Risk aversion is the prevailing theme in the global markets today, with major European indexes trading in the red and US futures pointing to a lower open. Australian Dollar reversed its earlier post-CPI gains and is currently the worst performer of the day, followed by New Zealand Dollar and Canadian Dollar. In contrast, Swiss Franc is the strongest, followed by Euro and the US Dollar, while Japanese Yen and British Pound are positioned in the middle.

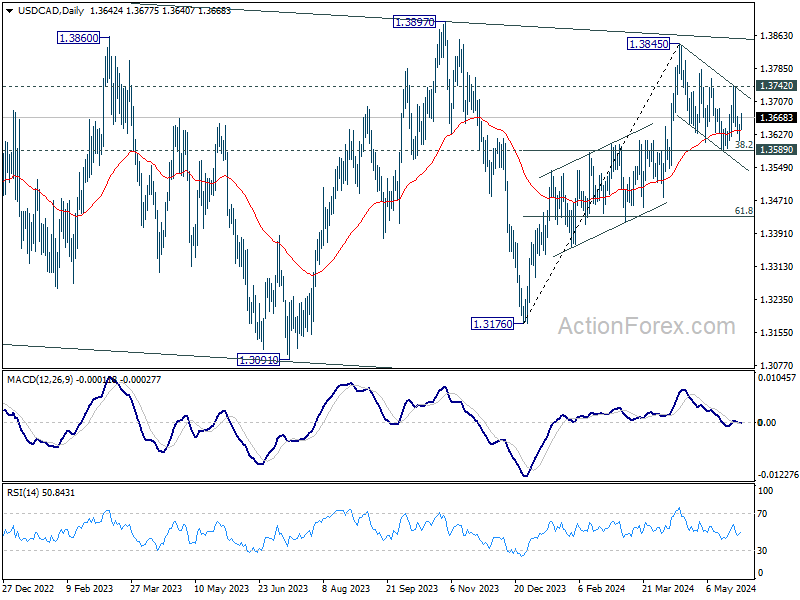

Technically, USD/CAD failed to sustain below 55 D EMA again, and recovered ahead of 1.3589 cluster support (38.2% retracement of 1.3176 to 1.3845). Near term bullishness is maintained thus far. Break of 1.3742 resistance will argue that corrective pullback from 1.3845 has completed already, and larger rise from 1.3176 is ready to resume. Let’s see if Friday’s US PCE inflation data could trigger the move.

In Europe, at the time of writing, FTSE is down -0.50%. DAX is down -1.05%. CAC is down -1.42%. UK 10-year yield is up 0.072 at 4.353. Germany 10-year yield is up 0.045 at 2.641. Earlier in Asia, Nikkei fell -0.77%. Hong Kong HSI fell -1.83%. China Shanghai SSE rose 0.05%. Singapore Strait Times fell -0.21%. Japan 10-year JGB yield rose 0.0403 to 1.080.

German Gfk consumer sentiment jumps to -20.9, falling inflation and wages increase

Germany’s GfK Consumer Sentiment index for June improved significantly, rising from -24.0 to -20.9 and surpassing expectations of -22.5. This marks the fourth consecutive month of improved sentiment.

In May, economic expectations jumped from 0.7 to 9.8, while income expectations rose from 10.7 to 12.5, the highest level since January 2022. Willingness to buy edged up slightly from -12.6 to -12.3, and willingness to save dropped sharply from 14.9 to 5.0, the lowest value since August 2023.

Rolf Bürkl, consumer expert at NIM, explained that “falling inflation rates combined with considerable wage and salary increases strengthen consumer purchasing power. This stimulates income expectations and also reduces consumer uncertainty, which was responsible for the comparatively high willingness to save in previous months.”

Despite these positive trends, Bürkl noted that uncertainty still lingers among German consumers. This is attributed to the lack of clear future prospects in the country, which undermines planning certainty for significant purchases. “People will have to regain this certainty before they are willing to invest their growing purchasing power in larger purchases,” he added.

