Asian markets kicked off the week on a positive note, buoyed by the record-breaking rally in US markets last week. Despite escalating geopolitical tensions in the Middle East, which have spurred strong rallies in metals, stock investors appear relatively calm. Trading activity today may be muted due to bank holidays in several European countries and Canada, along with an empty US economic calendar. However, market participants will be paying close attention to comments from BoE MPC member Ben Broadbent and several Fed officials. Later in the week, volatility is expected to rise with RBNZ rate decision, RBA and Fed minutes as well as key CPI and PMI data from several countries.

In the currency markets, Australian Dollar is currently leading the pack, followed by Euro and Canadian Dollar. Conversely, New Zealand Dollar is the weakest performer, likely due to caution ahead of RBNZ rate decision. Dollar and Japanese Yen are also lagging, with Swiss Franc not far behind. This pattern aligns with the prevailing risk-on sentiment in the markets.

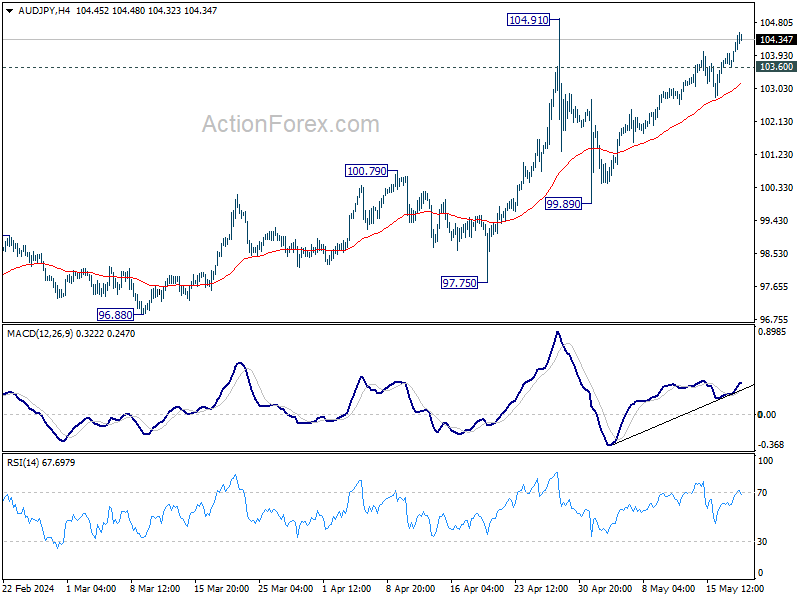

Technically, AUD/JPY’s rally from 99.89 continues today and it’s in progress for retesting 104.91 high. Resistance could be seen there to limit upside. Break of 103.60 minor support will turn intraday bias neutral first. Sustained break of 55 4H EMA (now at 103.17) will argue that the corrective pattern from 104.91 has started the third leg, and bring deeper fall back towards 99.89. However, decisive break of 104.91 will confirm larger up trend resumption instead.

In Asia, Nikkei rose 0.73%. Hong Kong HSI is up 0.61%. China Shanghai SSE is up 0.54%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.0256 at 0.978.

China holds rates steady amidst property sector support measures

China kept its benchmark lending rates unchanged at today’s monthly fixing, aligning with market expectations. One-year Loan Prime Rate remained at 3.45%, while Five-year LPR stayed at 3.95%. This decision follows the People’s Bank of China’s move last week to maintain a key policy rate at 2.50% while rolling over maturing medium-term lending facilities.

Additionally, China announced on Friday a series of measures to stabilize its crisis-hit property sector, including the central bank facilitating CNY 1T in extra funding and easing mortgage rules. This strong supportive policy rollout has increased the likelihood of further monetary easing in the coming months.

Some economists now expect one or two cuts to LPR later this year, alongside a reduction in the reserve requirement ratio. These anticipated measures aim to bolster the property sector and sustain economic growth amid ongoing challenges.

