Japanese Yen is extending its broad-based pullback today. This movement appears to be a strategic response from traders lightening their positions in anticipation of the upcoming BoJ policy decision. Although a rate hike by the BoJ seems highly unlikely at this stage, there is speculation about potential adjustments in the central bank’s communication. These changes are anticipated to lay the groundwork for concluding the yield curve control policy in January, followed by a possible rate hike in April to exit the prolonged phase of negative interest rates. However, given the BoJ’s history of unexpected moves, traders are bracing themselves for substantial volatility, regardless of the decision made.

In other parts of the currency markets, US Dollar, Sterling, and Euro are displaying signs of weakness. Notably, Euro remains unfazed by the recent, worse-than-expected German Ifo business climate data. On the other end of the spectrum, New Zealand Dollar and the Australian Dollar are showing marked strength. Meanwhile, Swiss Franc and Canadian Dollar are exhibiting mixed performances.

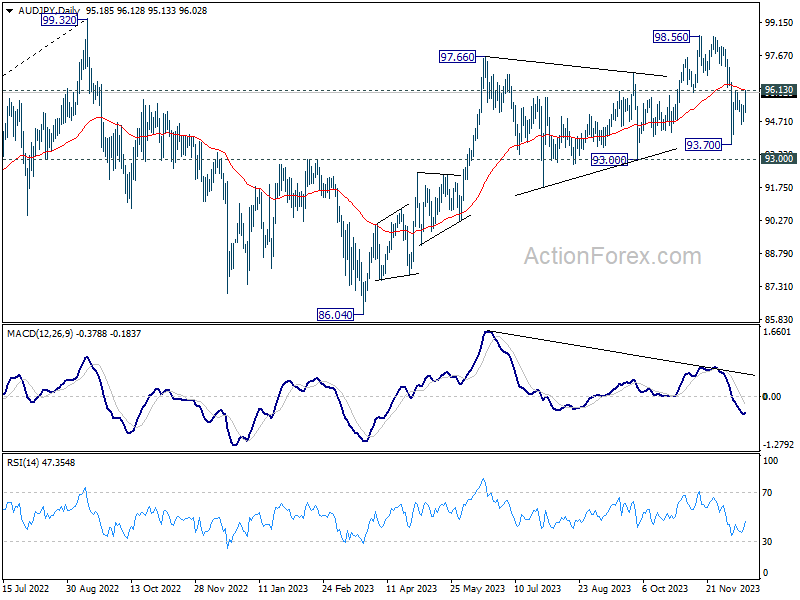

One currency pair of particular interest is AUD/JPY, especially in the context of the upcoming RBA minutes in the Asian session, in addition to BoJ. From a technical standpoint, decisive break of 96.13 resistance, which is close to 55 D EMA, will argue that corrective fall from 98.56 is completed at 93.70, ahead of 93.00 support. This development would keep the rally from 86.04 intact, for further rise through 98.56 next. Nevertheless, rejection by 96.13 will likely resume the fall from 98.56, probably through 93.00 support, as reversing the rise from 96.04.

In Europe, at the time of writing, FTSE is up 0.65%. DAX is down -0.43%. CAC is down -0.35%. Germany 10-yaer yield is up 0.024 at 2.043. UK 10-year yield is up 0.001 at 3.690. Earlier in Asia, Nikkei fell -0.64%. Hong Kong HSI fell -0.97%. China Shanghai SSE fell -0.40%. Singapore Strait Times fell -0.11%. Japan 10-year JGB yield fell -0.0403 to 0.670.

Fed’s Mester: The next phase is not when to reduce rates

In a Financial Times interview, Cleveland Fed President Loretta Mester put emphasis on the duration of maintaining restrictive monetary policy to ensure that inflation reliably returns to the 2% target. That’s contrary to market expectations, which centers on timing and extent of rate cuts.

Mester’s key statement, “The next phase is not when to reduce rates… It’s about how long do we need monetary policy to remain restrictive in order to be assured that inflation is on that sustainable and timely path back to 2%,”

“The markets are a little bit ahead. They jumped to the end part, which is ‘We’re going to normalize quickly’, and I don’t see that,” she added.

When the discussion eventually shifts to the timing and pace of rate cuts, Mester highlighted the importance of one-year forward inflation expectations and their alignment towards the 2% target.

“If you don’t take action as expected inflation comes down, then you’re really firming policy,” she warned. “You don’t want to inadvertently become more restrictive than you think is appropriate.”

ECB’s Vasle cautions against premature rate cut expectations

ECB Governing Council member Bostjan Vasle expressed skepticism about market expectations for imminent interest rate cuts, considering them “premature,” both in terms of timing and the overall scope of such moves. This perspective challenges the market’s anticipation of monetary easing, which currently sees 50-50 chance of a rate cut by March, with a full cut expected by April

Vasle emphasized that the current market pricing “has lowered the level of restriction”. Additionally, the accommodation priced into by interest rate expectations seems to be at odds with the monetary stance required to steer inflation back to the target.

Additionally, Vasle indicated that ECB would likely wait until at least the end of Q1 before considering any changes to its stance. This approach is grounded in the need for more comprehensive data, which will only be available around March or April. he added, “We will need to understand the underlying trends better, and we need the new projections, too.”

