Fresh selling is seen in Yen and Dollar in early US session, as the markets are going through a quiet day. There is no immediate fundamental catalyst identified for these movements. Traders might be repositioning ahead of significant US economic data releases scheduled for later in the week. Producer Price Index on Tuesday will offer early insights into upstream inflation, but the primary focus remains on Wednesday’s Consumer Price Index release.

Meanwhile, Australian Dollar is trading as the strongest performer, dismissing weak business conditions data. Aussie is set to face its own pivotal moment with the release of employment data on Thursday. Euro and Sterling follow as the second and third strongest currencies, respectively, with traders looking forward to German ZEW economic sentiment data and UK employment figures due tomorrow. New Zealand Dollar turn mixed, recovering from earlier selloff, while Canadian Dollar and Swiss Franc are mixed in the middle.

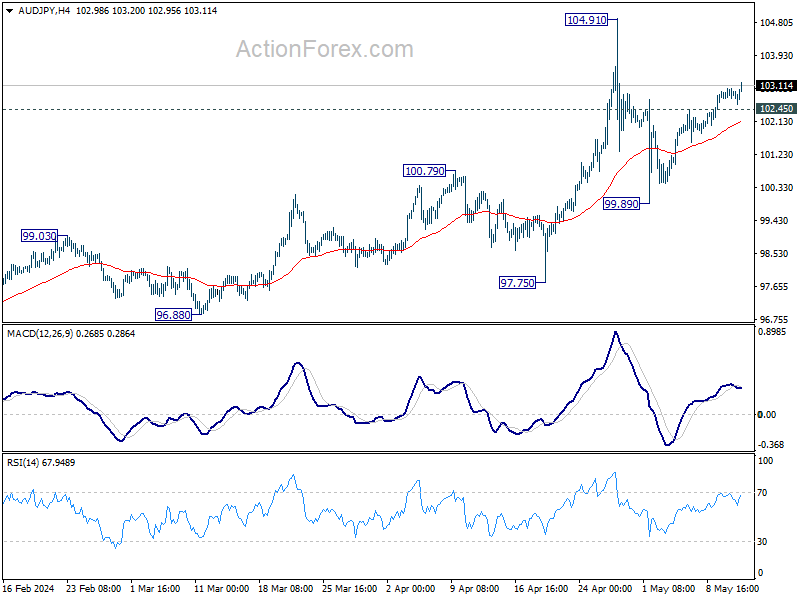

Technically, AUD/JPY’s rebound continues today. Further rally is in favor as long as 102.45 minor support holds, despite loss of upside momentum as seen in 4H MACD. Rise from 99.89 is seen as the second leg of the corrective pattern from 104.91. Hence, upside should be capped by this resistance. On the downside, break of 102.45 will argue that the pattern has already started the third leg for 99.89 support.

In Europe, at the time of writing, FTSE is down -0.21%. DAX is down -0.25%. CAC is down -0.24%. UK 10-year yield is down -0.0335 at 4.140. Germany 10-year yield is down -0.302 at 2.494. Earlier in Asia, Nikkei fell -0.13%. Hong Kong HSI rose 0.80%. China Shanghai SSE fell -0.21%. Singapore Strait Times rose 0.39%. Japan 10-year JGB yield rose 0.0315 to 0.941.

China launches ultra-long bond sale

China’s Ministry of Finance announced it will commence the sale of the first batch of a significant issuance of ultra-long special sovereign bonds this week, with plans to distribute CNY 1T across various tenors ranging from 20 to 50 years.

The ministry detailed that 30-year bonds would be issued in twelve tranches stretching from May 17 to November 15. Additionally, 20-year bonds will begin selling in seven phases starting May 24. 50-year bonds are scheduled for issuance in three parts, also commencing on May 17.

China’s Premier Li Qiang has emphasized the importance of these bonds in supporting the execution of major national strategies and enhancing security capabilities in critical sectors, as reported by state media.

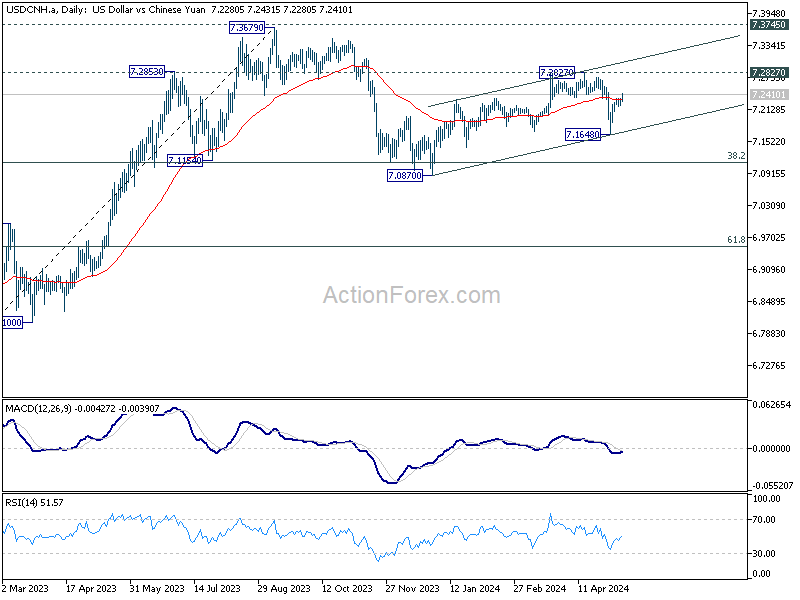

USD/CNH resumed the rebound from 7.1648 today, and the break of 55 D EMA argues that pull back from 7.2827 has completed already. Retest of 7.2827 will resume whole rise from 7.0870, as the second leg of the corrective pattern from 7.3679.

