Swiss Franc remained relatively stable today following SNB’s decision to cut its policy rate by 25bps, bringing it down to 1.00%. This move defied some market speculations that anticipated a larger 50bps reduction. Despite opting for a smaller cut, SNB issued a decidedly dovish statement, sharply downgrading its inflation forecasts. The central bank signaled a clear easing bias, suggesting that further monetary accommodation is on the horizon. Incoming Chair Martin Schlegel reinforced this sentiment by indicating in an interview that another rate cut in December is “not unlikely.”

In the broader foreign exchange market, currencies traded within familiar ranges. Dollar softened despite better-than-expected durable goods orders and jobless claims data. Canadian Dollar emerged as the second weakest of the day, while Japanese Yen followed as the third. Australian Dollar led the gains, buoyed by strong risk-on sentiment s in both China and Hong Kong. New Zealand Dollar was the second-best performer, with British Pound also showing strength. Euro and Swiss Franc are mixed, positioned in the middle of the currency spectrum.

Attention now shifts to the upcoming Asian session, where Tokyo’s CPI data is set to be released. Core CPI is expected to slow notably from 2.4% to 2.0% in September. BoJ has already communicated its cautious stance on implementing further rate hikes. Cooling inflationary pressures would provide BoJ with additional room to maintain its wait-and-see approach, delaying any further monetary tightening.

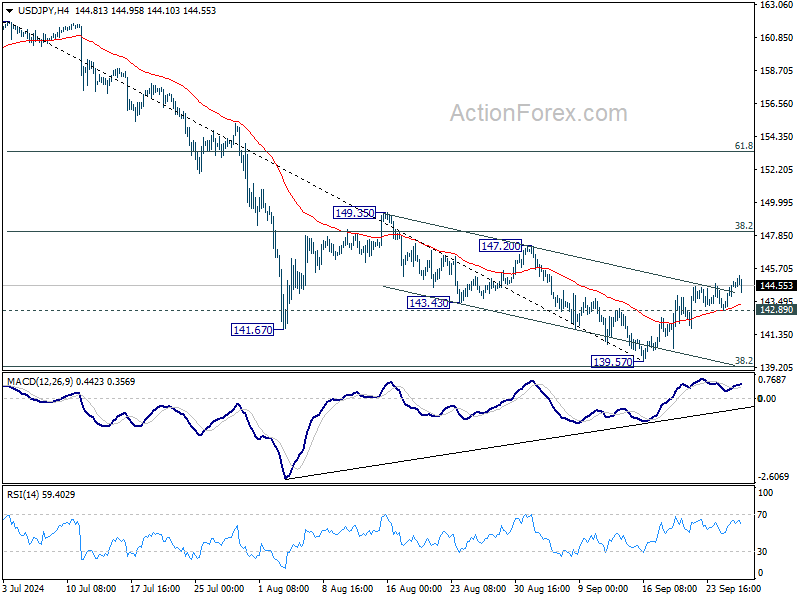

Technically, USD/JPY’s rebound from 139.57 is still expected to continue, despite weak upside momentum, to 38.2% retracement of 161.94 to 139.57 at 148.11. However, break of 142.89 minor support will suggest that the rebound is over and bring retest of 139.57 low.

In Europe, at the time of writing, FTSE is up 0.29%. DAX is up 1.35%. CAC is up 1.94%. UK 10-year yield rose 0.008 to 4.004. Germany 10-year yield is down -0.031 at 2.150. Earlier in Asia, Nikkei rose 2.79%. Hong Kong HSI rose 4.16%. China Shanghai SSE rose 3.61%. Singapore Strait Times fell -0.03%. Japan 10-year JGB yield rose 0.0182 to 0.831.

US durable goods orders flat in Aug ex-transport rises 0.5% mom

US durable goods orders rose 0.0% mom to USD 289.7B in August, much better than expectation of -2.8% mom decline. Ex-transport orders rose 0.5% mom to USD 188.5B, above expectation of 0.1% mom. Ex-defense orders fell -0.2% mom to USD 271.0B. Electrical equipment, appliances, and components, up two of the last three months, drove the increase, USD 0.3 billion or 1.9% mom to USD 14.4B.

