Forex markets are showing unremarkable activity in today’s Asian session, with major currency pairs and crosses largely contained within yesterday’s trading range. The mood this week has been one of indecision, with sporadic movements failing to evolve into sustained trends. Despite China’s intervention to bolster Yuan, the impact was fleeting. Similarly, stronger-than-expected manufacturing data seemed to have little lasting effect on market dynamics. All eyes are now on today’s US Non-Farm Payroll data to see if it can be a catalyst for more enduring shifts.

On weekly performance metric, Australian Dollar has been the star, followed closely by New Zealand Dollar and British Pound. Conversely, Dollar sits at the bottom of the performance list, trailed by Swiss Franc, Euro, the Japanese Yen. This composition hints at a risk-on sentiment prevailing in the markets, a mood underscored by a rebound in major US stock indexes a significant retraction in benchmark yields.

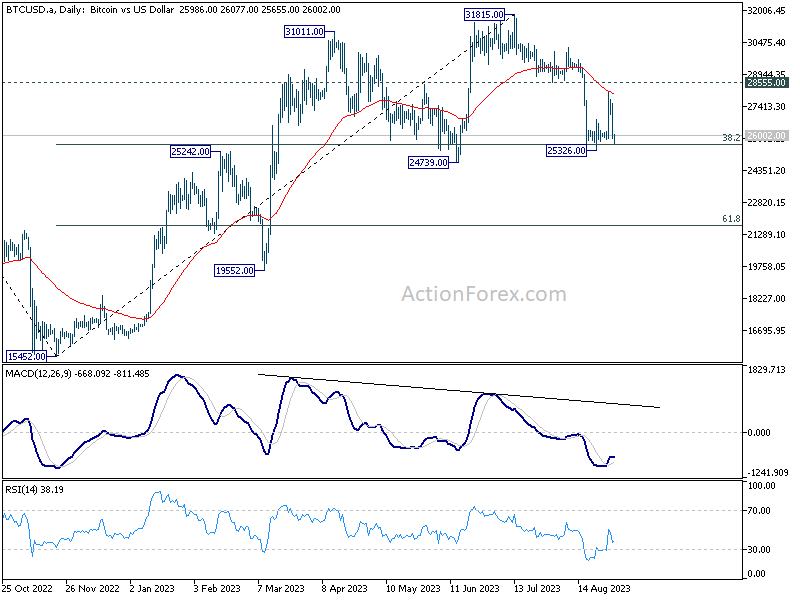

One noteworthy outlier in financial markets has been Bitcoin, which saw a sharp rally to 28146 earlier this week only to relinquish those gains in an overnight selloff. The abrupt reversal followed news that US Securities and Exchange Commission has postponed decisions on approving spot Bitcoin exchange-traded funds from firms like Invesco, WisdomTree, and Valkyrie.

Technically, rejection by 55 D EMA is a bearish sign, suggesting that fall from 31815 is not over yet. The key level now appears to be on 24739 support. Medium term rise from 15452 could still extend higher at a later stage as long as this support holds. Decisive break below this level, however, could open the door to a broader bearish reversal, potentially weighing down sentiment in equities markets, particularly NASDAQ.

In Asia, at the time of writing, Nikkei is up 0.41%. China Shanghai SSE is up 0.39%. Japan 10-year JGB yield down -0.0150 at 0.632. Overnight, DOW dropped -0.48%. S&P 500 dropped -0.16%. NASDAQ rose 0.11%. 10-year yield dropped -0.025 to 4.093.

Japan PMI manufacturing finalized at 49.6, input costs inflation at three-month high

Japan’s PMI Manufacturing remained stagnant at 49.6 in August, indicating a third consecutive month of sectoral contraction. According to Usamah Bhatti at S&P Global Market Intelligence, the rate of deterioration was “unchanged from July and only fractional,” primarily due to a “slower reduction in new orders.”