RBNZ survey shows moderating short-term inflation expectations

According to RBNZ Business Expectations Survey for Q2, respondents have lowered their expectations for CPI inflation in both the short-term and medium-term, while their long-term CPI inflation expectations have remained stable.

Specifically, one-year-ahead annual inflation expectations have notably decreased by 49 bps, moving from 3.22% to 2.73%. Two-year-ahead inflation expectations also saw a decline from 2.50% to 2.33%. Five-year-ahead inflation expectations are holding steady at 2.25%. Ten-year-ahead expectations edged up slightly by 3bps, from 2.16% to 2.19%.

Regarding the Official Cash Rate, survey respondents anticipate that it to 5.46% by the end Q2, similar to current rate at 5.50%. Looking further ahead, they forecast a reduction in OCR to 4.79% by the end of Q1 2025, marking a slight increase from last quarter’s prediction of 4.74%. These expectations align with anticipation of approximately three rate cuts by the end of Q1 next year.

NZ BNZ services dips to 47.1, lowest since early 2022

New Zealand’s BusinessNZ Performance of Services Index ticked down from 47.2 to 47.1 in April, marking the lowest level since January 2022.

Breaking down the components of the index reveals mixed signals: Activity and sales saw a modest improvement, rising from 44.8 to 46.5. However, employment took a downturn, dropping from 49.9 to 47.1, recording its lowest level since February 2022. New orders and business also declined slightly to 47.1, from 47.9. Stocks and inventories remained unchanged at 46.6, while supplier deliveries worsened, falling from 48.6 to 47.6—the lowest since November 2022.

The feedback from businesses has increasingly skewed negative, with 66.3% of comments in April being pessimistic, up from 63.0% in March and 57.3% in February. Many respondents highlighted the difficult economic environment and persistent inflationary pressures as significant concerns.

Doug Steel, a senior economist at BNZ, commented on the broader implications of these figures, stating, “combining today’s weak PSI with last week’s PMI yields a composite reading that would be consistent with GDP tracking below year earlier levels into the middle of this year.” He further noted that the combined index suggests there could be “some downside risk” to their current economic forecasts.

Australia’s NAB business confidence steady at 1, conditions normalize with slowing cost growth

Australia’s NAB Business Confidence held steady at 1 in April. Business Conditions index fell from from 9 to 7. Notably, trading conditions declined from 15 to 12, while profitability was unchanged at 6. A significant reduction was observed in employment conditions, which dropped from 6 to 2.

NAB Chief Economist Alan Oster reflected on these figures: “All three components of business conditions were back at their long-run averages in April.” He described this as a milestone, marking a normalization after the unusually high levels of 2022, “reflecting slowing economic growth.”

Labour cost growth decreased to 1.5% from 1.7%, and purchase cost growth slowed to 1.2% from 1.5%. Meanwhile, product price growth rose slightly to 0.9% from 0.7%. Retail price growth moderated significantly to 0.9% from 1.4%.

Oster noted, “There was some further improvement in the pace of cost growth in April, and a step down in the pace of retail price growth.” He suggested these changes could indicate easing in inflation in the second quarter, though further observation is needed to confirm this trend.

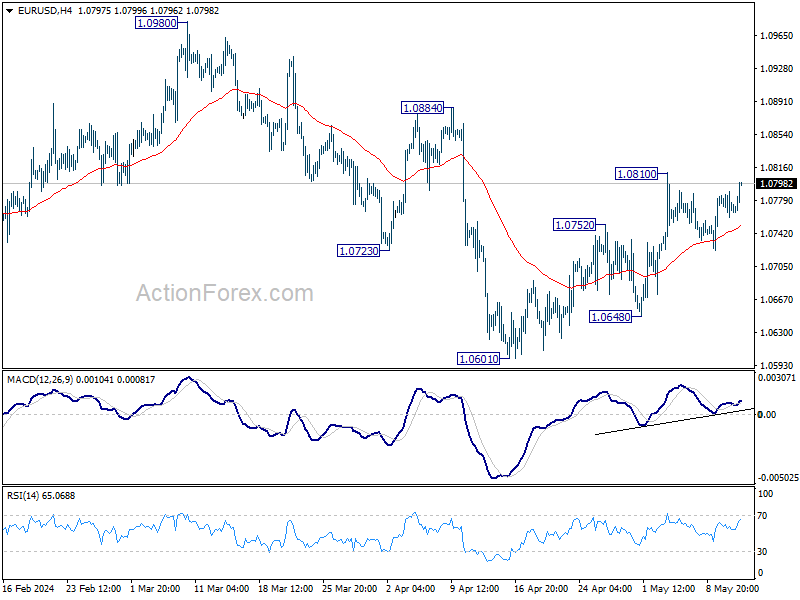

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0757; (P) 1.0773; (R1) 1.0787; More…

EUR/USD is staying below 1.0810 resistance despite today’s rise. Intraday bias remains neutral at this point. Further rally is expected as long as 55 4H EMA (now at 1.0751) holds. On the upside, above 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 55 4H EMA will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Apr | 47.1 | 47.5 | 47.2 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | 2.20% | 2.50% | ||

| 01:30 | AUD | NAB Business Confidence Apr | 1 | 1 | ||

| 01:30 | AUD | NAB Business Conditions Apr | 7 | 9 | ||

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q2 | 2.33% | 2.50% | ||

| 07:00 | CHF | SECO Consumer Climate Q2 | -38 | -40 | -38 | |

| 12:30 | CAD | Building Permits M/M Mar | -11.70% | -4.60% | 9.30% | 8.90% |