The forex markets are still generally staying in consolidative mode today, showing minimal reaction to the latest economic data and comments from central bank officials. Commodity currencies, along with Swiss Franc, are displaying relative strength. Meanwhile, Euro, Dollar, and Yen are on the weaker side.

In the broader financial markets, the recent selloff in global equities seems to have found some temporary stability, though downside risks persist. Gold hovering just below 2400 mark, with prospect for an rising leg towards the critical 2500 resistance level, before forming a major bottom. WTI crude oil is retreating this week, but market participants remaining vigilant for any geopolitical escalations, particularly any retaliatory actions by Israel against Iran.

Technically, buying appeared to be emerging in Nikkei today as it approached 38.2% retracement of 30487.67 to 41087.75 at 37038.51. Firm break of 55 D EMA (now at 38058.00) will argue that the pull back from 41087.75 has completed, and bring stronger rebound. The upcoming CPI data from Japan could be crucial in determining the Nikkei’s next moves.

In Europe, at the time of writing, FTSE is up 0.14%. DAX is down -0.10%. CAC is up 0.16%. UK 10-year yield is down -0.002 at 4.262. Germany 10-year yield is up 0.009 at 2.478. Earlier in Asia, Nikkei rose 0.31%. Hong Kong HSI rose 0.82%. China Shanghai SSE rose 0.09%. Singapore Strait Times rose 1.05%. Japan 10-year JGB yield is down -0.0165 at 0.871.

US initial jobless claims unchanged at 212k, vs exp 214k

US initial claims was unchanged at 212k in April 13, slightly below expectation of 214k. Four-week moving average of initial claims was also unchanged at 214.5k.

Continuing claims rose 2k to 1812k in the week ending April 6. Four-week moving average of continuing claims rose 4k to 1805k.

Bundesbank highlights modest improvement in German economy with ongoing risks

Bundesbank, in its latest monthly report, suggested some improvement in the German economy though underlying weaknesses remain. The report notes, “Germany’s economic situation has brightened somewhat, but it remains weak at its core,” signaling uncertainty about the sustainability of economic growth into the second quarter.

Despite these challenges, there has been a noticeable rise in optimism among consumers, businesses, and investors, potentially setting the stage for a stronger economic recovery than previously anticipated. The Bundesbank highlights, “If this improvement continues, the economy could also pick up more significantly than was expected a month ago.”

However, the report also points out several areas of concern. Industry continues to struggle, and the construction sector might see a downturn following a temporary boost from a mild winter. Furthermore, high interest rates are suppressing investment activities, and while export demand shows weakness, consumer spending remains restrained despite favorable conditions in the labor market, such as rising wages and slowing inflation.

ECB’s de Guindos: We have been crystal clear on June rate cut

During a European Parliament hearing today, ECB Vice President Luis de Guindos stated that ECB has been “crystal clear” on its conditional guidance regarding interest rate cut.

“If things continue as they have been evolving lately, in June we’ll be ready to reduce the restriction of our monetary policy stance,” he said.

While financial markets anticipate a total of 75bps in rate cuts for the year, de Guindos remained non-committal about specific future rate levels.

He pointed out several risks to inflation outlook, including wage dynamics, productivity, unit labor costs, profit margins, and geopolitical tensions.

BoJ’s Noguchi: Poicy rate adjustment expected to be slow

BoJ Board Member Asahi Noguchi highlighted in a speech today the unique economic conditions facing Japan compared to other major economies. He pointed out that any changes to the policy rate are expected to occur at a slower pace than those seen in recent actions by other major central banks.

“With regard to the pace of policy rate adjustment, it is expected to be slow, at a pace that cannot be compared to that of other major central banks in recent years,” Noguchi stated. This approach reflects the central bank’s assessment that it will take considerable time for Japan to consistently achieve its price stability target of 2% inflation.

Noguchi also noted the recent significant wage increases in Japan, describing them as unprecedented. However, he cautioned that these wage hikes alone are not yet sufficient to drive up prices to the level needed for trend inflation to stabilize at the 2% target.

“It is essential for the BoJ to maintain its ultra-loose monetary policy to seek an appropriate balance in the labour supply-demand,” he added.

Australia’s employment contracts -6.6k in Mar, labor market still relatively tight

Australia’s employment figures for March revealed a slight contraction of -6.6k, worse than expectation of 7.2k growth. This downturn was primarily due to drop in part-time employment by -34.5k, partially offset by rise in full-time by 27.9k.

Unemployment rate rose from 3.7% to 3.8%, below expectation of 3.9%. Participation rate fell from 66.7% to 66.6%. Monthly hours worked rose 0.9% mom.

Bjorn Jarvis, Head of Labour Statistics at ABS, noted, “The labour market remained relatively tight in March, with an employment-to-population ratio and participation rate still close to their record highs in November 2023.” He pointed out that although there has been a modest decline of 0.4 percentage points since the highs of last November, the metrics remain substantially above pre-pandemic levels.

Australia NAB business confidence rises to -2 in Q1, cost pressures ease slightly

Australia NAB Quarterly Business Confidence rose from -6 to -2 in Q1. Business Conditions was unchanged at 10. In terms of forward-looking expectations, businesses anticipate a slight downturn in conditions over the next three months, with expectations dipping from 14 to 12. However, the outlook for the next 12 months improved, rising from 16 to 17.