US initial jobless claims fall to 218k, vs exp 226k

US initial jobless claims fell -4k to 218k in the week ending September 21, below expectation of 226k. Four-week moving average of initial claims fell -3.5k to 225k.

Continuing claims rose 13k to 1834k in the week ending September 14. Four-week moving average of continuing claims fell -6.5k to 1836k.

German economy set for 2nd year of contraction amid structural challenges

Germany’s economic prospects have deteriorated further as the Joint Economic Forecast Project Group revised its GDP forecasts downward. The group now expects the German economy to contract by -0.1% in 2024, a downgrade from the previously anticipated 0.1% growth.

This adjustment implies that Germany will face two consecutive years of economic contraction, following a projected decline of -0.3% in 2023.

The forecast for 2025 has also been lowered, with GDP growth now expected at 0.8%, down from the earlier estimate of 1.4%. However, a modest recovery is anticipated in 2026, with growth projected to pick up to 1.3%.

Inflation is expected to decline, offering some relief to the economy. After reaching 5.9% last year, inflation is projected to slow to 2.2% this year and stabilize at 2% in both 2025 and 2026.

Geraldine Dany-Knedlik, head of forecasting and economic policy at DIW Berlin, highlighted the challenges facing Germany. She noted that “structural change” is compounding the economic downturn.

Key factors such as decarbonization, digitalization, and demographic shifts, along with intensified competition from Chinese companies, are initiating “structural adjustment processes.” These developments are “dampening the long-term growth prospects” of the German economy, noted Dany-Knedlik.

SNB cuts 25bps, slashes inflation forecasts

SNB lowered its policy rate by 25 basis points to 1.00%, citing that inflationary pressure “has again decreased significantly”, largely driven by the recent appreciation of Swiss Franc. SNB’s statement also indicated that further rate cuts “may become necessary” in the coming quarters to maintain price stability in the medium term.

The revised inflation forecast shows significant downward adjustment compared to June, reflecting factors such as the stronger Swiss franc, lower oil prices, and upcoming electricity price cuts scheduled for January 2025.

The new conditional forecast sees inflation averaging 1.2% in 2024, 0.6% in 2025, and 0.7% in 2026, down from previous estimates of 1.3%, 1.1%, and 1.0%, respectively.

The SNB’s forecast is based on maintaining the policy rate at 1.0% throughout the projection period. The central bank also noted that without today’s rate cut, inflation forecasts would have been even lower.

On the economic growth front, SNB expects “rather modest” performance in the coming quarters due to the recent strengthening of Swiss franc and slower global economic development. It forecasts GDP growth of around 1% for 2024 and 1.5% for 2025.

BoJ minutes show divided views on rate hike timing

Minutes from BoJ’s July meeting reveal a split among policymakers on the pace of future rate hikes. While BOJ raised its short-term interest rate to 0.25% by a 7-2 vote, differing opinions emerged on how quickly further increases should occur.

One member argued that if price trends follow the bank’s outlook, it would be “necessary” to proceed with further tightening. Another suggested that with inflation projected to reach its target by H2 of fiscal 2025, the policy rate should gradually rise toward the neutral rate, estimated at around 1%. This member cautioned against rapid rate increases and favored a “timely and gradual” approach to avoid shocks to the economy.

However, some members expressed concerns about the risks of moving too quickly. One warned that monetary policy normalization should not be an end in itself and urged caution in monitoring the risks tied to policy shifts. Another highlighted that inflation expectations were “not being anchored at 2 percent”, suggesting the need to avoid excessive market speculation about future rate hikes.

The minutes also reflect “high uncertainties regarding the level of the neutral interest rate” about Japan’s neutral interest rate, given the long period without rate hikes. One member noted the difficulty of setting policy based on estimates of the neutral rate, calling for flexibility in adjusting policy based on evolving economic conditions.