On the inflation front, Vasle posited that inflation could rebound at the year’s turn, potentially hovering between 2.5% to 3% through the first half of the next year. Vasle said, “So it’s appropriate to wait and observe price growth through this period and reassess our outlook.”

Germany’s Ifo business climate dips to 86.4, economy remains weak

Germany’ Ifo Business Climate fell from 87.3 to 86.4 in December, below expectation of 87.8. Current Assessment index fell from 89.4 to 88.5, below expectation of 89.5. Expectations index fell from 85.2 to 84.3, below expectation of 85.8.

By sector, manufacturing fell from -13.8 to -17.2. Services rose from -2.5 to -1.7. Trade fell from -22.2 to -26.6. Construction fell from -29.5 to -33.1.

The Ifo Institute’s statement encapsulates the current sentiment, noting that “companies were less satisfied with their current business” and expressing a more skeptical view of the first half of 2024. The acknowledgment that “the German economy remains weak as the year draws to a close” is telling of the challenges facing Europe’s largest economy.

NZ BNZ services rises to 51.2, maintains oscillating course

New Zealand BusinessNZ Performance of Services Index rose from 49.2 to 51.2 in November, crossing the threshold from contraction to expansion. However, it’s crucial to note that this figure remains below the long-term average of 53.5, suggesting that recovery is still in its nascent stages.

Looking at more details, activity/sales rose from 47.5 to 48.7. Employment rose from 49.5 to 51.0. New orders/business rose from 52.1 to 52.3. Stocks/inventories jumped from 51.5 to 55.0. Supplier deliveries rose from 50.1 to 52.9.

BusinessNZ Chief Executive Kirk Hope’s observation that the sector has been oscillating between contraction and expansion in recent months underscores the volatility and uncertainty still prevalent in the business environment.

The proportion of negative comments from businesses decreased from 58.2% in October to 54.0%. This reduction, though modest, is a positive sign, indicating a slight improvement in business sentiment. Hope added, “negative comments continued to be pinpointed on key areas such as the economy, inflation and cost of living”.

New Zealand Westpac consumer confidence rises to 88.9 in Q4, encouraging sign

New Zealand Westpac Consumer Confidence Index rose notably from 80.2 to 88.9 in Q4, hitting the highest level in nearly two years. Present Conditions Index rose from 69.5 to 77.1. Expected Conditions Index also rose from 87.4 to 96.7.

However, Westpac noted that the index is still below historical average. This means “many more New Zealanders [are] feeling pessimistic about economic conditions.” But it’s important to recognize the positive trajectory reflected in these recent months. The rise in the Consumer Confidence Index is an “encouraging sign,” as noted by Westpac.

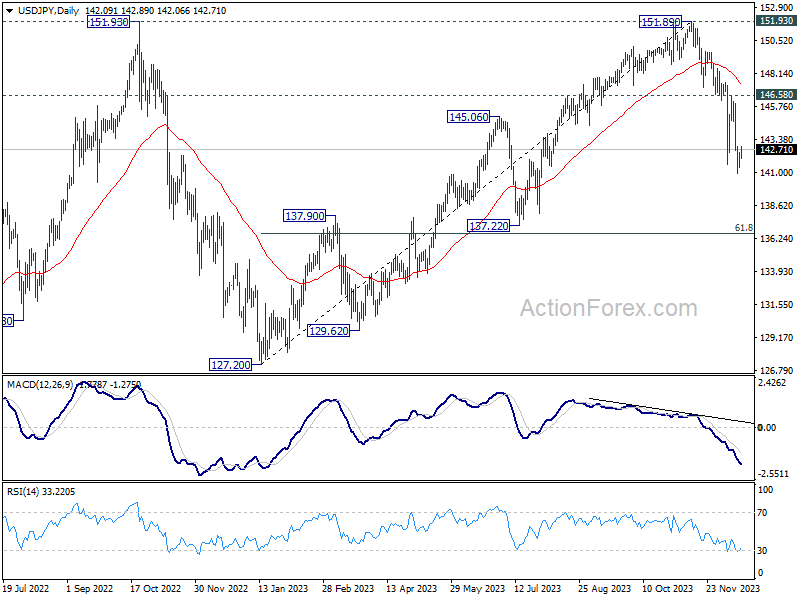

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.57; (P) 142.02; (R1) 142.61; More…

USD/JPY is still extending consolidation from 140.95 and intraday bias remains neutral. Stronger recovery cannot be ruled out. But upside should be limited well below 146.58 resistance to bring another decline. On the downside, break of 140.94 will resume the fall from 151.89 to next fibonacci level at 136.63.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 146.58 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | Westpac Consumer Survey Q4 | 88.9 | 80.2 | ||

| 21:30 | NZD | Business NZ PSI Nov | 51.2 | 48.9 | 49.2 | |

| 09:00 | EUR | Germany IFO Business Climate Dec | 86.4 | 87.8 | 87.3 | |

| 09:00 | EUR | Germany IFO Current Assessment Dec | 88.5 | 89.5 | 89.4 | |

| 09:00 | EUR | Germany IFO Expectations Dec | 84.3 | 85.8 | 85.2 | |

| 13:30 | CAD | New Housing Price Index M/M Nov | -0.20% | 0.10% | 0.00% | |

| 15:00 | USD | NAHB Housing Market Index Dec | 37 | 34 |