Gold soars to record on geotensions, Silver rallies too

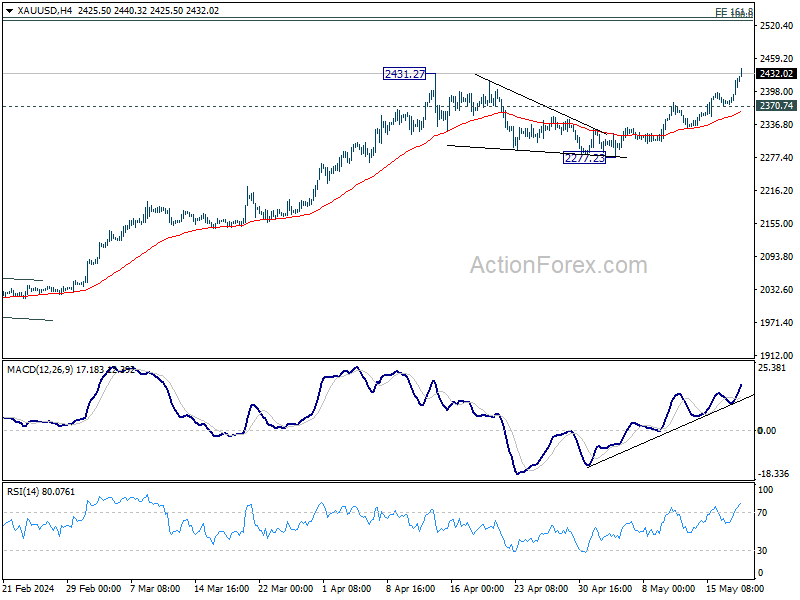

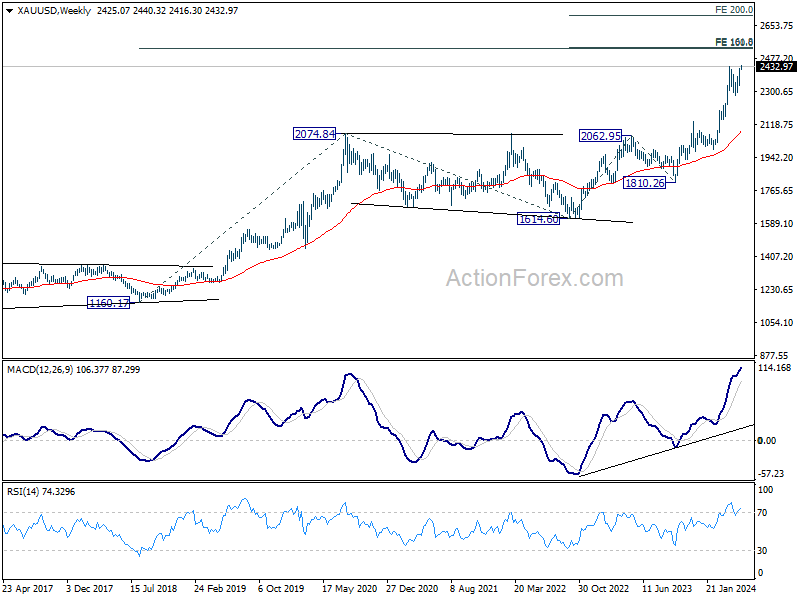

Gold reached a new record high today, fueled by escalating geopolitical tensions in the Middle East and the prospect of easing policies from major central banks this year. Investors are flocking to the safe-haven asset following a series of unsettling events. On Sunday, a helicopter carrying Iranian President Ebrahim Raisi crashed in dense fog, heightening regional instability. Additionally, a China-bound oil tanker was hit by a Houthi missile in the Red Sea on Saturday, further exacerbating tensions. The anticipated shift towards more accommodative monetary policies by global central banks is also reducing the opportunity cost of holding Gold, providing further support for its rally.

Technically, strong resistance could emerge at around 2500 to limit Gold’s up trend, at least on first attempt. There lies 161.8% projection of 1614.60 to 2062.95 from 1810.26 at 2535.69, and 100% projection of 1160.17 to 2074.84 at 1614.60 at 2529.27.

