As US session commences, Dollar’s rebound is gaining additional momentum. This upswing is occurring against a backdrop of intensifying selloff in the equities market, primarily influenced by Apple’s downturn following downgrade by Barclays over concerns of weakening sales.

European majors are currently bearing the brunt of the market’s shift. The final PMI manufacturing release from S&P Global has fueled this sentiment, suggesting that Eurozone may have already slipped into a recession in the third quarter. This perspective is further compounded by downward revision of UK’s PMI manufacturing figures, indicating continued strain on these economies.

In the broader currency markets, Japanese Yen is also showing weakness, a situation likely exacerbated by the powerful earthquake in Japan. This natural disaster has impacted the market at a time when the Japanese stock market remains closed for a public holiday. On the other hand, Canadian and Australian Dollars are showing mild firmness, trailing behind the strengthening greenback.

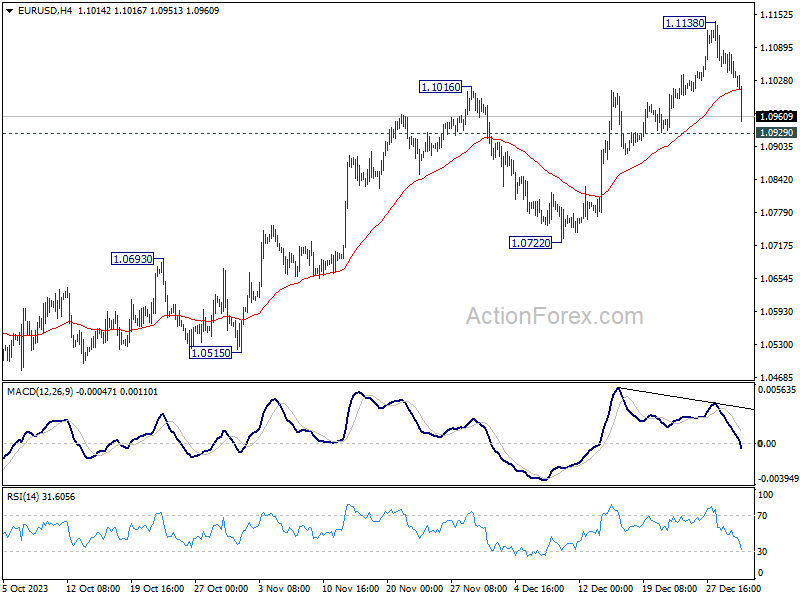

From a technical analysis perspective, as Dollar’s rebound extends, key levels to watch are 1.0929 minor support in EUR/USD and 1.2611 minor support in GBP/USD. Firm breaks below these levels could signify that Dollar’s rebound is poised to continue further, potentially until the release of non-farm payroll report on Friday.

In Europe, at the time of writing, FTSE is down -0.45%. DAX is down -0.46%. CAC is down -0.67%. Germany 10-year yield is up 0.0805 at 2.089. UK 10-year yield is up 0.141 at 3.680. Earlier in Asia, Hong Kong HSI fell -1.52%. China Shanghai SSE fell -0.43%. Singapore Strait Times fell -0.32%. Japan was on holiday.

UK PMI manufacturing finalized at 46.2, 17th month of contraction

UK PMI Manufacturing was finalized at 46.2 in December, down from November’s 47.2. This marks the seventeenth consecutive month where the index has remained below the neutral 50 threshold, indicating ongoing contraction. According to S&P Global, key aspects such as output, new orders, and employment are all in decline. Additionally, business optimism has reached a 12-month low.

Rob Dobson, Director at S&P Global Market Intelligence, pointed out demand environment remains challenging, with new orders continuing to decline due to difficult conditions in both domestic and key export markets, particularly the European Union.

The downturn is prompting companies to adopt a more cautious approach to costs. There have been notable cutbacks in stock levels, purchasing, and employment as firms grapple with the ongoing challenges.

Eurozone’s PMI manufacturing finalized at 44.4, relentless slump continues

Eurozone’s PMI Manufacturing was finalized at 44.4 in December, up slightly from November’s 44.2. Despite this minor uptick, marking a seven-month high, the index remained below the critical 50.0 threshold, signaling a continued deterioration in operating conditions across the sector.

Country-by-country breakdown of Manufacturing PMI reveals a diverse picture. Greece stands out with a PMI of 51.3, indicating expansion and marking a four-month high. In contrast, other major economies like Ireland, Spain, Italy, the Netherlands, Germany, France, and Austria all recorded PMIs indicative of contraction, with varying degrees of severity. Notably, France registered a PMI of 42.1, a 43-month low. On the other hand, Germany rose to an 8-month high at 433.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, remarked on the “relentless slump” in Eurozone’s manufacturing sector, noting that the marginal improvement in the PMI does little to alleviate concerns about the persistent decline in activity and demand for manufactured goods. The consistent sluggishness in new orders was particularly alarming, reflecting a pervasive gloom across the sector.

According to HCOB’s Nowcast model anticipates a contraction in the Eurozone’s GDP for the fourth quarter. This projection, if realized, indicates that Eurozone may have already entered a recession as early as the third quarter.

China’s Caixin PMI manufacturing rises, as NBS PMI shows contraction

December brought mixed signals from China’s manufacturing sector, as indicated by two key indices: Caixin PMI and official NBS PMI. Caixin PMI Manufacturing slightly increased from 50.7 to 50.8, surpassing expectations of 50.4, suggesting a marginal yet steady expansion in the manufacturing sector. Notably, Caixin highlighted that both output and new orders are rising at faster rates, indicating increased production and demand within the industry.

