Dollar rallied sharply today after news broke that Republican candidate Donald Trump defeated Democrat Kamala Harris in North Carolina, a crucial battleground state. This win is considered a pivotal move toward Trump’s return to office, sparking significant moves across financial markets. US stock futures responded with enthusiasm, with DOW futures climbing over 500 points. Meanwhile, 10-year Treasury yield surged above 4.4%, reinforcing the sentiment around Trump’s impact on fiscal policy. Despite this initial surge, traders remain on edge, waiting for further confirmation from key states before taking on new positions.

Asian stock markets offered a mixed picture in response to the news. Japan’s Nikkei soared over 2%, driven by positive sentiment linked to a possible Trump victory, as markets see his economic policies as supportive of growth and deregulation. On the other hand, Hong Kong stocks suffered, dropping by more than -2.5% amid concerns over Trump’s stance on China, which could bring intensified tensions. In contrast, markets in China and Singapore traded in a narrow range, reflecting uncertainty and caution.

In currency markets, the Australian Dollar is currently the weakest performer, followed by Euro and Yen, pressured by Dollar’s strength. Meanwhile, Canadian Dollar joins Dollar as one of the stronger performers, with Swiss Franc also displaying resilience. New Zealand’s Kiwi is holding steady, seemingly unaffected by recent Q3 employment data, trading alongside the British Pound in mid-range.

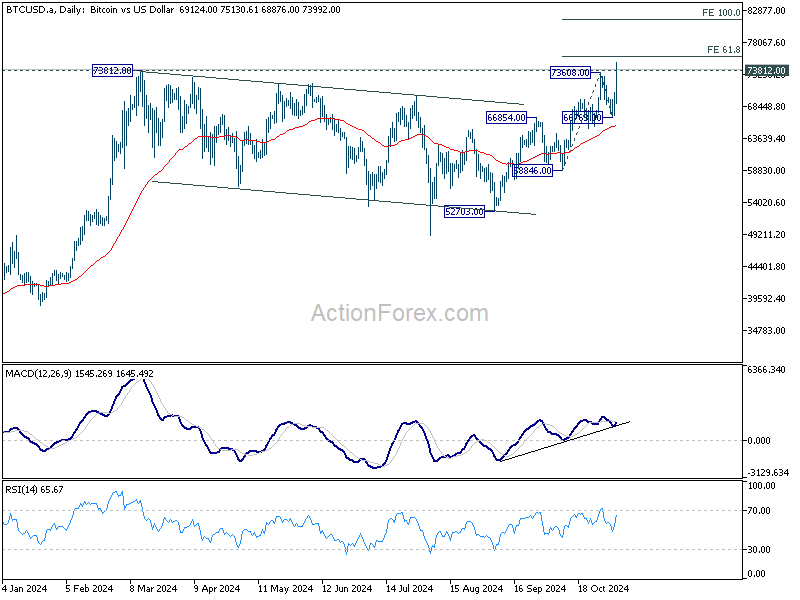

Technically, Bitcoin hits new record high by breaking through 73812 resistance today. Immediate focus is now on 61.8% projection of 58846 to 73608 from 66763 at 75885. Decisive break there could prompt upside acceleration to 100% projection at 81525 rather quickly.

In Asia, at the time of writing, Nikkei is up 2.24%. Hong Kong HSI is down -2.61%. China Shanghai SSE is up 0.16%. Singapore Strait Times is down -0.04%. Japan 10-year JGB yield is up 0.0421 at 0.971. Overnight, DOW rose 1.02%. S&P 500 rose 1.23% .NASDAQ rose 1.43%. 10-year yield fell -0.020 to 4.289.

BoC minutes reveals strong consensus for aggressive rate cut

Summary of BoC Governing Council’s October 23 meeting highlights a decisive stance among members to prioritize growth through an aggressive 50bps rate cut. While members initially discussed the possibility of a modest 25bps cut, a “strong consensus” emerged in favor of a larger reduction to counter economic headwinds.

The Governing Council members expressed “increasingly confident” that inflationary pressures are expected to ease, reducing the need for a restrictive policy stance. Some members voiced concern that an unusual 50bps cut might be perceived as a signal of “economic trouble.” Despite this, they agreed that a more substantial cut was justified, given the “ongoing softness” in the labor market and the need to bolster growth to “absorb excess supply” in the economy.

BoJ minutes: Yen stabilization gives time to monitor global economic risks

Minutes from BoJ’s September meeting reveal a careful stance on monetary policy amid global economic uncertainties. At the meeting, BoJ kept its interest rate steady at 0.25%.

Regarding future direction of monetary policy, members broadly agreed that if Japan’s economic and inflation outlook aligns with their projections, the Bank would “continue to raise the policy interest rate” and gradually adjust its level of monetary accommodation.

The minutes also underscore the need for “high vigilance” given uncertainties in overseas economies, particularly in the US, and ongoing volatility in global financial markets.

Some members pointed out that recent retracements in Yen’s depreciation have moderated upside risk to inflation from import prices. Given this development, they noted that the Bank has “enough time” to evaluate the effects of global economic shifts and recent policy rate hikes before deciding on further moves.

