Dollar has launched a broad-based rebound in today’s market. However, momentum appears to be faltering against its European counterparts in early U.S. trading session. Although it continues to perform strongly against Yen and Australian dollar, the greenback has been struggling to break last week’s high against other key currencies. Consequently, this rebound seems to be more of a corrective move than a robust up trend. Nevertheless, today’s surge could potentially signal a period of consolidation that might extend through the remainder of the month.

Meanwhile, Euro has suffered broad losses today, driven by disappointing PMI data. While a July rate hike by ECB seems almost certain, the outlook beyond that point is clouded in uncertainty. Australian and New Zealand Dollars, have taken a severe hit following sell-off in Hong Kong stocks and continuous decline in Chinese Yuan. Despite being among the week’s worst performers, Yen is experiencing a slight recovery against other currencies, with the notable exception of Dollar.

In Europe, at the time of writing, FTSE is down -0.57%. DAX is down -1.20%. CAC is down -0.60%. Germany 10-year yield is down -0.165 at 2.335. Earlier in Asia, Nikkei fell -1.45%. 10-year JGB yield dropped -0.0072 to 0.372. Hong Kong HSI fell -1.71%. Singapore Strait Times fell -0.96%.

ECB de Cos: Not appropriate to forecast rates after July hike

ECB Governing Council member Pablo Hernandez de Cos conveyed his anticipation of another interest rate hike. He underscored that ECB’s decisions would continue to rely on key data and inflation outlook.

He stated today, “If the central scenario of our forecasts published by the ECB last week materialises, we will also have to raise 25 basis points again in July.” However, “beyond that it is not appropriate to make any forecasts.”

De Cos highlighted the essential role of key data and inflation dynamics in shaping ECB’s decisions. He added, “we will continue to take our decisions depending on the data and, in particular, on the aggregate assessment of the inflation outlook, the dynamics of underlying inflation.”

Eurozone PMI manufacturing down to 43.6, services down to 52.4

Eurozone PMI Manufacturing fell from 44.8 to 43.6 in June, a 37-month low. PMI Services dropped from 52.4 to 55.1, a 5-month low. PMI Composite tumbled from 52.8 to 50.3, a 5-month low.

HCBO Bank noted in the release that there are diverging trends in the manufacturing and service sectors. Despite falling prices in manufacturing that would typically herald rate cuts, persistent price hikes in the larger service sector continue to slow down core inflation’s decline.

Adding to the complexity are regional differences: France’s service sector contracted in June while Germany’s continues to expand. With Eurozone GDP potentially falling for a third consecutive quarter, the Composite PMI predicts a challenging second half of the year for businesses.

In France, PMI Manufacturing ticked down from 45.7 to 45.5 in June, a 37-month low. PMI Services dropped sharply from 52.5 to 48.0, a 28-month low. PMI Composite fell from 51.2 to 47.3, a 28-month low.

In Germany, PMI Manufacturing fell from 43.2 to 41.0, a 27-month low. PMI Services dropped from 57.2 to 54.1, a 3-month low. PMI Composite declined from 53.9 to 50.8, a 4-month low.

UK PMI manufacturing down to 46.2, Services down to 53.7

UK PMI Manufacturing fell from 47.1 to 46.2 in June, a 6-month low. PMI Services dropped from 55.2 to 53.7, a 3-month low. PMI Composite lowered from 54.0 to 52.8, a 3-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“June’s flash PMI survey indicates that the UK economy has lost momentum again after a brief growth spurt in the spring, and looks set to weaken further in the months ahead.

“Most notably, consumer spending on services, which was a core growth driver in the spring, is now showing signs of faltering… The manufacturing sector meanwhile continues to report recessionary conditions.

“One notable area of resilience in the economy is the labour market…While falling backlogs of work suggest this hiring trend could also fade in the coming months as the economy weakens.

“The survey’s price gauges point to consumer price inflation remaining well above the Bank of England’s target into 2024, which will add to the case for further interest rate hikes…

“Stubbornly elevated price growth in the service sector suggests the Bank of England will consider its fight against inflation as still a work in progress.

