The forex markets today are characterized by a lack of decisive direction. Dollar remains generally weak, yet there seems to be a reluctance among sellers to push it further down. Market focus is now shifting to comments from several Fed officials scheduled for today and the rest of the week, as Fed’s blackout period approaches this weekend. However, these comments might not provide significant guidance as officials are likely waiting for more economic data, such as PCE inflation, ISM figures, and next week’s non-farm payrolls, before forming a more defined view on the interest rate path.

Yen’s rally experienced an interruption in European session, although it continues to be one of the strongest performers of the day. This rally has been fuelled by expectations that BoJ will exit its negative interest rate policy in the first half of next year. However, the market’s reaction has been somewhat muted after initial move, as this view aligns with the general understanding that Japan’s wage negotiations next year will play a crucial role in shaping monetary policy.

In other currency market movements, Canadian Dollar emerges as the strongest today, followed by Yen and Australian Dollar. On the weaker side, Swiss Franc is lagging, followed by New Zealand Dollar and Sterling. Euro and Dollar are showing mixed performances.

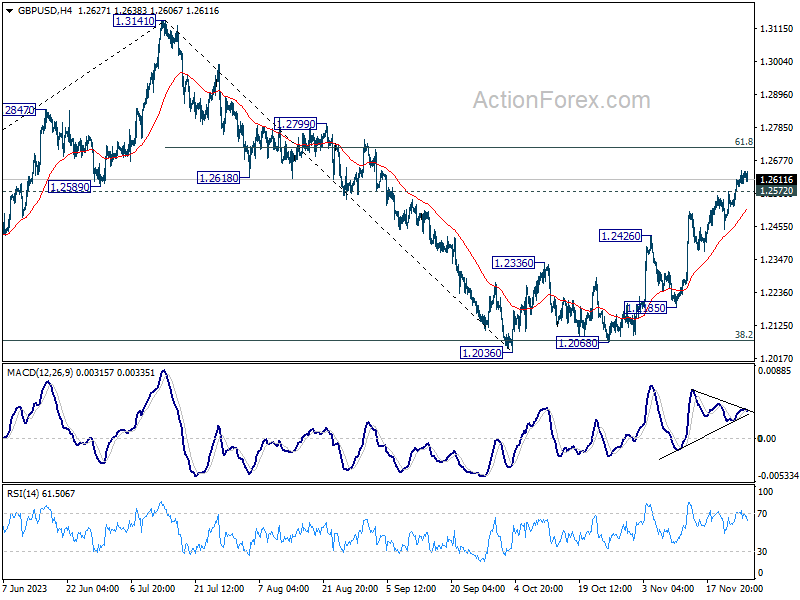

Technically, GBP/USD is losing momentum as seen in 4H MACD. While another rise cannot be ruled out, upside would likely be limited by 61.8% retracement of 1.3141 to 1.2036 at 1.2716 on first attempt. Meanwhile, break of 1.2572 minor support should now indicate short term topping, and bring deeper retreat, and lengthier consolidations. Still, outlook will stay cautiously bullish as long as 1.2426 resistance turned support holds.

In Europe, at the time of writing, FTSE is down -0.41%. DAX is down -0.18%. CAC is down -0.65%. Germany 10-year yield is up 0.0007 at 2.558. Earlier in Asia, Nikkei fell -0.12%. Hong Kong HSI fell -0.98%. China Shanghai SSE rose 0.23%. Singapore Strait Times fell -0.66%. Japan 10-year JGB yield fell -0.0205 to 0.755.

BoE’s Ramsden: Inflation to stay stubbornly high through next year

In an interview with Bloomberg TV today, BoE Deputy Governor Dave Ramsden highlighted that services inflation, accounting for 45% of the consumer basket for CPI inflation, has been unexpectedly resilient at 6.6%. This figure, he noted, is an indication that UK inflation is increasingly becoming “home-grown.”