Japan’s PMI services finalized at 49.7, first contraction since Jun

Japan’s services sector slipped into contraction in October, with PMI Services index finalized at 49.7, down from September’s 53.1 and marking its first contraction since June. PMI Composite also declined to 49.6 from 52.0, signaling a contraction in private sector activity for the first time in four months and the lowest reading since November 2023.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, the services sector’s performance “came to an abrupt halt” at the start of Q4. While the decline was modest, it was driven by a notable slowdown in new business inflows, particularly in export orders. Despite the dip, businesses maintained a positive outlook, though optimism weakened to its lowest in over two-and-a-half years, with companies citing concerns over labor shortages as a key factor.

The services sector slowdown, combined with a continuing contraction in manufacturing, contributed to the steepest private sector contraction in nearly a year. New order inflows stagnated, particularly impacted by weakened demand in manufacturing order books. Business sentiment, overall, has also softened, with optimism now at its lowest since January 2021.

NZ employment falls -0.5% in Q3, unemployment rate rises to 4.8%

New Zealand’s labor market showed signs of cooling in Q3, with employment falling by -0.5% qoq, in line with expectations. Unemployment rate rose from 4.6 to 4.8%, slightly better than the anticipated 5.0%, but still indicative of softening labor conditions.

Labor force participation rate also declined, dropping from 71.7% to 71.2%, while the employment rate slipped from 68.4% to 67.8%, reflecting fewer people actively engaged in the workforce.

On the wage front, growth showed deceleration. The labor cost index, which includes salary and wage rates with overtime, rose by 3.8% yoy, down from the previous quarter’s 4.3% yoy increase.

The slowdown in wage growth suggests some relief in wage-driven inflation pressures, which could factor into RBNZ’s upcoming rate cut.

Looking ahead

Germany factory orders, Eurozone PMI services final and PPI, UK PMI construction will be released in European session. Later in the day, Canada will release Ivey PMI.

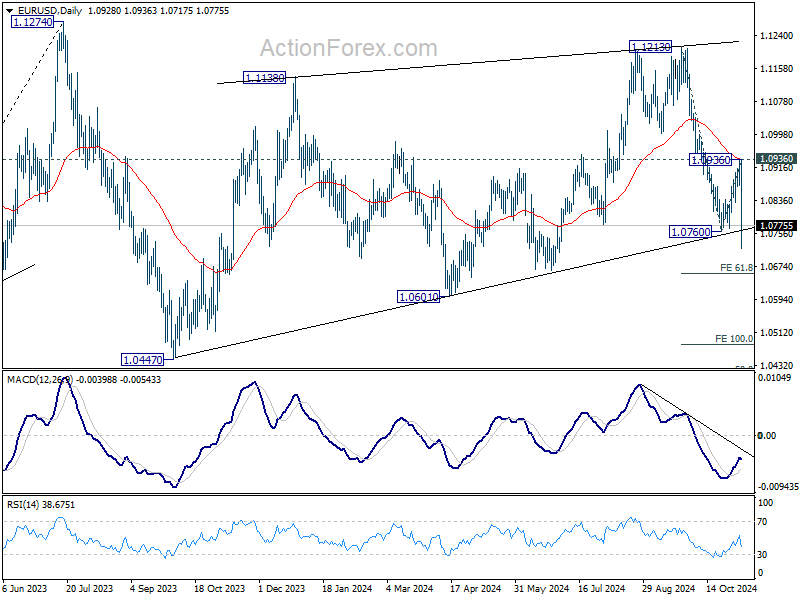

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0890; (P) 1.0913; (R1) 1.0954; More…

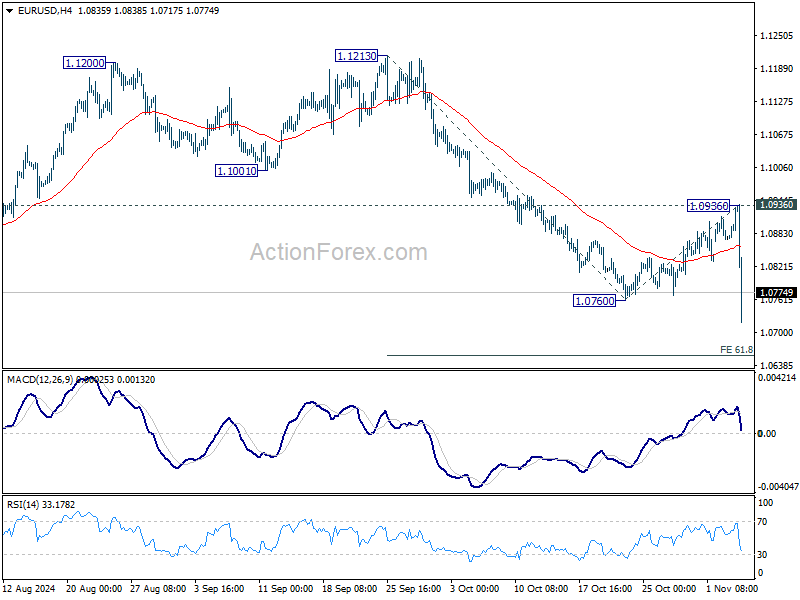

EUR/USD’s breach of 1.0760 indicates that corrective recovery from there has completed after rejection by 55 D EMA (now at 1.0939), and fall from 1.1213 is resuming. Intraday bias is back on the downside for 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656. Firm break there will pave the way to 100% projection at 1.0483. For now, near term outlook will stay bearish as long as 1.0936 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.