Japanese Yen is facing increased selling pressure today, influenced by rebound in US and European benchmark treasury yields. Additionally, traders are scaling back their expectations of imminent monetary policy changes by BoJ, in the wake of the recent devastating earthquake in Japan. This context sets the stage for potential downside risks to Yen in the near term, with break of certain support levels possibly leading to a more significant unwinding of long positions.

In contrast, both Sterling and Euro recovered earlier in the day, bolstered by the release of upward revisions in their respective PMI Services data. regained some of its lost ground against these European currencies following the release of stronger-than-expected ADP job data. Nevertheless, the key determinant of Dollar’s near-term trajectory is likely to be tomorrow’s non-farm payrolls report. Elsewhere in the currency markets, Swiss Franc and Aussie are showing weakness, while Loonie displays mixed performance.

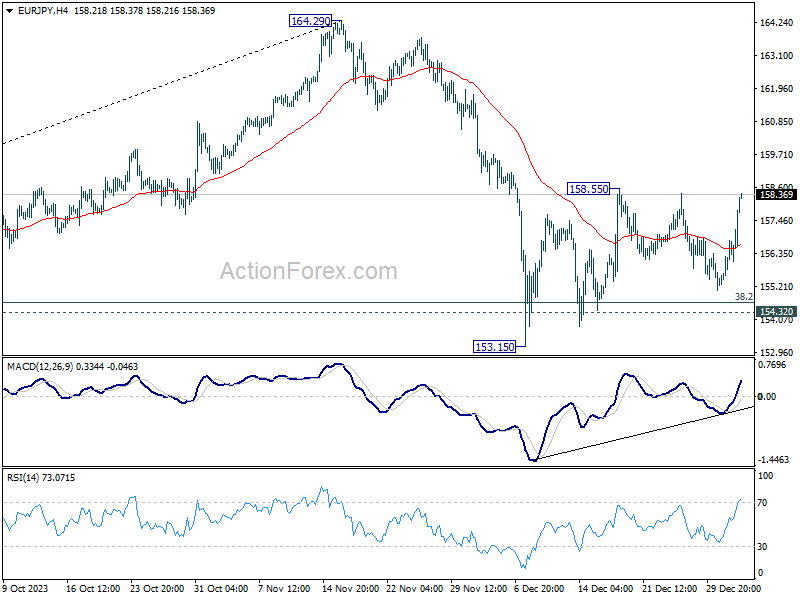

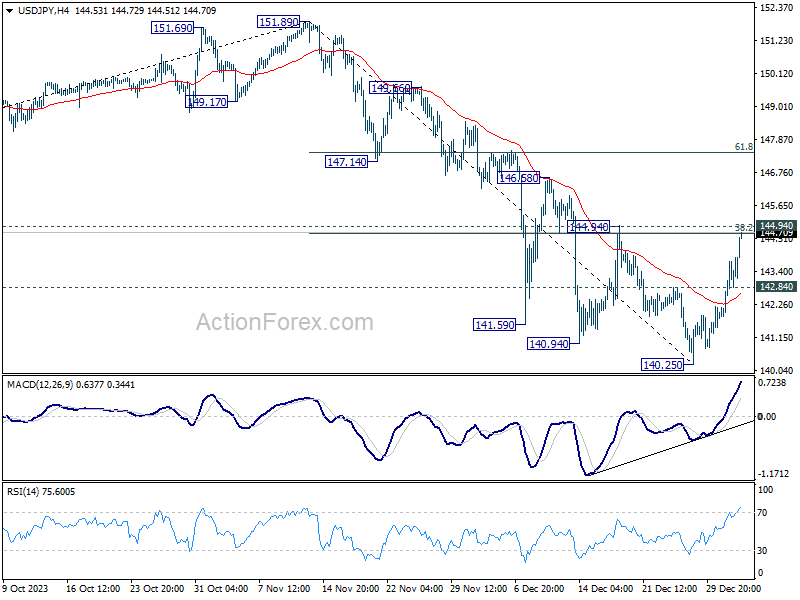

Technically, immediate focus is now on some resistance levels in Yen pairs. These levels include 144.94 resistance in USD/JPY, 158.55 resistance in EUR/JPY, and 184.15 resistance in GBP/JPY. Simultaneous break of these levels will indicate that Yen’s near term selloff is gathering momentum for more decline.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.06%. CAC is up 0.18%. Germany 10-year yield is up 0.097 at 2.122. UK 10-year yield is up 0.084 at 3.724. Earlier in Asia, Nikkei fell -0.53%. Hong Kong HSI fell -0.00% China Shanghai SSE fell -0.43%. Singapore Strait Times fell -0.79%. Japan 10-year JGB yield rose 0.0016 to 0.627.