The report highlighted concerning trends in cost pressures. “Input prices rose at a quicker pace for the first time since September 2022, pushing the rate of input cost inflation to a three-month high,” Bhatti stated. The escalation in input costs was specifically attributed to high raw material prices, labor costs, and a weakened yen.

Despite these pressures, the report found that manufacturers increased their selling prices at the “weakest rate in two years,” indicating that companies may be absorbing the additional costs instead of transferring them to consumers.

The employment situation also emerged as a point of concern. Bhatti noted, “The rate of job creation broadly stalled, with the latest increase the slowest recorded in the 29-month sequence.”

China’s Caixin PMI manufacturing rose to 51, output and employment see uptick

China’s Caixin PMI for manufacturing defied expectations in August, rising from 49.2 to 51.0 and beating market forecasts of 49.4. This indicates a return to expansionary territory. The report noted several key improvements, including increases in output, new business, and a rebound in employment levels. Significantly, input costs rose for the first time since February, suggesting an easing in deflationary pressures.

Wang Zhe, Senior Economist at Caixin Insight Group, elaborated on the data, stating, “In August, the manufacturing sector showed overall improvement. Apart from sluggish exports, the gauges for supply, total demand, and employment were all in expansionary territory.” Wang also noted that the “slight rise in prices buffered the pressure of deflation” and that logistics remained smooth.

However, caution still underlines the market’s medium-term outlook. According to Wang, “Looking ahead, seasonal impacts will gradually subside, but the problem of insufficient internal demand and weak expectations may form a vicious cycle for a longer period of time.” Wang also warned that “combined with the uncertainty in external demand, the downward pressure on the economy may continue to increase.”

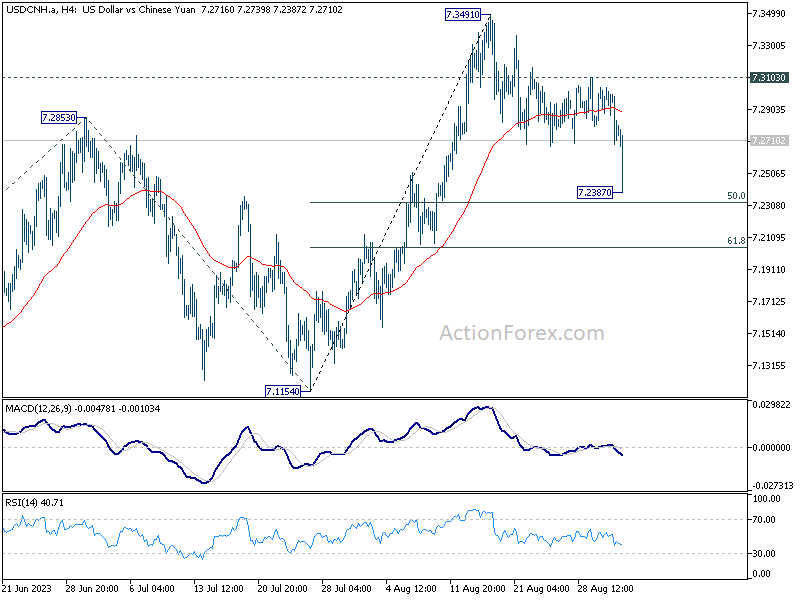

Yuan spikes higher as PBOC slashes FX RRR, but move quickly undone

Chinese Yuan saw a sharp uptick after PBoC announced a substantial 200 bps cut in foreign exchange reserve requirement ratio to 4% from 6%, effective September 15. According to PBoC, the move aims to “improve financial institutions’ ability to use foreign exchange funds.”

This rate RRR is set to release approximately USD 16.4B in foreign exchange, based on China’s FX deposits standing at USD 821.8B as of end-July. Market analysts also note that the FX RRR reduction could have the added effect of lowering dollar funding costs in the interbank market, thereby alleviating some of downward pressure on Yuan.