However, decisive break of 2500 would set the stage for 200% projection of 1614.60 to 2062.95 from 1810.26 at 2706.96 next. In any case, near term outlook will stay bullish as long as 2370.74 support holds.

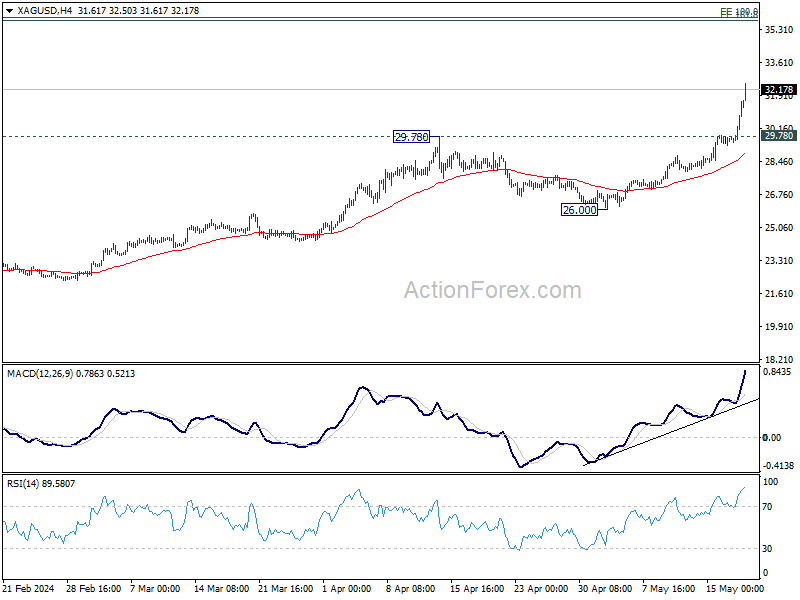

Silver is also in strong rally at this point. Near term outlook will stay bullish as long as 29.78 resistance turned support holds. Next target is cluster projection level at 35.80/94, 161.8% projection of 17.54 to 26.12 from 21.92 at 35.80 and 100% projection of 11.67 to 30.07 from 17.54 at 35.94.

RBNZ; RBA and FOMC Minutes; CPIs and PMIs

Several key central bank activities will take center stage this week, along with consumer inflation data and PMIs from several major economies.

RBNZ rate decision is widely expected to keep OCR unchanged at 5.50%. Investors and analysts will be particularly interested in the new Monetary Policy Statement for any changes in its OCR forecasts. Previously, the forecasts suggested 40% probability of a rate hike in Q3, followed by the first rate cut in Q2 2025. The upcoming statement may adjust these probabilities, with prospects of eliminating the chance of another hike, though it may stop short of advancing the timeline for the first rate cut.

Attention will also be directed towards the minutes from RBA and FOMC meetings. RBA has maintained a flexible stance, by not ruling anything in and out. Market observers will scrutinize the minutes for any indications of how inclined (or not) the board towards a rate hike. As for FOMC minutes, market will look for further evidence to rule out the chance of another rate hike. Regarding the first Fed rate cut, it’s too early for the minutes to tell whether September is the timing.

Additionally, inflation data from Canada, the UK, and Japan will be closely watched. For BoE and BoC, substantial decline in inflation is necessary before considering a rate cut in June. If inflation remains elevated, BoE might look to August, and the BoC to July, for potential rate adjustments.

Other significant economic indicators to monitor include durable goods orders from the US and retail sales data from Canada, the UK, and New Zealand. PMIs from Australia, Japan, Eurozone, the UK, and the US will also provide valuable insights.

Here are some highlights for the week:

- Monday: Japan tertiary industry index.

- Tuesday: Australia Westpac consumer sentiment, RBA minutes; Eurozone current account, trade balance; Canada CPI.

- Wednesday: Japan machine orders, trade balance; RBNZ rate decision; UK CPI, PPI; US existing home sales.

- Thursday: New Zealand retail sales; Australia PMIs, inflation expectations; Japan PMIs; Eurozone PMIs; UK PMIs; US jobless claims, PMIs, new home sales.

