Euro is facing significant selling pressure today, with its recent decline gaining momentum. Fresh data from ECB paints a grim picture: bank lending growth in July was notably sluggish, failing to meet even historical averages. Meanwhile, money growth, which had shown signs of improvement in prior months, remained stagnant with M3 increasing by just 2.3% year-over-year.

The prevailing market expectation is that ECB will implement two additional rate cuts this year, in September and December. However, as Germany’s economic woes deepen, with the real threat of a recession on the horizon, speculation is growing that ECB might be forced to consider yet another rate reduction beyond what is currently anticipated.

Meanwhile, Dollar is staging a broad recovery, though its trajectory is likely to be influenced by Nvidia’s earnings and the subsequent impact on overall market sentiment. Despite some market participants betting on a total of 100bps in rate cuts by Fed this year, such expectations is overly ambitious. Unless next week’s non-farm payroll report is unexpectedly weak, Fed is still likely to proceed with a modest 25bps cut at its September meeting.

As the week progresses, Euro is emerging as the weakest performer, followed by Australian Dollar and Japanese Yen. In contrast, Swiss Franc is leading the charge, with Canadian Dollar and New Zealand Dollar also showing relative strength. Dollar and British Pound are positioned somewhere in the middle of the performance spectrum.

Technically, NZD/USD is now at a juncture after breaking through 0.6221 resistance last week. Decisive break of falling trend line resistance will strength the case that consolidation from 0.6537 has already completed. That is, rise form 0.5511 (2022 low) could be ready to resume through 0.6537 in the medium term. Tomorrow’s ANZ business confidence data could be the catalyst needed for the Kiwi to break through the trendline with conviction.

In Europe, at the time of writing, FTSE is down -0.24%. DAX is up 0.73%. CAC is up 0.37%. UK 10-year yield is down -0.0041 at 3.974. Germany 10-year yield is down -0.037 at 2.257. Earlier in Asia, Nikkei rose 0.22%. Hong Kong HSI fell -1.02%. China Shanghai SSE fell -0.40%. Singapore Strait Times fell -0.22%. Japan 10-year JGB yield rose 0.0147 to 0.895.

Australia’s monthly CPI slows to 3.5% in Jul, slightly above expectations

Australia’s monthly CPI inflation slowed from 3.8% yoy in June to 3.5% yoy in July, above the expected 3.4% yoy. CPI excluding volatile items and holiday travel also eased, dropping from 4.0% yoy to 3.7% yoy. Additionally, the annual trimmed mean CPI, a measure that smooths out irregular price fluctuations, decreased from 4.1% yoy to 3.8% yoy.

The most significant contributors to the price increases were housing (+4.0%), food and non-alcoholic beverages (+3.8%), alcohol and tobacco (+7.2%), and transport (+3.4%). These sectors continue to exert upward pressure on inflation, despite the overall slowing trend.

BoJ’s Himino signals readiness for further rate hikes if economic confidence grows

BoJ Deputy Governor Ryozo Himino reaffirmed the central bank’s commitment to adjusting its monetary policy if confidence in the economic outlook strengthens. In a speech, Himino stated that if BoJ gains “growing confidence” in its economic and price forecasts, it “will adjust the degree of monetary accommodation,” signaling readiness for rate hikes ahead.

Himino outlined the baseline scenario for fiscal 2025 and 2026, describing it as a “reasonably balanced state” where inflation aligns with the price stability target, and economic growth “slightly above cruising speed”. However, he cautioned against two risk scenarios: one where inflation remains above 2% and another where it falls well below 2% and fails to recover.

Addressing recent financial market volatility, Himino noted that Yen’s appreciation might ease the import cost pressures faced by small and medium-sized enterprises, though it could reduce yen-denominated profits for export industries. He reassured that Japanese firms have developed competitive strengths. Stock price volatilities, while influential, should not significantly undermine business sentiment.

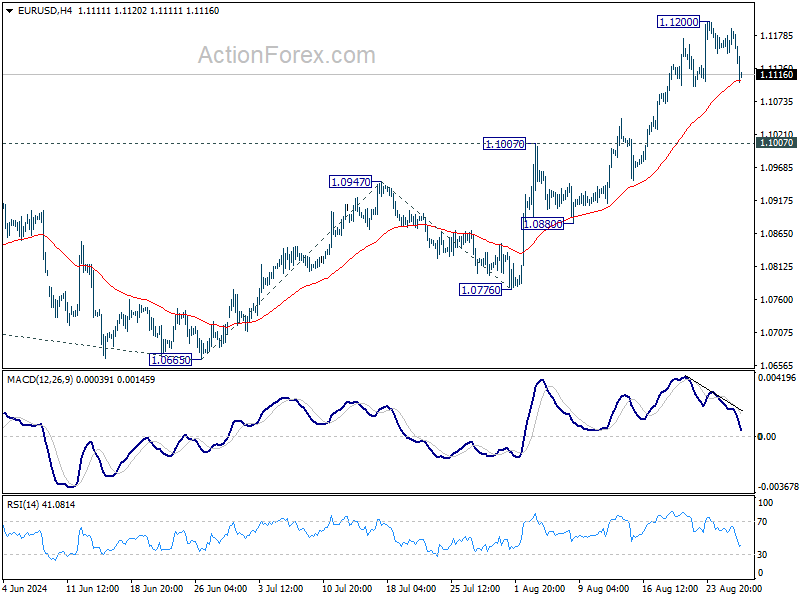

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1160; (P) 1.1175; (R1) 1.1200; More….

EUR/USD’s retreat from 1.1200 extends lower today, but stays well above 1.1007 resistance turned support. Intraday bias remains neutral first and further rally is still in favor. On the upside, break of 1.1200 will resume recent rally to 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232, and then 1.1274 high.

In the bigger picture, break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Construction Work Done Q2 | 0.10% | 0.70% | -2.90% | |

| 01:30 | AUD | Monthly CPI Y/Y Jul | 3.50% | 3.40% | 3.80% | |

| 08:00 | CHF | UBS Economic Expectations Aug | -3.4 | 9.4 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | 2.30% | 2.80% | 2.20% | 2.30% |

| 14:30 | USD | Crude Oil Inventories | -2.7M | -4.6M |