Dollar is having a strong, broad-based rebound in early US session, driven by upside surprises in CPI data. The concern for Fed stems not just from the headline inflation spurred by rising energy costs. But more significantly, core inflation failed to slow again, arguing that disinflation progress has stalled further.

The market’s attention is now shifted to the forthcoming minutes from FOMC’s March meeting. The split in Fed policymakers’ projections, revealed through the dot plot, underscores the uncertain path ahead. With 10 officials forecasting three rate cuts this year and nine others suggesting two or fewer, the upcoming minutes are eagerly awaited for deeper insights into Fed’s internal debate and the balance between hawkish and dovish views.

In terms of market reactions, the inflation report lead to sharp increase in 10-year yields, pushing towards 4.5%, and steep decline in stock futures. Additionally, USD/JPY breaks through critical 152, a level that could trigger intervention by Japan. This development positions the currency pair at the center of attention in the upcoming Asian session, with market participants eyeing Japan’s response.

In the broader currency landscape, Dollar’s ascent positions it as the current market leader, followed by Yen. New Zealand Dollar, despite an initial boost from a hawkish RBNZ, slid to one of the second weakest position, just ahead of Australian Dollar. Canadian Dollar remains in limbo, with markets awaiting BoC’s rate decision, while Sterling slightly outperforms other European majors like the Euro and Swiss Franc.

Technically, one focus for the US session is whether DOW would dive through 38483.25 near term support, and close below there. If realized, that would indicate that DOW is at least in a correction to the rally from 32327.20, and target 38.2% retracement of 32327.20 to 39899.05 at 37000.42 next.

In Europe, at the time of writing, FTSE is up 0.42%. DAX is up 0.19%. CAC is up 0.04%. UK 10-year yield is up 0.075 at 4.107. Germany 10-year yield is up 0.054. Earlier in Asia, Nikkei fell -0.48%. Hong Kong HSI rose 1.85%. China Shanghai SSE fell -0.70%. Singapore Strait Times rose 0.67%. Japan 10-year JGB yield rose 0.014 to 0.799.

US CPI jumps to 3.5% yoy in Mar, CPI core unchanged at 3.8% yoy

US CPI rises 0.4% mom in March, above expectation of 0.3% mom. CPI core (all items less food and energy) rises 0.4% mom, also above expectation of 0.3% mom. Energy index rose 1.1% mom. Food index rose 0.1% mom.

For the 12 months period, CPI accelerated from 3.2% yoy to 3.5% yoy, above expectation of 3.4% yoy. CPI core was unchanged at 3.8% yoy, above expectation of 3.7% yoy. Energy index was up 2.1% yoy while food index was up 2.2% yoy.

RBNZ holds OCR steady, no room for delay in bring down inflation to target band

RBNZ maintained Official Cash Rate unchanged at 5.50%, aligning with market expectations. This decision comes with reiterated commitment to “restrictive monetary policy stance,” deemed necessary to alleviate capacity pressures and guide inflation back within the target range of 1 to 3 percent within “this calendar year”.

During the recent meeting, members concurred that there has been “no material change in economic outlook” since their February Statement. There remains a “limited tolerance” for prolonging the timeframe to meet the inflation target, especially with inflation expectations and pricing intentions continuing to “remain elevated”.

The “persistence of services inflation” and “elevated” goods price inflation were identified as continuous risks, with expected near-term increases in local government rates, insurance, and utility costs potentially decelerating the reduction in headline inflation.

On the flip side, RBNZ acknowledges potential downside risks to the inflation outlook, notably the impact of continued restrictive monetary policy amid weak global growth. This environment could precipitate a quicker than anticipated reduction in inflation. Weak business and consumer confidence, coupled with potential increases in unemployment and financial stress, are areas of concern. Additionally, structural economic challenges in China are highlighted as significant, given its critical role in the global economy and as a major trading partner for New Zealand.

BoJ’s Ueda: Accommodative monetary policy to continue

In today’s parliamentary address, BoJ Governor Kazuo Ueda reaffirmed the Bank of Japan’s stance on continuing its accommodative monetary policy, underscoring the short-term interest rate as the “primary policy tool.”

A key focus for BoJ, as Ueda noted, is the scrutiny of trend inflation’s progress towards 2% target in judging “appropriate degree of monetary support.”

Meanwhile, Ueda clarified that BoJ would not alter its monetary policy solely in response to FX fluctuations. However, he acknowledged that significant FX movements, if they lead to an unexpected increase in import prices and thereby risk elevating trend inflation beyond projections, could necessitate a reassessment of monetary policy.