On the technical front, USD/CNH saw a drop to as low as 7.2387 following the announcement, but it has since recovered most ground. Despite the knee-jerk reaction, the broader uptrend from 6.6971 appears to remain intact. Should it break 7.3103 minor resistance, this would signal completion of the correction from 7.3491 and likely pave the way through 7.3491 for testing 7.3745 high.

However, considering bearish divergence condition in D MACD, strong resistance is likely at 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4091 to limit upside, to complete the five wave sequence from 6.6971.

While technical landscape seems to suggest further upside for USD/CNH, it is crucial to note that these views could be rendered academic at a moment’s notice. The Chinese authorities may implement various intervention measures any time, adding an extra layer of unpredictability to the equation.

Downside risks for NFP, yet market impact may be fleeting

Today, the financial markets are keenly focused on US Non-Farm Payrolls data, which is expected to show growth of 170k jobs in August. While unemployment rate is anticipated to remain steady at 3.50%, average hourly earnings are projected to grow by 0.3% mom. However, related data paint a murkier picture, suggesting that risks could be skewed to the downside for the NFP report. Yet, it’s unsure if the impact on the markets would last long.

Earlier this week, ADP private job growth came in at 177k, slightly missing expectations and dampening the overall employment outlook. Moreover, JOLTS data showed that job openings have plummeted to their lowest level since March 2021, and consumer confidence took a significant hit, dropping from 114.0 to 106.1. The employment components of ISM Manufacturing and Non-Manufacturing reports are not yet available, leaving a gap in the data to fully assess labor market conditions.

Traders have been notably indecisive recently. While it is almost certain that Fed will pause its tightening this month, the likelihood of a rate hike by year’s end seems to be teetering around 50% mark. Market participants are unlikely to get more clarity until the Fed releases its new economic projections and dot plot on September 20, alongside the rate decision.

As for Dollar Index, it’s clearly losing upside momentum as seen in D MACD. While another rise cannot be ruled out as long as 102.84 support holds, strong resistance is likely at 38.2% retracement of 144.77 to 99.57 at 105.37 to limit upside. Break of 102.84 will argue that the corrective rally from 99.57 has completed earlier then expected.

Looking ahead

Swiss CPI and PMI manufacturing, Eurozone and UK PMI manufacturing final will be featured in European session. Later in the day, Canada GDP and US non-farm payrolls are the main events, while US will also release ISM manufacturing.

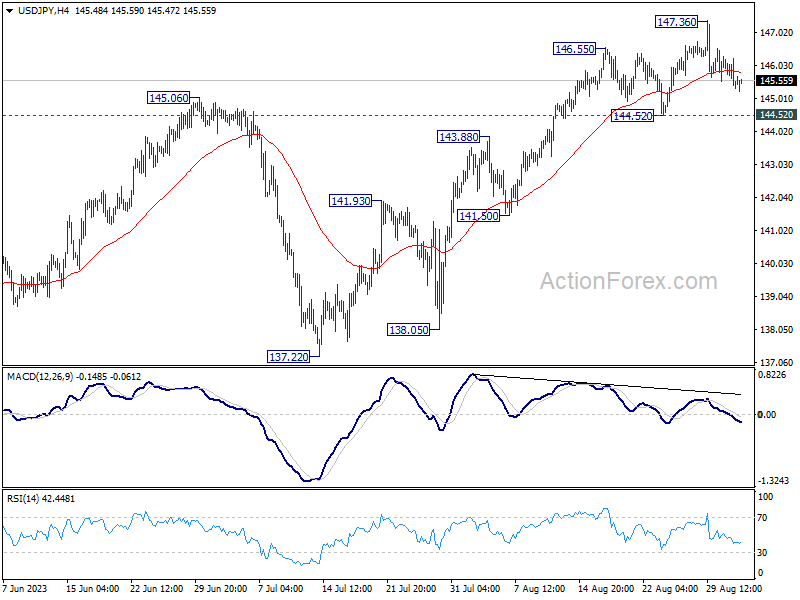

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.17; (P) 145.72; (R1) 146.10; More…

USD/JPY is staying in range of 144.52/147.36 and intraday bias remains neutral. As long as 144.52 support holds, further rally remains in favor. Above 147.36 will resume the rise from 127.20 to retest 151.93 high. On the downside, however, firm break of 144.52 should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 143.04).

