration next year.

For the week so far, Swiss Franc unexpectedly leads as the strongest performer, followed by Sterling and Dollar. Australian Dollar lags at the bottom, trailed by Kiwi and Yen. Euro and Canadian Dollar are positioned mid-pack.

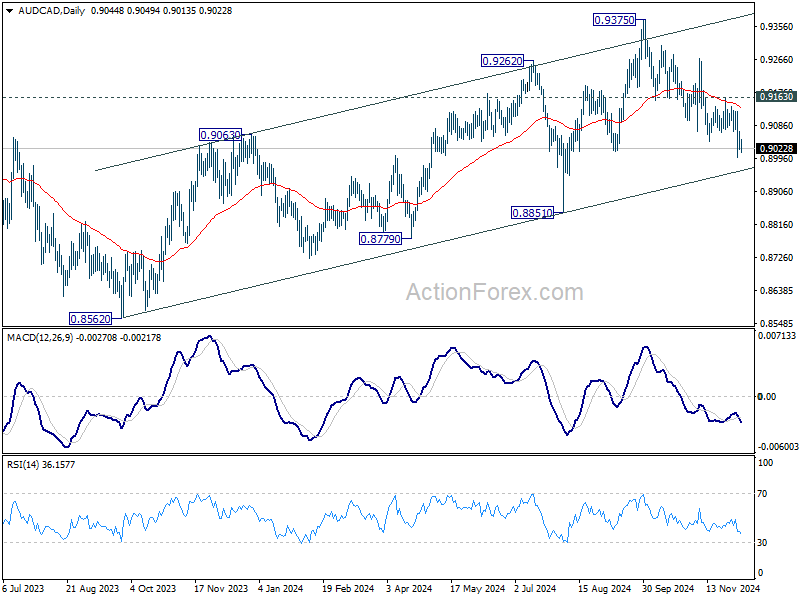

Technically, AUD/CAD’s fall from 0.9375 could still be a corrective move tot he rise from 0.8562. Strong rebound from rising channel support (now at 0.8966), followed by break of 0.9163 resistance will suggest that the pull back has completed, and keep the up trend from 0.8562 intact. However, decisive break of the channel support will indicate bearish trend reversal, and target 0.8851 support and below. Canada’s upcoming employment data today could be the catalyst for AUD/CAD’s next significant move.

In Asia, Nikkei closed down -0.77%. Hong Kong HSI is up 1.52%. China Shanghai SSE is up 1.05%. Singapore Strait Times is down -0.42%. Japan 10-year JGB yield fell -0.0179 to 1.055. Overnight, DOW fell -0.55%. S&P 500 fell -0.19%. NASDAQ fell -0.17%. 10-year yield closed flat at 4.180.

Japan’s nominal wages growth hits multi-decade high, but real gains remain elusive

Japan’s labor market data for October showed nominal wages, or labor cash earnings, rose 2.6% yoy, in line with expectations. Regular pay, or base salary, grew 2.7% yoy, marking the fastest increase since November 1992. Full-time workers saw an even sharper wage rise at 2.8% yoy, the highest increase since comparable records began in 1994. Overtime pay also rebounded, registering a 1.4% yoy growth compared to a -0.9% decrease in the prior month.

However, real wages—adjusted for inflation—was stagnant, showing no change from a year ago. This followed declines of -0.4% and -0.8% yoy in September and August, respectively. The inflation rate used by Japan’s labor ministry for these calculations, excluding owners’ equivalent rent, slowed to 2.6%, the lowest in nine months.

On the household front, spending fell -1.3% yoy, better than the forecasted -2.6% yoy decline but still reflecting cautious consumer behavior. Food expenditures, comprising around 30% of total spending, dropped -0.8% yoy. Other categories faced sharper declines, including a -13.7% yoy plunge in clothing and shoes, a -10.7% yoy drop in housing-related expenditures, and a -14.0% yoy decrease in education spending, such as tuition fees.

NFP’s role looms larger for January Fed pause while December cut looks set

The pivotal US non-farm payroll report today stands at the center of market focus, with its implications likely to influence both the Fed decision outlook, but probably more on January meeting than this month’s.