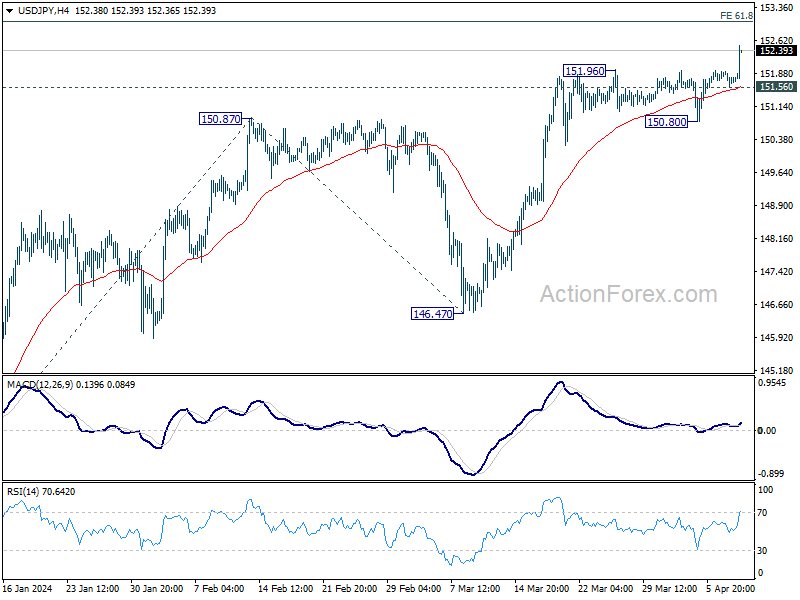

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.59; (P) 151.76; (R1) 151.96; More…

USD/JPY’s surges to as high as 151.51 so far, and the break of 151.93 key resistance indicates long term up trend resumption. Intraday bias is back on the upside. Next target is 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. On the downside, below 151.56 minor support will turn intraday bias neutral again. But outlook will stay bullish as long as 150.80 support holds.

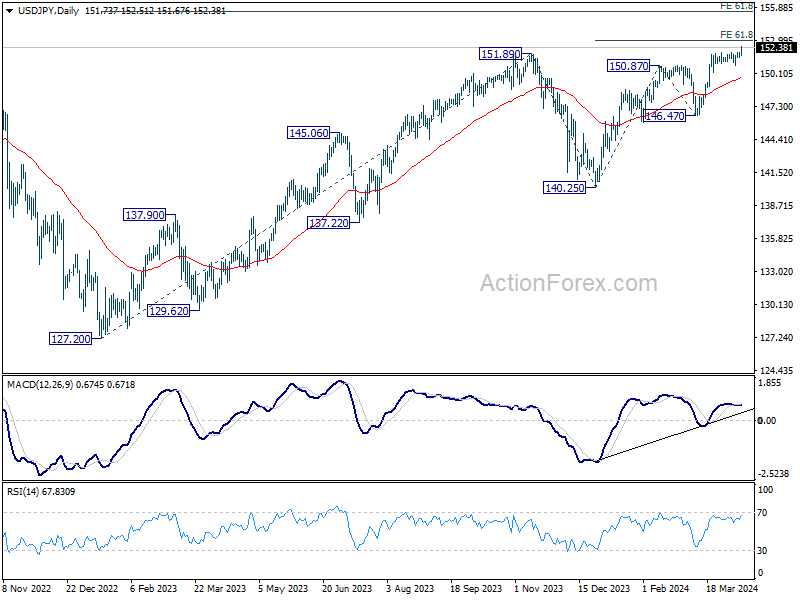

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Mar | 3.20% | 3.10% | 3.00% | |

| 23:50 | JPY | PPI Y/Y Mar | 0.80% | 0.80% | 0.60% | 0.70% |

| 02:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% | 5.50% | |

| 08:00 | EUR | Italy Retail Sales M/M Feb | 0.10% | 0.20% | -0.10% | |

| 12:30 | CAD | Building Permits M/M Feb | 9.30% | -3.50% | 13.50% | 12.90% |

| 12:30 | USD | CPI M/M Mar | 0.40% | 0.30% | 0.40% | |

| 12:30 | USD | CPI Y/Y Mar | 3.50% | 3.40% | 3.20% | |

| 12:30 | USD | CPI Core M/M Mar | 0.40% | 0.30% | 0.40% | |

| 12:30 | USD | CPI Core Y/Y Mar | 3.80% | 3.70% | 3.80% | |

| 13:45 | CAD | BoC Rate Decision | 5.00% | 5.00% | ||

| 14:00 | USD | Wholesale Inventories Feb F | 0.50% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | 0.9M | 3.2M | ||

| 15:30 | CAD | BoC Press Conference | ||||

| 18:00 | USD | FOMC Minutes |