According to NAB Chief Economist Alan Oster, “Consistent with our monthly business survey, today’s release shows business conditions remained resilient at above-average levels through the start of the year. Confidence remained weak but showed some improvement relative to the tail end of 2023.”

The report also highlighted easing cost pressures, although the reduction was minimal. Labor costs grew at a slightly reduced rate of 1.2%, down from 1.3% in the previous quarter, and purchase costs increased by 1.1%, down from 1.2%. Meanwhile, final product price growth remained steady at 0.7%, and retail price growth decreased marginally to 0.8% from 0.9%.

Oster noted, “There continue to be some positive signs of easing cost pressures for businesses but progress was more incremental through Q1. Importantly, forward-looking indicators of firms’ expectations for price growth suggest firms expect some further moderation.”

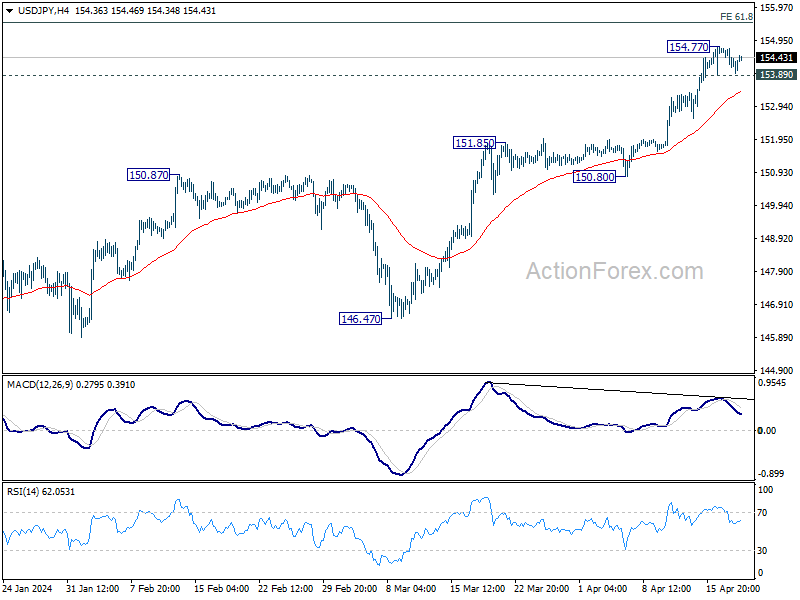

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.11; (P) 154.43; (R1) 154.71; More…

Intraday bias in USD/JPY remains neutral for the moment. Considering bearish divergence condition in 4H MACD, in case of another rise, upside should be limited by 155.20 fibonacci projection level. On the downside, break of 153.89 minor support will turn bias back to the downside for 55 4H EMA (now at 153.41) and possibly below.

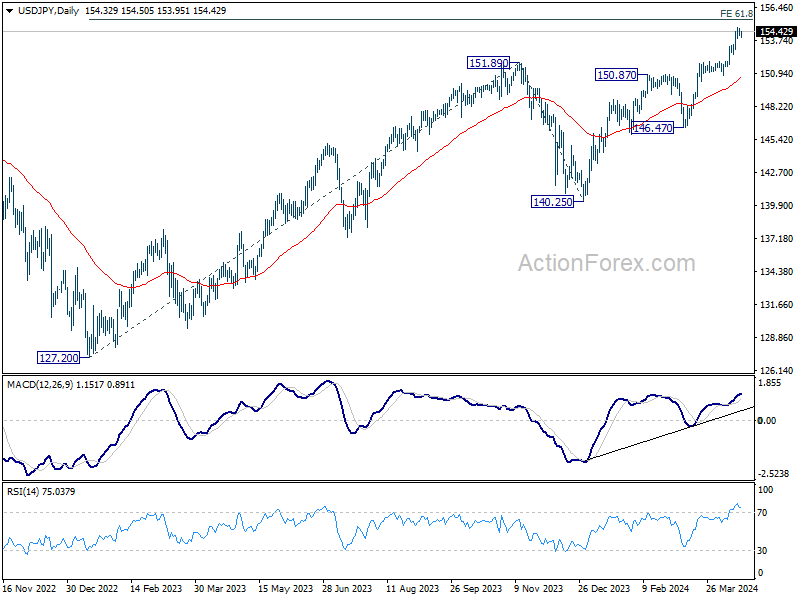

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | -2 | -6 | ||

| 01:30 | AUD | Employment Change Mar | -6.6K | 7.2K | 116.5K | 117.6K |

| 01:30 | AUD | Unemployment Rate Mar | 3.80% | 3.90% | 3.70% | |

| 01:30 | AUD | RBA Bulletin Q1 | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 1.50% | 0.80% | 0.30% | -0.50% |

| 06:00 | CHF | Trade Balance (CHF) Mar | 3.54B | 3.22B | 3.66B | 3.68B |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 29.5B | 45.2B | 39.4B | |

| 12:30 | USD | Initial Jobless Claims (Apr 12) | 212K | 214K | 211K | 212K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | 15.5 | 0.8 | 3.2 | |

| 14:00 | USD | Existing Home Sales Mar | 4.20M | 4.38M | ||

| 14:30 | USD | Natural Gas Storage | 54B | 24B |