BoJ’s Adachi: Yen depreciation could prompt earlier rate hike

BoJ board member Seiji Adachi has signaled that the central bank could raise interest rate earlier if depreciation of Yen accelerates or persists.

In his speech today, Adachi emphasized the need to avoid premature rate increases. However, he also warned that an excessive focus on downside risks could lead to an inflation spike, necessitating sharp monetary tightening later on.

Adachi highlighted the importance to “gradually adjust” monetary support based on economic, price, and financial developments, as long as underlying inflation trends toward 2% target.

He projected that consumer inflation will re-accelerate from summer through autumn due to rising import costs and sustained wage gains. However, if Yen’s decline accelerates or persists, “consumer inflation could rebound sooner than expected”.

“If this happens at a time when there is a higher chance of inflation durably and stably exceeding 2%, we may need to push forward the timing of an interest rate hike,” Adachi noted.

Australia’s April CPI rises to 3.6%, driven by housing and food costs

Australia monthly CPI rose form 3.5% yoy to 3.6% yoy in April, exceeding the expectation of 3.4%. This marks the second consecutive month of rising inflation. CPI excluding volatile items and holiday travel remained steady at 4.1% yoy, while the trimmed mean CPI also edged up from 4.0% yoy to 4.1% yoy.

Significant price increases were observed in several categories: Housing saw a 4.9% rise, Food and non-alcoholic beverages increased by 3.8%, Alcohol and tobacco prices surged by 6.5%, and Transport costs went up by 4.2%.

Australia’s Westpac Leading Index rises to -0.01%, some signs of stabilization

Australia Westpac Leading Index improved slightly in April, rising from -0.08% to -0.01%. Westpac noted that the index is once again indicating some stabilization in growth momentum. However, the improvement in growth is expected to be modest.

Westpac forecasts GDP to grow at an annual pace of 1.9% in the second half of the year, up from 1.3% in the first half. Despite this uptick, the growth rate remains below Australia’s trend, which is estimated to be around 2.5% per year with some moderation in population growth.

New Zealand ANZ business confidence falls to 11.2, inflation pressures ease

New Zealand’s ANZ Business Confidence index dropped from 14.9 to 11.2 in May, signaling a decline in business sentiment. Outlook for own activity also decreased from 14.3 to 11.8.

Cost expectations saw a reduction 76.7 to 72.6, the lowest since February 2021. Wage expectations ticked down slightly from 75.5 to 75.4. Profit expectations fell sharply, from -9.8 to -15.3, and pricing intentions decreased from 46.9 to 41.6, the lowest level since December 2020. Inflation expectations edged down from 3.76% to 3.59%.

According to ANZ, “This month’s Business Outlook survey makes for grim reading, but it also provides confirmation that inflation pressures are waning.”

They indicated that significant progress in reducing non-tradable inflation is anticipated, which, barring any unforeseen inflationary spikes, should restore RBNZ’s confidence. This would potentially allow for future rate cuts, signaling a cautiously optimistic outlook on inflation control and economic stability.