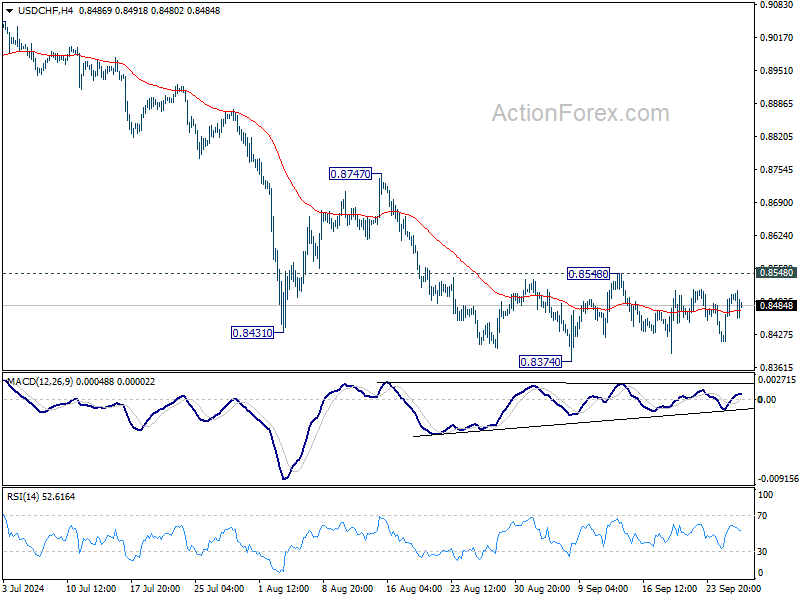

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8444; (P) 0.8475; (R1) 0.8536; More…

USD/CHF is still bounded in range of 0.8374/8548 and intraday bias remains neutral. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, break of 0.8548 resistance will turn bias back to the upside for 0.8747 resistance.

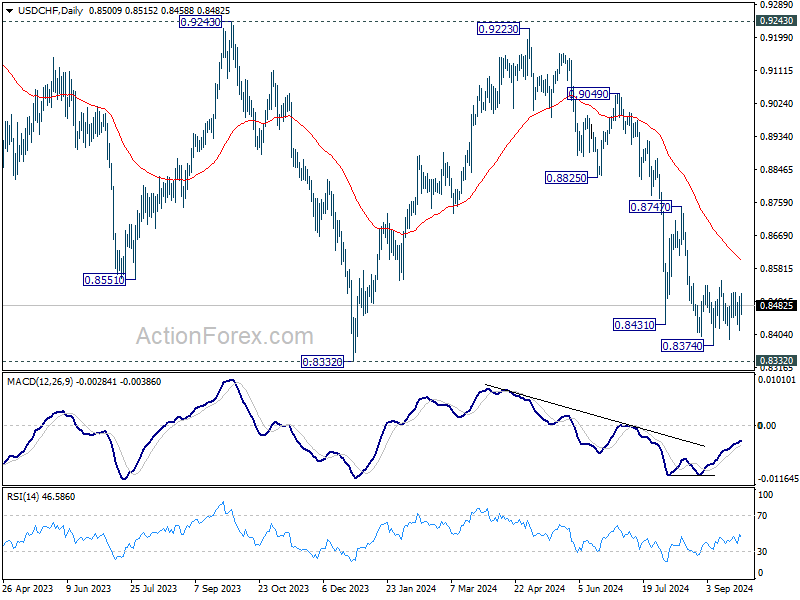

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 06:00 | EUR | Germany GfK Consumer Sentiment Oct | -21.2 | -21 | -22 | -21.9 |

| 07:30 | CHF | SNB Interest Rate Decision | 1.00% | 1.00% | 1.25% | |

| 08:00 | CHF | SNB Press Conference | ||||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Aug | 2.90% | 2.50% | 2.30% | |

| 12:30 | USD | Initial Jobless Claims (Sep 20) | 218K | 226K | 219K | 222K |

| 12:30 | USD | GDP Annualized Q2 F | 3.00% | 3.00% | 3.00% | |

| 12:30 | USD | GDP Price Index Q2 F | 2.50% | 2.50% | 2.50% | |

| 12:30 | USD | Durable Goods Orders Aug | 0.00% | -2.80% | 9.80% | |

| 12:30 | USD | Durable Goods Orders ex Transport Aug | 0.50% | 0.10% | -0.20% | |

| 14:00 | USD | Pending Home Sales M/M Aug | 0.90% | -5.50% | ||

| 14:30 | USD | Natural Gas Storage | 52B | 58B |