Ramsden expressed concern over the stubborn nature of inflation, attributing it to factors such as high wage growth, which remains above 7%. Given the labor-intensive nature of UK’s service sector, these wage pressures are a significant contributor to persistent inflation. This situation leads BoE to anticipate that inflation “is going to stay stubbornly high through next year.”

Regarding monetary policy, Ramsden stated that it would need to remain “restrictive for an extended period of time” to effectively bring inflation down from its current level of 4.6% to the Bank’s target of 2%.

Bundesbank’s Nagel: Encouraging inflation outlook doesn’t mean hike cycle is over

In a speech in Cyprus today, Joachim Nagel, ECB Governing Council member and Bundesbank President, described the inflation outlook as “encouraging”. But he was quick to caution that this “that does not necessarily mean that the current hike cycle is now over.”

Nagel emphasized the potential need to raise rates again if the “inflation outlook worsened”

He mentioned that a downside surprise, where price growth returns to ECB’s 2% target quicker than anticipated, is “much less probable.” As a result, Nagel believes it is too soon to even consider the possibility of rate cuts.

On the economic growth front, Nagel projected a rebound next year. He noted that wage growth remains robust and pointed out that the disinflationary effect of falling energy prices has faded.

Nagel also specifically advocated for a “significantly” smaller balance sheet. He stressed his preference to “err on the side of caution” to ensure a timely return to price stability.

Germany’s Gfk consumer sentiment ticks up to -27.8, mood still characterized by uncertainty and concern

Germany’s Gfk consumer sentiment index for December showed a marginal improvement, rising from -28.3 to -27.8, slightly better than expected -28.5. This slight uptick indicates a subtle shift in consumer sentiment as the year ends.

In November, economic expectations had a minor increase from -2.4 to -2.3. However, income expectations dropped from -15.3 to -16.7. There was a slight rise in willingness to buy, from -16.3 to -15.0, while willingness to save decreased from 8.5 to 5.3.

Rolf Bürkl, consumer expert at NIM,noted that “after three consecutive months of decline, consumer sentiment is stabilizing as the year draws to a close.”

Despite this stabilization, Bürkl pointed out that consumer confidence remains at a very low level, with no indications of a sustainable recovery in the upcoming months. He emphasized that the overall mood is still “characterized by uncertainty and concern.”

Australia retail sales down -0.2% mom in Oct, strategic delay for Black Friday

Australia’s retail sales turnover in October displayed an unexpected downturn, falling by -0.2% mom, contrary to the anticipated rise of 0.1% mom. This decline follows a period of growth, with 0.9% mom increase in September and 0.2% mom rise in August.

Ben Dorber, head of retail statistics at ABS, noted “Retail turnover fell in October after a short-lived boost in spending in September.” This downturn was seen across all retail categories except food retailing.

Dorber attributed this pause in consumer spending to a strategic delay by consumers, who are likely waiting to capitalize on Black Friday sales events in November. He observed that this has become a recurring pattern in recent years, with Black Friday sales gaining increasing popularity among consumers.

RBA’s Bullock: we have to be a little bit careful in this period

In a central bank conference held in Hong Kong, RBA Governor Michele Bullock said that monetary policy is currently restrictive, a necessary stance to moderate demand and anchor inflation expectations.

Bullock highlighted the need to be “a little bit careful,” in this period, aiming to control inflation and bring it back within target range of 2-3%, while also being mindful of not overly burdening the economy or causing a significant rise in unemployment rates.