However, the same period saw a dip in official PMI Manufacturing, which fell from 49.4 to 49.0. This decline suggests contraction in the sector, contrasting with optimism reflected in Caixin PMI data. The difference between these two indices can be attributed to their varied focus groups; Caixin PMI typically surveys small and medium-sized enterprises, while NBS PMI is more reflective of larger, state-owned companies.

Wang Zhe, Senior Economist at Caixin Insight Group, emphasized the improved economic outlook for the manufacturing sector, with expanding supply and demand, and stable price levels. Yet, he also pointed out significant challenge in employment, highlighting businesses’ cautious approach in areas like hiring, raw material purchasing, and inventory management.

On the other hand, NBS PMI Non-Manufacturing showed a slight improvement, rising from 50.2 to 50.4. This marginal increase suggests a modest expansion in China’s services sector.

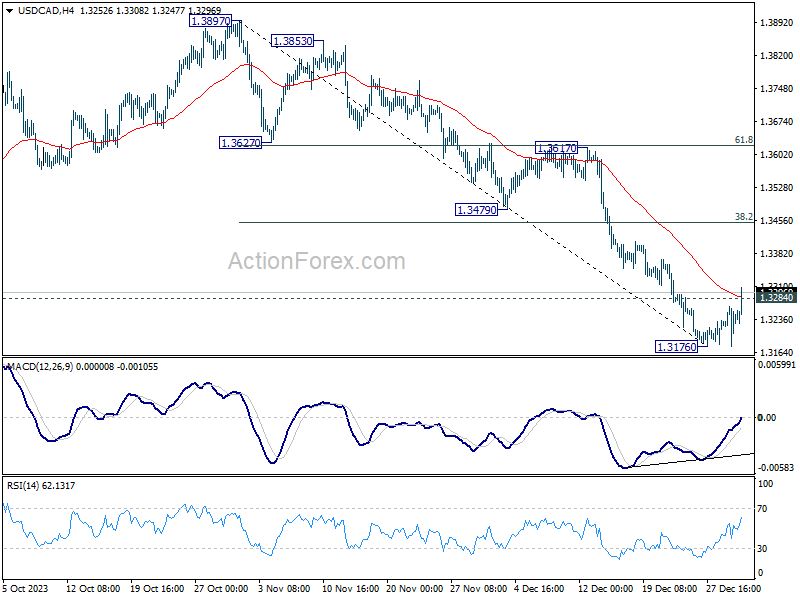

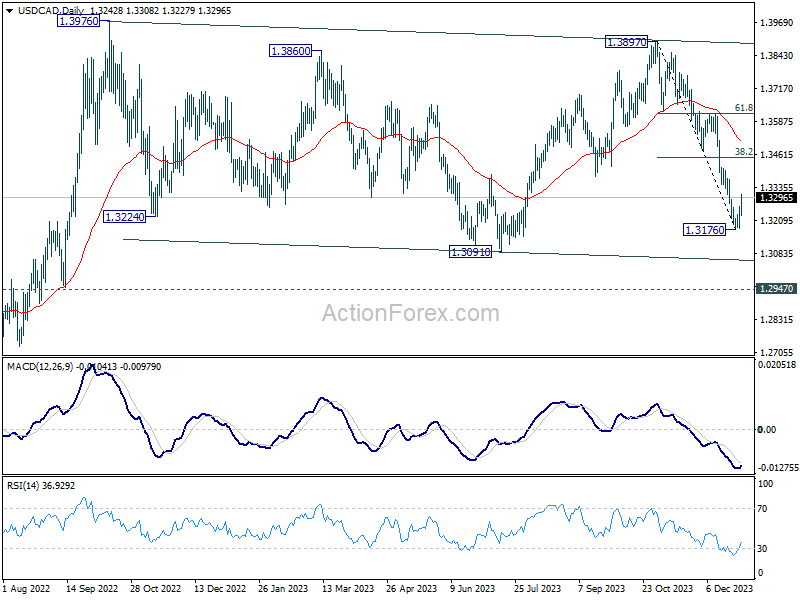

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3196; (P) 1.3230; (R1) 1.3283; More…

USD/CAD’s break of 1.3284 minor resistance indicate short term bottoming at 1.3176, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 38.2% retracement of 1.3897 to 1.3176 at 1.3451. On the downside, however, break of 1.3176 will resume the fall from 1.3897 to 1.3091 support and possibly below.

In the bigger picture, outlook is mixed up by deeper then expected fall from 1.3897. But after all, price actions from 1.3976 (2022 high) are viewed as a corrective pattern that’s in progress. Larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage as long as 1.2947 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Nov | 4.30% | 4.30% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Dec | 50.8 | 50.4 | 50.7 | |

| 08:45 | EUR | Italy Manufacturing PMI Dec | 45.3 | 44.4 | 44.4 | |

| 08:50 | EUR | France Manufacturing PMI Dec F | 42.1 | 42 | 42 | |

| 08:55 | EUR | Germany Manufacturing PMI Dec F | 43.3 | 43.1 | 43.1 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec F | 44.4 | 44.2 | 44.2 | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Nov | -0.90% | -1% | -1% | |

| 09:30 | GBP | Manufacturing PMI Dec F | 46.2 | 46.4 | 46.4 | |

| 14:30 | CAD | Manufacturing PMI Dec | 47.7 | |||

| 14:45 | USD | Manufacturing PMI Dec F | 48.2 | 48.2 | ||

| 15:00 | USD | Construction Spending M/M Nov | 0.60% | 0.60% |