Japanese Finance Minister speaks out amid rapid Yen depreciation

As Yen continues to face intense selling pressure, Japanese Finance Minister Shunichi Suzuki reiterated the importance of market-determined exchange rates and the undesirability of abrupt currency movements.

Suzuki stated, “Currency rates should be set by the market, reflecting fundamentals.” He also emphasized the need for stability, saying, “Sharp moves are undesirable, currencies should move stably reflecting fundamentals. With that in mind, we will continue to keep firm watch on market moves.”

His comments come as the USD/JPY surged past the 143 handle, marking a significant acceleration in Yen’s recent depreciation. The slide began last week following BoJ’s decision to maintain its ultra-loose monetary policy stance. Today’s strong inflation data, rather than tempering Yen’s decline, seemed to have had little impact in averting its downtrend.

The verbal intervention from Suzuki underscores the growing concern over the pace and extent of Yen’s depreciation. It also signals the government’s readiness to monitor market trends closely, and possibly intervene should the currency’s movements threaten to undermine the economic fundamentals.

Japan PMI manufacturing fell to 49.8, services down to 54.2

Japan PMI Manufacturing declined from 50.6 to 49.8 in June, below expectation of 50.2. PMI Manufacturing Output fell from 50.9 to 48.3. PMI Services dropped from 55.9 to 5.4.2. PMI Composite decreased from 54.3 to 52.3.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said:

“A fresh fall in manufacturing output coincided with a softer rise in services activity, leading to the weakest expansion of overall output for four months….

“The softening of growth momentum fed through to reduced optimism around the outlook, with business confidence slipping to a five-month low…

“However, there was some better news in terms of inflationary pressures, which showed further signs of easing. Notably, input price inflation softened to a 22-month low in June, while output charges increased at the softest pace since January.”

Australia PMI composite fell to 50.5, RBA has time on their side

Australia PMI Manufacturing ticked up from 48.4 to 48.6 in June. PMI Services fell from 52.1 to 50.7. PMI Composite declined from 51.6 to 50.5.

Warren Hogan, Chief Economic Advisor at Judo Bank said:

“The loss of momentum in recent months will probably give the RBA some comfort that economic activity is slowing down across the economy in 2023, following their consecutive rate hikes in May and June…

“The survey suggests that the RBA has time on their side and does not necessarily need to hike rates again in July. The slowdown taking place across the economy provides further evidence that the point at which the RBA can undertake a genuine pause in their tightening cycle is getting closer.

“We cannot rule out a further hike in the next few months, but we are close to a level of interest rates whereby the RBA can sit back for 4-6 months and observe the effects of past interest rate increases.”

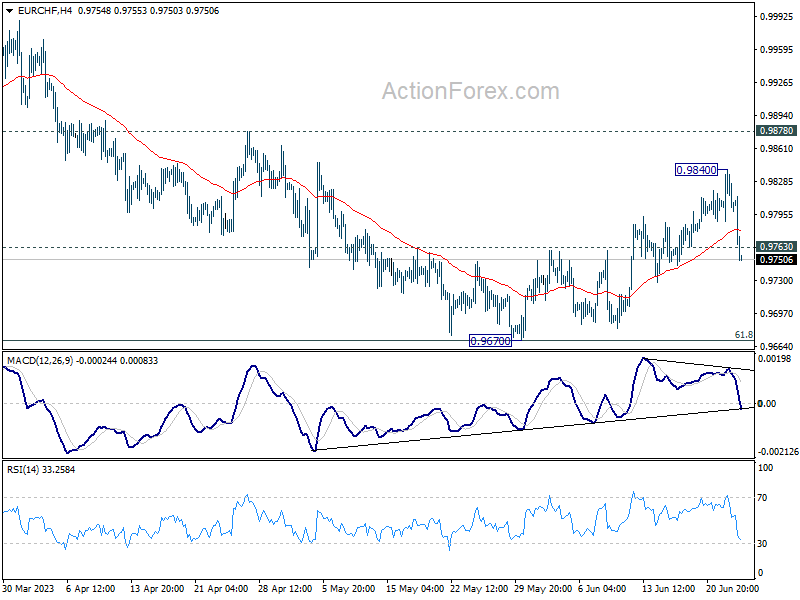

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9783; (P) 0.9812; (R1) 0.9834; More…