- Friday New Zealand trade balance; Japan CPI; UK consumer confidence, retail sales; Canada retail sales; US durable goods orders.

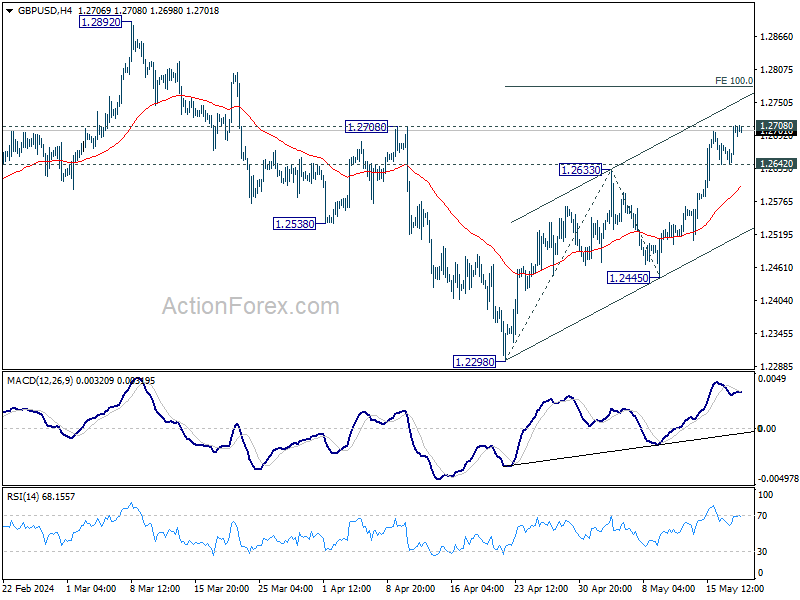

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2660; (P) 1.2686; (R1) 1.2727; More…

Intraday bias in GBP/USD remains on the upside for the moment. Firm break of 1.2708 resistance will extend the rise from 1.2298 to 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780. On the downside, below 1.2642 minor support will turn intraday bias neutral again. But further rise will now remain in favor as long as 1.2445 support holds, in case of retreat.

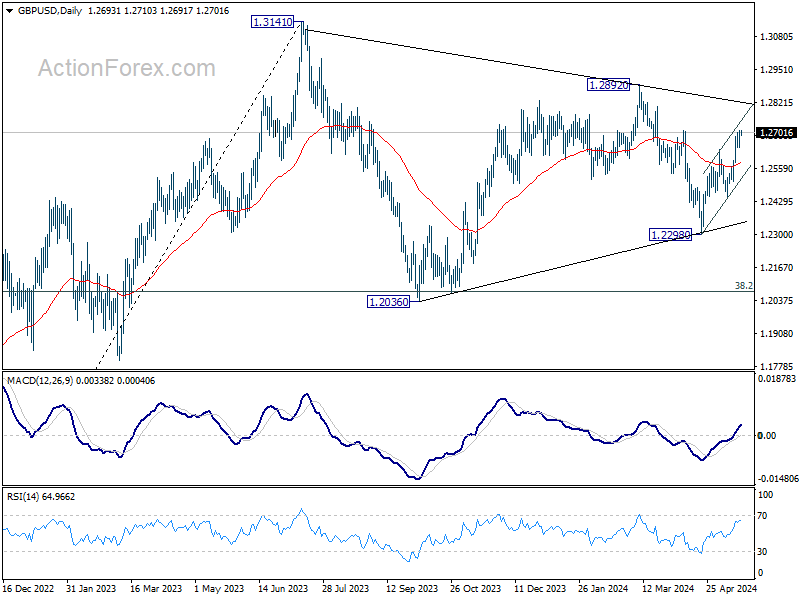

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:15 | CNY | PBoC 1-y Loan Prime Rate | 3.45% | 3.45% | 3.45% | |

| 01:15 | CNY | PBoC 5-y Loan Prime Rate | 3.95% | 3.95% | 3.95% | |

| 04:30 | JPY | Tertiary Industry Index M/M Mar | -2.40% | 0.10% | 1.50% |