Sterling is making notable gains after UK employment data revealed an unexpected drop in the unemployment rate for June. Additionally, July’s figures showed continued growth in payrolled employment and a rebound in wage growth. This robust set of data strengthens the position of the hawks within BoE’s MPC, who incline to maintain a cautious stance on further interest rate cuts. However, the Pound’s ride may not be smooth this week, with key economic data still to come, including tomorrow’s UK CPI, Thursday’s GDP, and Friday’s retail sales. These upcoming reports could lead to considerable volatility for the currency.

Elsewhere in the forex markets, trading activity remains subdued. Although Yen and Swiss Franc weakened yesterday, there has been no significant follow-through in selling. Euro is also struggling to extend its rebound against Dollar, while commodity currencies are confined to tight ranges. Market participants are now turning their attention to today’s US PPI data, which could spark some brief volatility, but the primary focus remains on tomorrow’s US CPI report.

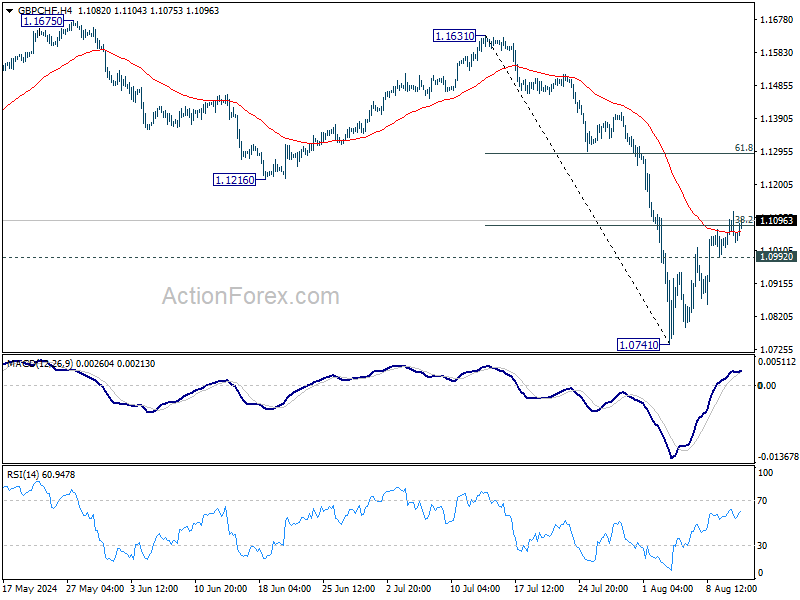

Technically, following up on GBP/CHF, while rebound from 1.0741 extends higher, it’s still struggling to get rid of 38.2% retracement of 1.1631 to 1.0741 at 1.1108 cleanly. Nonetheless, further rise is mildly in favor as long as 1.0992 minor support holds. Sustained trading above 1.1108 will pave the way to 1.1216 support turned resistance. However, break of 1.0092 will retain near term bearishness and bring retest of 1.0741 low next.

In Asia Nikkei closed up 3.45%. Hong Kong HSI is down -0.02%. China Shanghai SSE is down -0.38%. Singapore Strait Times is up 0.72%. Japan 10-year JGB yield fell -0.0041 to 0.854. Overnight, DOW fell -0.36%. S&P 500 rose 0.00%. NASDAQ rose 0.21%. 10-year yield fell -0.033 to 3.909.

UK payrolled employment grows 24k in Jul, unemployment rate falls to 4.2% in Jun

UK payrolled employment rose 24k or 0.1% mom in July. Median monthly pay increased by 5.6% up sharply from June’s 3.8% yoy, but below May’s 6.0% yoy. Claimant count jumped 135k versus expectation of 14.5k.

In the three months to June, unemployment fell from 4.4% to 4.2%, versus expectation of a rise to 4.5%. Average earnings including bonus rose 5.4% yoy, slowed from 5.7% but beat expectation of 4.6%. Average earnings excluding bonus slowed to 4.5% yoy, down from 5.7%, below expectation of 4.6%.

Japan’s PPI rises to 3% yoy as Yen weakness fuels import costs surge

Japan’s Producer Price Index rose by 3.0% yoy in July, aligning with market expectations and slightly up from June’s 2.9% yoy increase. This marks the sixth consecutive month of acceleration and the fastest rate of increase in 11 months.