Bullock also pointed out the emergence of “second-round effects” in areas like wages, observing that businesses are currently able to pass on increased costs to maintain profit margins, a trend reflecting sufficient demand.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0933; (P) 1.0946; (R1) 1.0967; More…

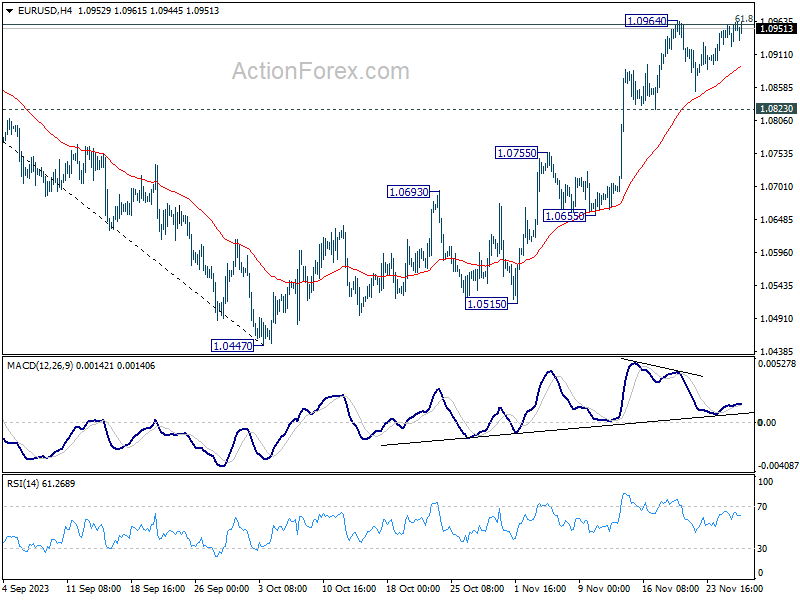

Intraday bias in EUR/USD remains neutral at this point. Consolidation pattern from 1.0964 could still extend further. But after all. further rally is in favor as long as 1.0823 support holds. Sustained break of 61.8% retracement of 1.1274 to 1.0447 at 1.0958 will resume the rise from 1.0447 to retest 1.1274 high. However, firm break of 1.0823 will indicate short term topping, and turn bias back to the downside for deeper decline.

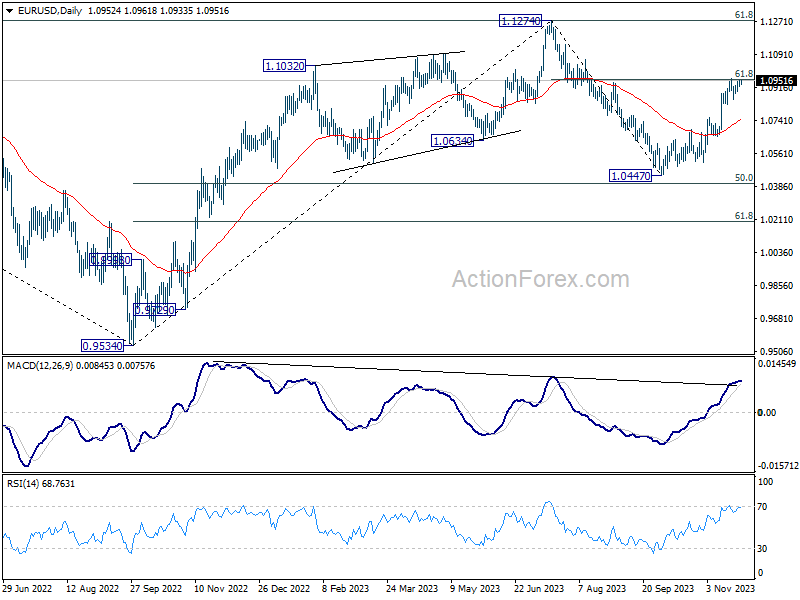

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Oct | 4.30% | 5.20% | ||

| 00:30 | AUD | Retail Sales M/M Oct | -0.20% | 0.10% | 0.90% | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Dec | -27.8 | -28.5 | -28.1 | -28.3 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | -1.00% | -0.90% | -1.20% | |

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Sep | 4.20% | 2.20% | ||

| 14:00 | USD | Housing Price Index M/M Sep | 0.40% | 0.60% | ||

| 15:00 | USD | Consumer Confidence Nov | 101 | 102.6 |