EUR/CHF’s break of 0.9763 minor support argues that recovery from 0.9670 has completed as a correction to 0.9840 Intraday bias is back on the downside for retesting 0.9670 low. Sustained break there will resume the whole fall from 1.0095. Nevertheless, break of 0.9840 will resume the rebound to 0.9878 resistance.

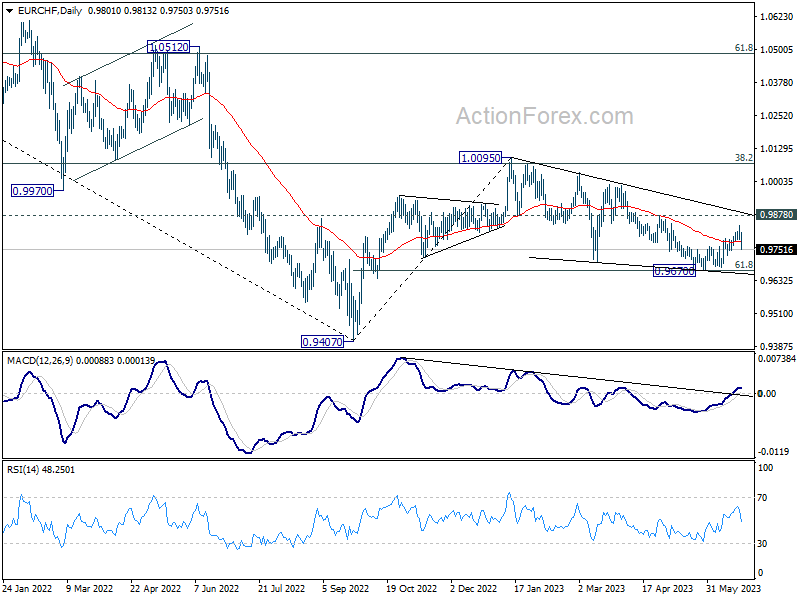

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9924). Down trend from 1.2004 (2018 high) is not complete yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun P | 48.6 | 48.4 | ||

| 23:00 | AUD | Services PMI Jun P | 50.7 | 52.1 | ||

| 23:01 | GBP | GfK Consumer Confidence Jun | -24 | -26 | -27 | |

| 23:30 | JPY | National CPI Y/Y May | 3.20% | 3.50% | ||

| 23:30 | JPY | National CPI Core Y/Y May | 3.20% | 3.10% | 3.40% | |

| 23:30 | JPY | National CPI Core-Core Y/Y May | 4.30% | 4.10% | ||

| 00:30 | JPY | Manufacturing PMI Jun P | 49.8 | 50.2 | 50.6 | |

| 06:00 | GBP | Retail Sales M/M May | 0.30% | -0.20% | 0.50% | |

| 07:15 | EUR | France Manufacturing PMI Jun P | 45.5 | 45.2 | 45.7 | |

| 07:15 | EUR | France Services PMI Jun P | 48 | 52.1 | 52.5 | |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 41 | 43.6 | 43.2 | |

| 07:30 | EUR | Germany Services PMI Jun P | 54.1 | 56.3 | 57.2 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 43.6 | 44.9 | 44.8 | |

| 08:00 | EUR | Eurozone Services PMI Jun P | 52.4 | 54.5 | 55.1 | |

| 08:30 | GBP | Manufacturing PMI Jun P | 46.2 | 46.8 | 47.1 | |

| 08:30 | GBP | Services PMI Jun P | 53.7 | 54.9 | 55.2 | |

| 13:45 | USD | Manufacturing PMI Jun P | 48.5 | 48.4 | ||

| 13:45 | USD | Services PMI Jun P | 54 | 54.9 |