Canadian Dollar sees a broad decline in early US session due to growing speculation about rate cut by BoC in the near future. April’s headline CPI slowed as expected, despite a significant increase in gasoline prices. Core inflation measures also showed more progress in disinflation than anticipated. While it remains uncertain if this progress will be enough to prompt BoC to ease policy at next meeting, speculation is likely to intensify ahead of June 5 meeting.

Meanwhile, New Zealand Dollar followed Loonie as the second weakest performer of the day. Attention is now turning to RBNZ rate decision scheduled for tomorrow, with most market participants expecting the central bank to hold the rate steady at 5.50%. While many analysts see November as the likely timing for the first rate cut, this view is not universally held. The upcoming OCR forecasts from RBNZ will be closely scrutinized, particularly to see if they adjust to remove the possibility of another rate hike. However, it remains uncertain whether RBNZ will move up the timeline for the first rate cut from next year.

Elsewhere in the currency markets, Dollar is currently the third weakest. Swiss Franc has emerged as the strongest performer, followed the British Pound and Australian Dollar. Euro and Japanese Yen are positioned in the middle of the performance spectrum.

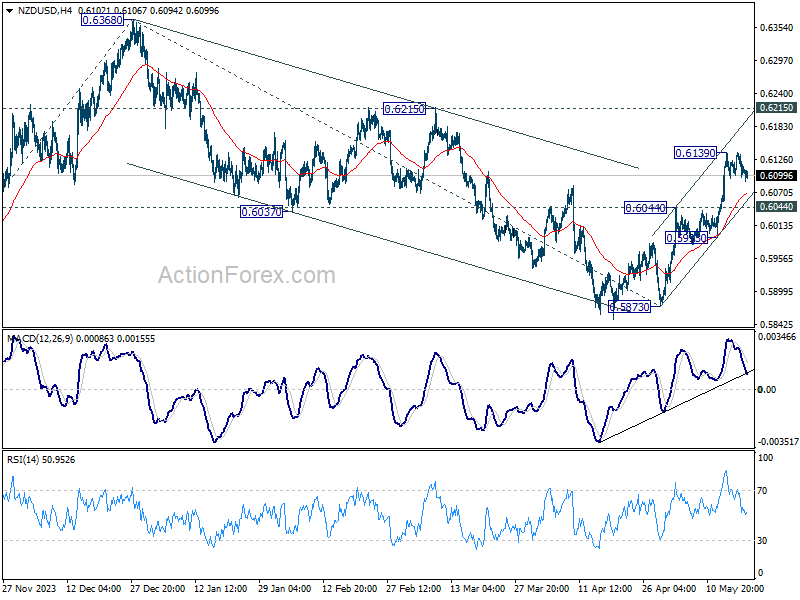

Technically, NZD/USD turned sideway after rebounding to 0.6139, but the retreat is so far shallow. Further rise is expected as long as 0.6044 resistance turned support holds. Above 0.6139 will resume the rally from 0.5873 to 0.6215 resistance. Decisive break there should confirm that whole corrective fall from 0.6368 has completed at 0.5873 already, and bring retest of 0.6368 next.

In Europe, at the time of writing, FTSE is down -0.42%. DAX is down -0.53%. CAC is down -1.06%. UK 10-year yield is down -0.029 at 4.147. Germany 10-year yield is down -0.0168 at 2.518. Earlier in Asia, Nikkei fell -0.31%. Hong Kong HSI fell -2.12%. China Shanghai SSE fell -0.42%. Singapore Strait Times fell -0.19%. Japan 10-year JGB yield rose 0.0051 to 0.985.

Canada’s CPI falls to 2.7% in Apr, matches expectations

Canada’s CPI slowed from 2.9% yoy to 2.7% yoy in April, matched expectations. Ex-gasoline, CPI slowed from 2.8% yoy to 2.5% yoy. Gasoline prices accelerated from 4.5% yoy to 6.1% yoy. Food prices slowed from 1.9% yoy to 1.4% yoy. On a monthly basis CPI rose 0.5% mom, matched expectations.

Looking at the core measures, CPI median slowed from 2.9% yoy to 2.6% yoy, below expectation of 2.7% yoy. CPI trimmed slowed from 3.2% yoy to 2.9% yoy, matched expectations. CPI common slowed from 2.9% yoy to 2.6% yoy, below expectation of 2.8% yoy.

IMF recommends BoE cut rates by 50-75 bps in 2024

IMF issued a report today suggesting that with UK inflation currently 2% above its neutral rate estimate, BoE should consider moving towards monetary easing.

IMF highlighted the risks of “delayed easing”, cautioning that while BoE emphasizes the need to wait for clearer signs of reduced inflation persistence, holding off too long could be detrimental.

Additionally, keeping the Bank Rate unchanged as inflation and inflation expectations decrease would “raise ex-post real rates”, which could hinder or even reverse the economic recovery. This scenario might lead to “extended undershooting of the inflation target”.

To address these concerns, IMF recommends that BoE implement rate cuts totaling 50-75 basis points in 2024. This would help balance the risks of premature easing against the need to support economic growth and ensure inflation remains on target.

Eurozone goods exports down -9.2% yoy in Mar, imports down -12.0% yoy

Eurozone goods exports fell -9.2% yoy to EUR 245.5B in March. Goods imports fell -12.0% yoy to EUR 221.3B. Trade balance recorded EUR 24.1B surplus. Intra-Eurozone trade fell -12.4% yoy to EUR 222.1B.