US ADP employment grows 164k, pay growth retreat further

US ADP private employment grew 164k in December, above expectation of 130k. By sector, goods-producing jobs rose 9k while service-providing jobs rose 155k. By establishment size, small companies added 74k jobs, medium companies added 53k, and large companies added 40. Median change in annual pay for jobs-stayers slowed from 5.6% to 5.4%, and for job-changers from 8.3% to 8.0%.

“We’re returning to a labor market that’s very much aligned with pre-pandemic hiring,” said Nela Richardson, chief economist, ADP. “While wages didn’t drive the recent bout of inflation, now that pay growth has retreated, any risk of a wage-price spiral has all but disappeared.”

US initial jobless claims falls to 202k, vs exp 210k

US initial jobless claims fell -18k to 202k in the week ending December 30, below expectation of 210k. Four-week moving average of initial claims fell -5k to 208k.

Continuing claims fell -31k to 1855k in the week ending December 23. Four-week moving average of continuing claims fell -250 to 1867k.

UK PMI services finalized at 53.4, rising output and price pressures

UK PMI Services was finalized at 53.4 in December, up from November’s 50.9, and the highest reading since last June. S&P Global noted continuous rise in output and new work for the second consecutive month. However, the sector also saw a slight decline in employment numbers, and there was acceleration in price charged inflation. Price charged inflation accelerated again. PMI Composite was finalized at 52.1, up from prior month’s 50.7.

Tim Moore, Economics Director at S&P Global Market Intelligence, stated, “December data indicated that the UK service sector ended last year on a high,” attributing the recovery in client demand to expectations of lower borrowing costs and an improving global economic outlook for 2024.

Moore also highlighted that business activity expectations for the upcoming year are now at their most optimistic since May of the previous year, although he pointed out that staff hiring remained a weak spot in December, with many companies yet to lift their hiring freezes.

Moore further commented on the inflationary pressures within the service sector, noting substantial input cost increases driven by strong wage pressures. This trend has led to a robust rise in prices charged across the service sector as businesses strive to protect their margins. The rate of inflation in this regard was the fastest since July of the previous year, indicating the challenges faced by service providers in managing costs while maintaining competitive pricing.

Eurozone PMI services finalized at 48.8, not quite recession yet, but hardly growth oriented

Eurozone PMI Services was finalized at 48.8 in December, up slightly from November’s 48.7, a 5-month high. PMI Composite was finalized at 47.6, unchanged from prior month’s reading, indicating continued contraction in the broader economy.

A country-by-country analysis of Composite PMI reveals varying performances. Ireland, with PMI of 51.5, experienced a two-month low, while Spain, at 50.4, reached a five-month high. Italy’s PMI climbed to a three-month high of 48.6, and Germany’s index, at 47.4, hit a two-month low. France, at 44.8, saw a four-month high, yet its service sector remains the weakest among the top Eurozone economies.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, observed that Eurozone’s service sector is undergoing a slight contraction, with job numbers marginally increasing. He stated, “It’s not quite recession territory yet for services, but the vibe is far from growth-oriented.”

Furthermore, he expressed concerns about the broader economic outlook, noting that the Composite PMI is signaling a recession in Eurozone. The bank’s GDP Nowcast model projects a consecutive contraction in the region’s output for the fourth quarter, adding credence to this recessionary warning.

In examining the service sectors of the top Eurozone countries, de la Rubia identified significant variations. Spain’s service sector is performing well, showing growth for four consecutive months. In contrast, Germany and Italy are experiencing stagnation, while France’s service sector is consistently declining, making it the worst performer in this group.

Japan’s PMI manufacturing finalized at 47.9, deeper contraction and higher input inflation

Japan’s PMI Manufacturing was finalized at 47.9 in December, down from November’s 48.3, marking the most significant sector contraction since February 2023. S&P Global reports that this downturn was characterized by notable declines in both production and new orders, alongside rise in input price inflation. Despite these challenges, there was an unexpected increase in business confidence, reaching a five-month high.

Paul Smith from S&P Global Market Intelligence noted, “Market uncertainty led to reduced orders and output, especially from key export clients in China, Europe, and North America.” He also mentioned specific struggles in the electronics sector and a general lack of investment.

However, Smith acknowledged increased cost pressures, with input price inflation at a three-month high due to more expensive raw materials, particularly imports.

Looking ahead, Smith conveyed optimism among Japanese manufacturers, expecting an end to client destocking and predicting that new product launches will boost production in 2024.