A significant driver of this rise was the 10.8% yoy increase in yen-denominated costs for imported materials, which accelerated from a revised 10.6% yoy rise in June. This highlights the ongoing impact of the weak Yen on import prices, contributing to higher overall production costs.

On a month-over-month basis, PPI rose by 0.3%, again matching consensus estimates.

Australia’s wage growth slows in 0.8% qoq in Q2, with private sector lagging

Australia’s wage price index rose by 0.8% qoq in Q2, slightly down from the previous quarter’s 0.9% qoq increase and falling short of expectations for another 0.9% qoq rise. On an annual basis, wage growth remained steady at 4.1%, unchanged from Q1.

In the private sector, wage growth slowed to 0.7% qoq, down from 0.9% in the previous quarter. This marks the lowest increase for a second quarter since 2021 and ties for the lowest growth for any quarter since Q4 2021.

On the other hand, public sector wages grew by 0.9% qoq, up from 0.6% previously, making it the strongest June quarter increase since 2012. This stronger rise in the public sector was attributed to the newly synchronized timing of Commonwealth public sector agreement increases.

Australia’s Westpac consumer sentiment edges up amid small relief over steady rates

Australia’s Westpac Consumer Sentiment Index saw a modest increase of 2.8% mom in August, rising from 82.7 to 85.0. Westpac attributed this uptick to a “small sigh of relief” from consumers after RBA decided to keep interest rates unchanged, coupled with the positive effects of tax cuts and other fiscal measures.

However, despite the rise, the index remains historically weak, hovering within the 78–86 range that has persisted for over two years. Westpac’s analysis highlighted ongoing concerns among consumers about the cost of living and potential future rate hikes, which continue to “weigh heavily” on sentiment.

Looking ahead to RBA’s next meeting on September 23-24, Westpac noted that data flow leading up to the meeting is unlikely to provide significant new insights into inflation trends. With RBA having already ruled out near-term rate cuts, it is expected that the central bank will maintain its current interest rate at the upcoming meeting.

Looking ahead

Germany will release ZEW economic sentiment in European session. Later in the day, US PPI will take center stage.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2743; (P) 1.2769; (R1) 1.2790; More…

GBP/USD’s rebound from 1.2664 extends higher today but stays below 1.2839 resistance. Intraday bias stays neutral for the moment. On the downside, break of 1.2664 will resume the fall from 1.3043 to 1.2612 support. Decisive break there should confirm that rise from 1.2298 has completed, and target this support next. However, break of 1.2839 resistance will argue that the pull back from 1.3043 has completed and turn bias back to the upside.

In the bigger picture, current development suggests that corrective pattern from 1.3141 is extending with fall from 1.3043 as another leg. Break of 1.2612 support would strengthen this case. But still, downside should be contained by 1.2036/2298 support zone even in case of deep decline. Rise from 1.0351 (2022 low) remains in favor to resume at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jul | 3.00% | 3.00% | 2.90% | |

| 00:30 | AUD | Westpac Consumer Confidence Aug | 2.80% | -1.10% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q2 | 0.80% | 0.90% | 0.80% | 0.90% |

| 01:30 | AUD | NAB Business Conditions Jul | 1.00% | 4 | ||

| 01:30 | AUD | NAB Business Confidence Jul | 6 | 4 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jul | -2.10% | 9.70% | ||

| 06:00 | GBP | Claimant Count Change Jul | 135.0K | 14.5K | 32.3K | 36.2K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 4.20% | 4.50% | 4.40% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 5.40% | 4.60% | 5.70% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 4.50% | 4.60% | 5.70% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Aug | 30.6 | 41.8 | ||

| 09:00 | EUR | Germany ZEW Current Situation Aug | -68.9 | |||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | 35.4 | 43.7 | ||

| 10:00 | USD | NFIB Business Optimism Index Jul | 91.7 | 91.5 | ||

| 12:30 | USD | PPI M/M Jul | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Y/Y Jul | 2.30% | 2.60% | ||

| 12:30 | USD | PPI ex Food & Energy M/M Jul | 0.20% | 0.40% | ||

| 12:30 | USD | PPI ex Food & Energy Y/Y Jul | 2.70% | 3.00% |