The USD is ending the session lower to end the trading week with most of the declines coming vs the AUD and the NZD. Overnight, ANZ reported that is now predicts that the Reserve Bank of New Zealand (RBNZ) will increase the Official Cash Rate (OCR) by 25 basis points in both February and April, bringing it to a total of 6%, which deviates from the consensus view. This forecast is based on a series of small, but unwelcome surprises in economic data, leading ANZ to believe that the RBNZ will not feel confident that it has sufficiently met its inflation targets. The OCR is currently at 5.5%, and while the market is largely expecting the RBNZ to maintain rates in the upcoming February meeting, with a 90% anticipation of a hold decision, ANZ stands out by anticipating rate hikes in both the February 28 and April 10 meetings.

That news helped to propel the NZDUSD to a near 1% gain on the day. The AUDUSD moved up 0.54%. The USD was mixed vs the other currencies in a subdued up and down trading session in the US. Overall, for the day, the NZD was the strongest of the major currencies while the CHF was the weakest.

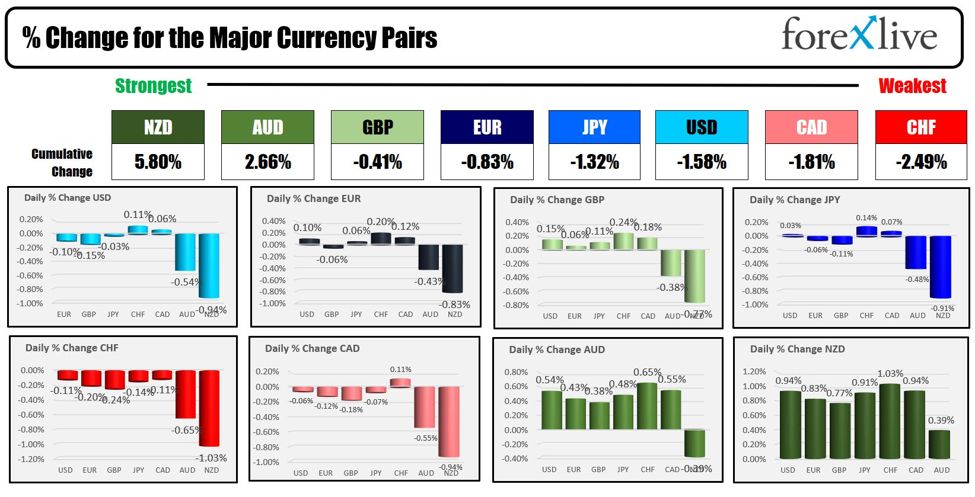

The strongest to the weakest of the major currencies

In the session today, the Canada employment data showed a gain of 37.6K but all the gain was in part time jobs. Full time jobs fell by -11.6K. The unemployment rate did fall to 5.7% from 5.8% last month. The USDCAD ended the day little changed in up and down trading.

There were no US economic data today. However, there was some additional Fed talk from Fed’s Logan and Bostic.

Fed’s Logan emphasized that the labor market remains very tight, although there are signs of loosening, signaling a nuanced view of current economic conditions. She acknowledged significant progress made on inflation but noted that further efforts are necessary to fully address it. Logan advocated for a careful and data-driven approach, suggesting there is no immediate urgency to adjust interest rates at this time. Her comments reflect a priority on building confidence in the long-term stability of inflation rates. While she noted that supply chains have largely normalized, Logan also acknowledged ongoing supply chain issues in certain industries, indicating these may need more time to resolve fully. She expressed a strong focus on monitoring potential risks that could undermine progress on inflation, highlighting the Fed’s vigilance in maintaining economic stability.

Fed’s Bostic, in a discussion with NPR, expressed concern that inflation has been excessively high for an extended period. He conveyed optimism about the United States being on track to regain its pre-pandemic economic vitality, emphasizing the importance of preventing a new surge in inflation. Bostic highlighted that current data indicate the potential for continued real wage gains over the next several months. He pointed out that businesses are primarily challenged by difficulties in finding employees and affordable housing. Furthermore, Bostic reassured that banks are aware of the risks present in their portfolios and are equipped to manage them effectively, suggesting a level of preparedness within the banking sector to navigate potential economic fluctuations.

For the trading week, the US dollar index rose 0.10% (DXY) but was mixed vs the major currencies. Looking at the major currencies, the USD was virtually unchanged vs the EUR and GBP, it was the strongest vs the CHF and the weakest vs the NZD:

- EUR, unchanged

- JPY, +0.65%

- GBP, unchanged

- CHF, +0.90%

- CAD, -0.02%

- AUD, -0.20%

- NZD, -1.49%

Today, yields were mixed with the shorter end higher, and the longer end lower.

- 2-year 4.484%, +2.8 basis points

- 5-year, 4.140%, +1.6 basis points

- 10-year, 4.177%, +0.7 basis points

- 30 year, 4.374%, -0.6 basis points

For the trading week, yields moved higher as the market started to dial back the number of tightening.

- 2 year, +11.4 basis points

- 5 year, +15.4 basis points

- 10 year, +15.3 basis points

- 30 year, +15.1 basis points

US stocks today continued it move to the upside with solid gains for the broader indices. The S&P index closed above the 5000 level for the first time ever. The Nasdaq index traded above 16K for the first time since November 2021. The S&P closed at a record level and although the Dow as lower today, it traded to record levels this week.

The final numbers are showing:

- Dow industrial average fell -54.64 points or -0.14% at 38671.70

- S&P rose 28.70 points or 0.57% at 5026.62

- Nasdaq rose 196.94 points or 1.25% at 15990.65

For the week, the major indices closed higher for the 5th week in a row after starting 2024 with a sharp decline in the 1st trading week of the year.

- Dow industrial average, rose 0.04%

- S&P rose 1.37%

- Nasdaq rose 2.31%

In other markets this week,

- Crude oil rose $4.26 or 5.89% to $76.54

- Gold fell -$15.02 or -0.74% to $2024.42

- Silver fell $0.08 or -0.34%

- Bitcoin surged by $4975 or 11.6% as risk on flows pushed the digital currency higher.

Next week US CPI will highlight the economic releases

Monday:

- BOE Gov. Bailey speaks

Tuesday:

- NZ inflation expectations

- UK Employment

- US CPI

Wednesday:

- UK CPI

- UK Gov. Bailey speaks

Thursday:

- AUD employment

- UK GDP

- US Retail Sales

- US unemployment claims

Friday:

- UK Retail sales

- US PPI

- US Michigan Consumer Sentiment.

On the earnings calendar next week, Shopify, Coca Cola, AIG, Cisco and Coinbase are companies of interest. The Big Daddy of perhaps the entire earnings season will be released on February 21, when Nvidia is scheduled to report. The fate of AI and Ai stocks rests with the chip supplier:

Tuesday:

- Shopify

- Coca Cola

- Marriott

- Lyft

- AIG

Wednesday:

- Kraft Heinz

- Albemarle

- Twillio

- Cisco

Thursday:

- John Deere

- Coinbase

Thank you for your support. Wishing you all a great weekend.