China’s Caixin PMI services rises to 52.9, businesses express confidence

China’s Caixin PMI Services marked a significant rise to 52.9 in December from 51.5, achieving its highest level since July. Concurrently, PMI Composite, which combines both manufacturing and services, also saw an improvement, climbing from 51.6 to 52.6.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that businesses are “expressing confidence” in an improved economic outlook for the coming year. This optimism is reflected in the business expectations gauge, which, despite being “about 3 points below” the 2023 average for the first 11 months, still aligns with the “historical mean” from 2012 to 2022.

Looking ahead

Germany CPI flash, Eurozone PMI services final and UK PMI services final will be released in European session. Later in the day, main focus will be on US ADP employment and jobless claims.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.18; (P) 142.96; (R1) 144.07; More…

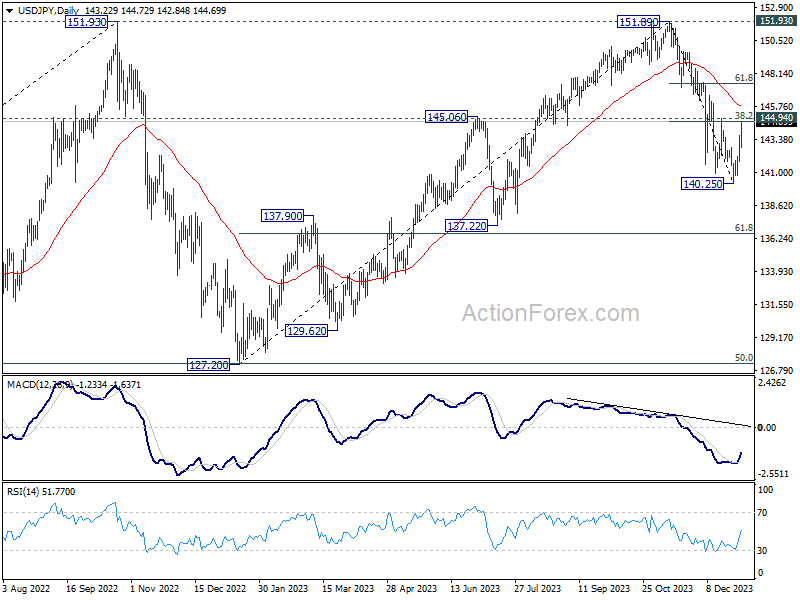

USD/JPY’s rebound from 140.25 short term bottom accelerates higher today and met 38.2% retracement of 151.89 to 140.25 at 144.69 already. Intraday bias will stay on the upside as long as 142.84 minor support holds. Sustained break of 144.94 resistance will bring further rally to 61.8% retracement at 147.44. On the downside, though, break of 142.84 minor support will bring retest of 140.25 instead.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). However, break of 144.94 resistance will dampen this bearish view and argue that fall from 151.89 is a correction to rise from 127.20 only.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Dec F | 47.9 | 47.7 | 47.7 | |

| 01:45 | CNY | Caixin Services PMI Dec | 52.9 | 51.6 | 51.5 | |

| 08:45 | EUR | Italy Services PMI Dec | 49.8 | 49.8 | 49.5 | |

| 08:50 | EUR | France Services PMI Dec F | 45.7 | 44.3 | 44.3 | |

| 08:55 | EUR | Germany Services PMI Dec F | 49.3 | 48.4 | 48.4 | |

| 09:00 | EUR | Eurozone Services PMI Dec F | 48.8 | 48.1 | 48.1 | |

| 09:30 | GBP | Services PMI Dec F | 53.4 | 52.7 | 52.7 | |

| 09:30 | GBP | Mortgage Approvals Nov | 50K | 48K | 47K | |

| 09:30 | GBP | M4 Money Supply M/M Nov | -0.10% | 0.20% | 0.30% | |

| 12:30 | USD | Challenger Job Cuts Y/Y Dec | -20.20% | -40.80% | ||

| 13:00 | EUR | Germany CPI M/M Dec P | 0.10% | 0.20% | -0.40% | |

| 13:00 | EUR | Germany CPI Y/Y Dec P | 3.70% | 3.80% | 3.20% | |

| 13:15 | USD | ADP Employment Change Dec | 164K | 130K | 103K | |

| 13:30 | USD | Initial Jobless Claims (Dec 29) | 202K | 210K | 218K | 220K |

| 14:45 | USD | Services PMI Dec F | 51.3 | 51.3 | ||

| 15:30 | USD | Natural Gas Storage | -33B | -87B | ||

| 16:00 | USD | Crude Oil Inventories | -3.2M | -7.1M |