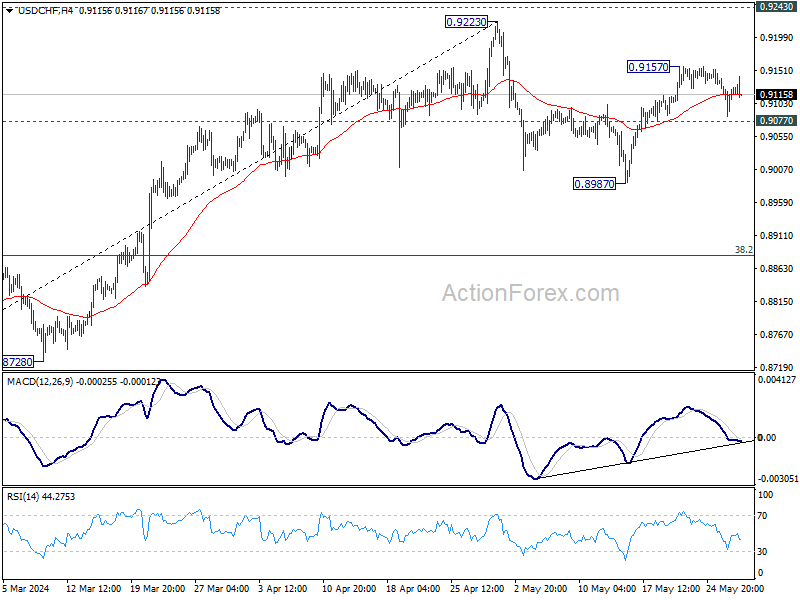

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9091; (P) 0.9120; (R1) 0.9153; More….

Range trading continues in USD/CHF below 0.9157 and intraday bias stays neutral. Further rally is in favor with 0.9077 minor support intact. On the upside, above 0.9157 will bring retest of 0.9223. However, on the downside, break of 0.9077 will suggest that rebound from 0.8987 has completed. Intraday bias will be turned back to the downside for 0.8987 support. Further break there will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

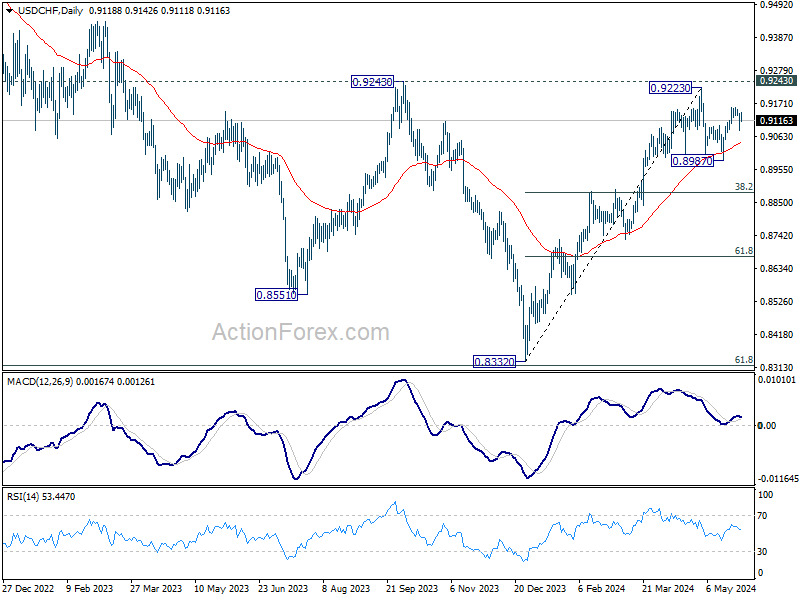

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Apr | 0.00% | -0.10% | ||

| 01:00 | NZD | ANZ Business Confidence May | 11.2 | 14.9 | ||

| 01:30 | AUD | Construction Work Done Q1 | -2.90% | 0.50% | 0.70% | 1.80% |

| 01:30 | AUD | Monthly CPI Y/Y Apr | 3.60% | 3.40% | 3.50% | |

| 05:00 | JPY | Consumer Confidence May | 36.2 | 38.9 | 38.3 | |

| 06:00 | EUR | Germany GfK Consumer Confidence Jun | -20.9 | -22.5 | -24.2 | -24 |

| 08:00 | CHF | UBS Economic Expectations May | 18.2 | 17.6 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 1.30% | 1.50% | 0.90% | |

| 12:00 | EUR | Germany CPI M/M May P | 0.10% | 0.20% | 0.50% | |

| 12:00 | EUR | Germany CPI Y/Y May P | 2.40% | 2.40% | 2.20% | |

| 18:00 | USD | Fed’s Beige Book |