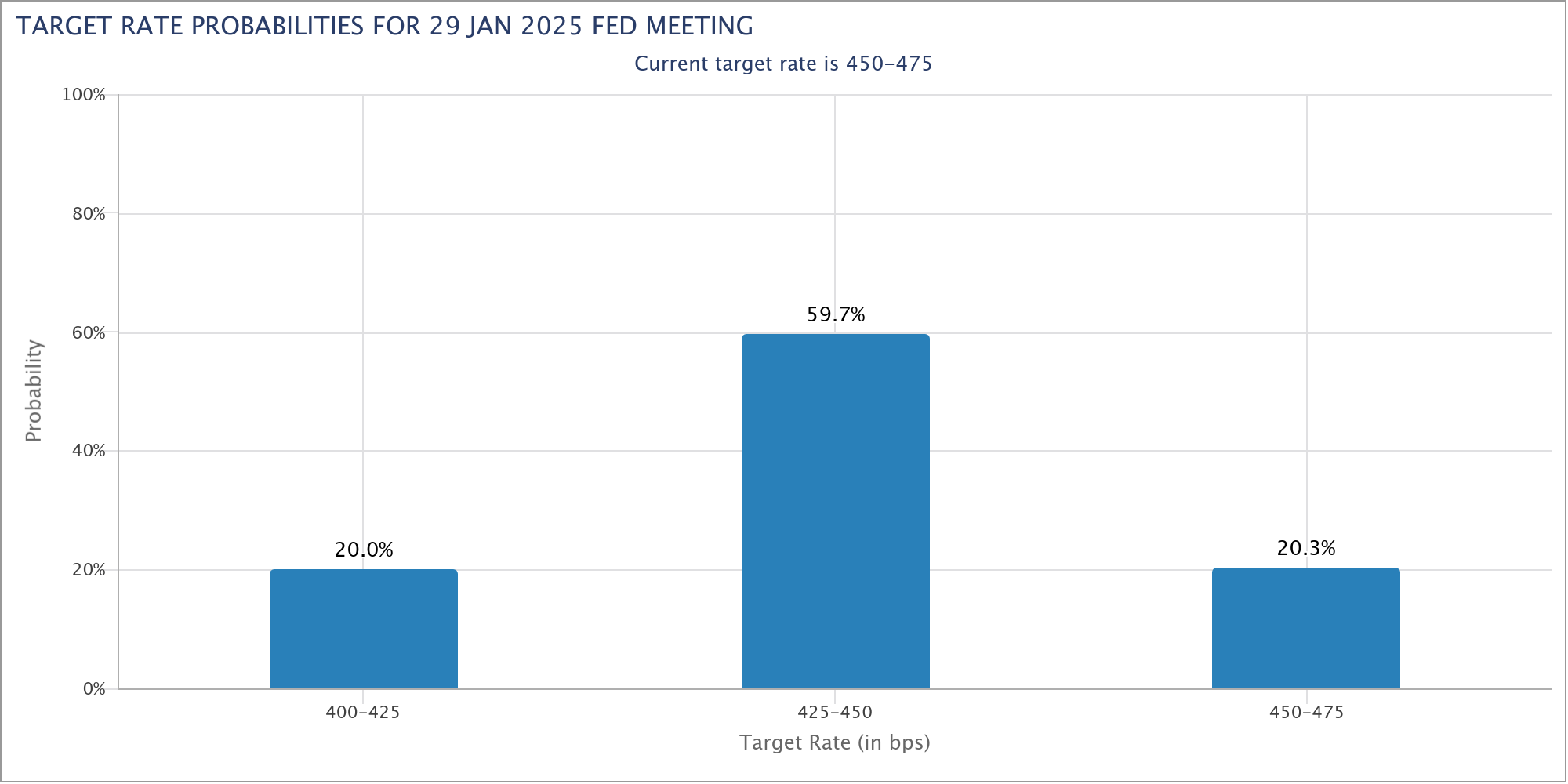

Fed fund futures indicate a 70% probability of a 25bps rate cut this month, up from 66% a week ago. This reflects a growing expectation that recent economic data, including ISM services and manufacturing figures, ADP employment, and JOLTs openings, support further easing to 4.25%-4.50% at the December 18 meeting. This mounting confidence in Fed’s decision is unlikely to be deterred by today’s data, barring any drastic upside surprises.

However, sentiment regarding January paints a different picture, with just a 20% likelihood of another 25bps cut to 4.00%-4.25%. A stronger-than-expected NFP report today, particularly one highlighting a significant rebound in job growth after October’s hurricane- and strike-induced distortions, could solidify expectations of a pause in January.

Recent labor market indicators offer a mixed but steady backdrop. ISM Manufacturing Employment improved to 48.1 from 44.4, while ISM Services Employment softened to 52.1 from 56.0. ADP employment showed a moderation in net job additions at 146K, down from a revised 184K prior. Meanwhile, the 4-week average of initial unemployment claims fell to a strong 218K from 236K. These data points suggest no major red flags for today’s NFP release.

In terms of market reactions, Dollar Index remains in a corrective phase after peaking at 108.07. While a recovery today is possible, near-term risks tilt to the downside as long as 106.72 resistance holds. Deeper pullback could extend to 38.2% retracement of 100.15 to 108.07 at 105.04 completion. Nevertheless, rise from 100.15 would remain in favor to resume at a later stage as long as 55 D EMA (now at 104.77) holds.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0533; (P) 1.0562; (R1) 1.0615; More…

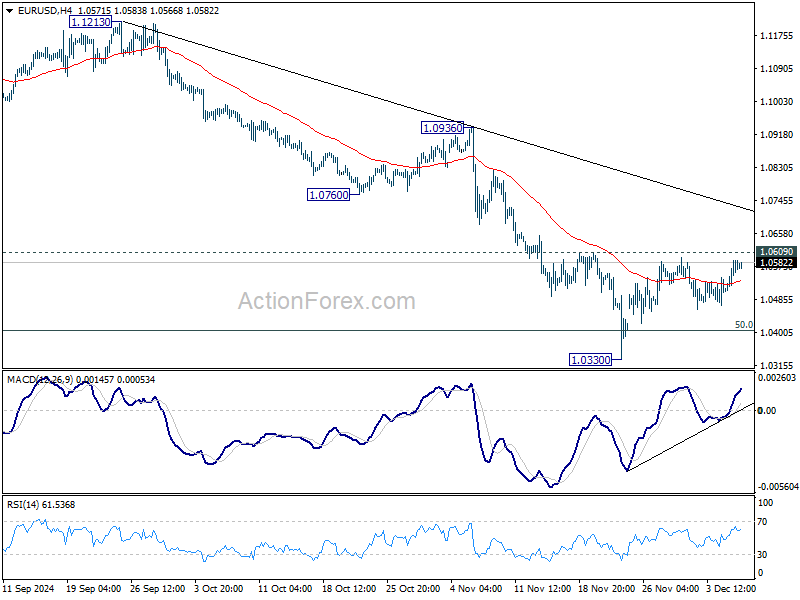

Intraday bias in EUR/USD remains neutral for the moment. On the upside, firm break of 1.0609 resistance will resume the rebound from 1.0330 to 55 D EMA (now at 1.0729). But strong resistance could be seen there to limit upside. . On the downside, break of 1.0330 will resume the fall from 1.1213. Also, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.