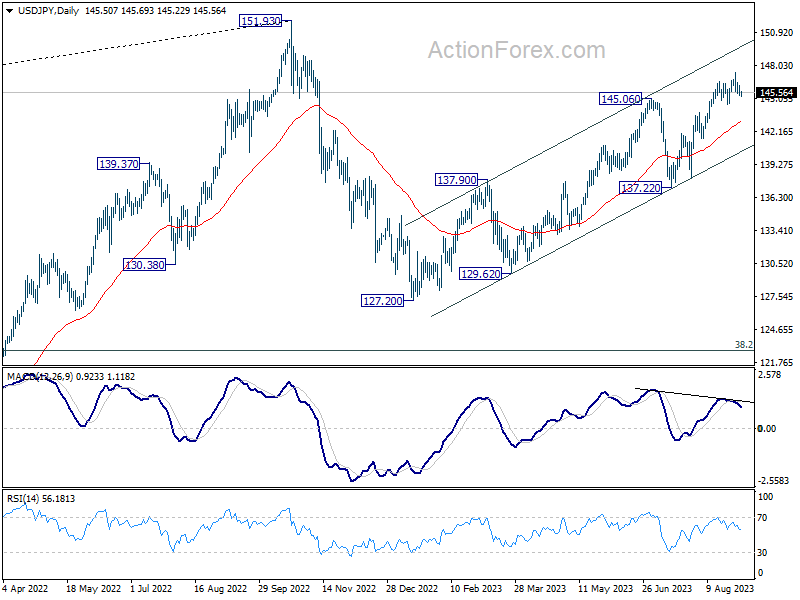

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q2 | 4.50% | 7.90% | 11.00% | |

| 00:30 | JPY | Manufacturing PMI Aug F | 49.6 | 49.7 | 49.7 | |

| 01:45 | CNY | Caixin Manufacturing PMI Aug | 51 | 49.4 | 49.2 | |

| 06:30 | CHF | CPI M/M Aug | 0.20% | -0.10% | ||

| 06:30 | CHF | CPI Y/Y Aug | 1.50% | 1.60% | ||

| 07:30 | CHF | PMI Manufacturing Aug | 41.5 | 38.5 | ||

| 07:45 | EUR | Italy Manufacturing PMI Aug | 45.9 | 44.5 | ||

| 07:50 | EUR | France Manufacturing PMI Aug F | 46.4 | 46.4 | ||

| 07:55 | EUR | Germany Manufacturing PMI Aug F | 39.1 | 39.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | 43.7 | 43.7 | ||

| 08:30 | GBP | Manufacturing PMI Aug F | 42.5 | 42.5 | ||

| 12:30 | CAD | GDP M/M Jun | 0.20% | 0.30% | ||

| 12:30 | USD | Nonfarm Payrolls Aug | 170K | 187K | ||

| 12:30 | USD | Unemployment Rate Aug | 3.50% | 3.50% | ||

| 12:30 | USD | Average Hourly Earnings M/M Aug | 0.30% | 0.40% | ||

| 13:30 | CAD | Manufacturing PMI Aug | 49.6 | |||

| 13:45 | USD | Manufacturing PMI Aug F | 47 | 47 | ||

| 14:00 | USD | ISM Manufacturing PMI Aug | 46.6 | 46.4 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Aug | 42.9 | 42.6 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Aug | 44.4 | |||

| 14:00 | USD | Construction Spending M/M Jul | 0.50% | 0.50% |