In seasonally adjusted term, goods exports rose 0.1% mom to EUR 237.7B. Goods imports fell -0.1% mom to EUR 220.4B. Trade surplus widened slightly from EUR 16.7B to 17.3B. Intra-Eurozone trade fell -0.5% mom to EUR 213.7B.

RBA minutes highlight debate over rate hike

RBA minutes from May 7 meeting reveal that a rate hike was considered but ultimately, the decision was made to hold cash rate target steady at 4.35%. The board emphasized that recent data indicated that “risks around inflation had risen somewhat,” acknowledging the considerable uncertainty and the difficulty in “ruling in or ruling out” future changes in interest rate.

The minutes detailed that raising the cash rate could be appropriate if the board believed that the staff forecasts were “overly optimistic” about the forces driving down inflation, leaving the balance of risks tilted to the upside. Additionally, a higher cash rate might be necessary even with ongoing weakness in aggregate demand if “other factors slowed the pace of disinflation.”

Conversely, the decision to hold the cash rate steady was based on the view that, although there had been significant updates on the economy since the last meeting, these updates were “not sufficient to warrant a change in the stance of monetary policy.” Inflation was still declining towards the target, and the new information “did not materially alter its trajectory.”

Australian Westpac consumer sentiment falls -0.3% mom amid budget disappointment

Australia Westpac Consumer Sentiment index fell by -0.3% mom to 82.2 in May. Westpac highlighted that the primary takeaways from the May survey are “no let-up in the weak consumer environment” and the cautious mindset of consumers. Consumers are more inclined to use funds from fiscal measures to repair their finances rather than go on spending sprees, which aligns with RBA’s efforts to bring inflation back to target.

The May survey, conducted during budget week, provided a clear comparison of sentiment before and after the budget announcement. Sentiment among those surveyed before the budget was relatively optimistic, with an index reading of 86.8, marking a 5.3% increase from April. However, sentiment plummeted to 76.6 after the budget announcement, reflecting a 7% decline from April. This -11.8% drop in sentiment post-budget contrasts with a -7.4% decline observed last year.

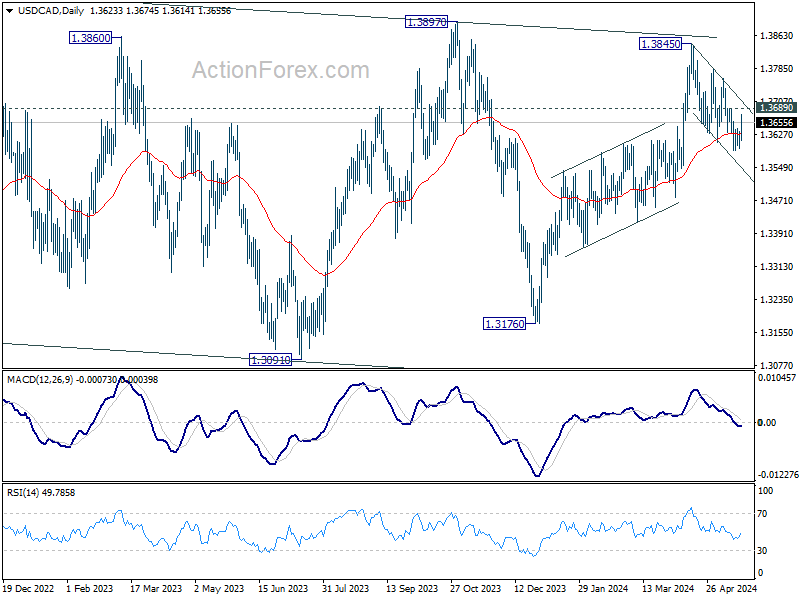

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3602; (P) 1.3618; (R1) 1.3641; More…

USD/CAD recovered notably today but stays below 1.3689 resistance. Intraday bias stays neutral first. Strong bounce from current level will confirm support by 55 D EMA (now at 1.3628). Break of 1.3689 minor resistance will argue that correction from 1.3845 has completed, and bring stronger rally to 1.3761 resistance. However, sustained break of 55 D EMA will argue that whole rise from 1.3176 has completed already, and turn outlook bearish.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence May | -0.30% | -2.40% | ||

| 01:30 | AUD | RBA Minutes | ||||

| 06:00 | EUR | Germany PPI M/M Apr | 0.20% | 0.10% | 0.20% | |

| 06:00 | EUR | Germany PPI Y/Y Apr | -3.30% | -3.20% | -2.90% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Mar | 35.8B | 30.2B | 29.5B | 28.9B |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | 17.3B | 19.9B | 17.9B | 16.7B |

| 12:30 | CAD | CPI M/M Apr | 0.50% | 0.50% | 0.60% | |

| 12:30 | CAD | CPI Y/Y Apr | 2.70% | 2.70% | 2.90% | |

| 12:30 | CAD | CPI Median Y/Y Apr | 2.60% | 2.70% | 2.80% | 2.90% |

| 12:30 | CAD | CPI Trimmed Y/Y Apr | 2.90% | 2.90% | 3.10% | |

| 12:30 | CAD | CPI Common Y/Y Apr | 2.60% | 2.80% | 2.90% |