Financial markets are generally leaning towards a risk-on posture, with significant rise in Asia’s Nikkei, following a solid close in the US overnight. However, this momentum will face a series of tests from significant events on the horizon, including today’s US CPI data, tomorrow’s much-anticipated FOMC rate decision, and ECB’s rate decision due on Thursday. Market sentiment will require substantial resilience to weather these potentially market-shifting events.

For the time being, Euro is leading the pack, benefitting from a reversal against both Sterling and Swiss Franc. Meanwhile, the Pound is under pressure and will be seeking some support from today’s employment figures and tomorrow’s GDP data. Australian Dollar is hot on Euro’s heels, with Dollar trailing closely behind. Conversely, Swiss Franc and Sterling are the worse performer. Yen is mixed for now, awaiting guidance from BoJ and bond market developments.

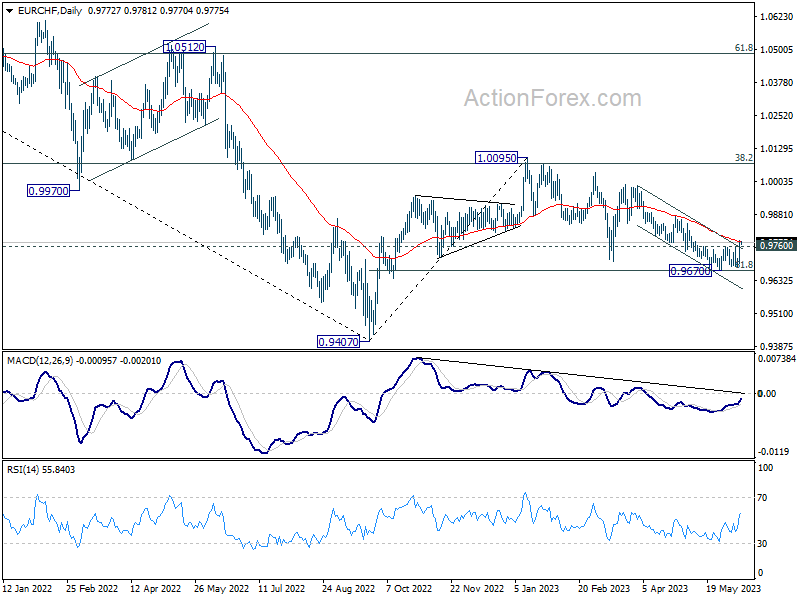

Technically, EUR/CHF’s break of 0.9760 resistance suggests short term bottoming at 0.9670, after hitting 61.8% retracement of 0.9407 to 1.0095 at 0.9670. Sustained trading above 55 D EMA (now at 0.9779) will affirm the case that whole correction from 1.0095 has completed too. Stronger rally would then be seen to 0.9878 resistance next. If realized, the strength in EUR/CHF could help lift Euro against Dollar, Yen and Sterling.

In Asia, at the time of writing, Nikkei is up 1.87%. Hong Kong HSI is up 0.40%. China Shanghai SSE is down -0.06%. Singapore Strait Times is down -0.52%. Japan 10-year JGB yield is down -0.0088 at 0.420. Overnight, DOW rose 0.56%. NASDAQ rose 1.53%. 10-year yield rose 0.020 to 3.765. S&P 500 rose 0.93% and closed above key resistance level at 4325.

Australia Westpac consumer sentiment up 0.2%, dived after RBA hike

Australia Westpac Consumer Sentiment Index rose marginally by 0.2% to 79.2 in June. Nevertheless, the index continues to hover around “recession lows” over the past year, similar to figures recorded during the “deep recessions” of late 1980s/early 1990s.

Significantly, responses gathered within the survey period (June 5-9) reflected the considerable impact of RBA’s unexpected rate hike on June 6. Confidence had seen a substantial surge from 79.0 in May to 89.0 prior to the rate hike announcement. However, it experienced a sharp decline post-announcement, plummeting to a severely low level of 72.6.

Westpac pointed out that inflation continues to be the “dominant drag” on consumer confidence, overshadowing even the effects of higher interest rate Nevertheless,confidence in labor market turned as one consistent positive.

In light of the upcoming RBA meeting on July 4, Westpac forecasts another 25 basis point rate hike, taking the rate to 4.35%. It noted, “Given that little further information will be available on expectations and unit labour costs in the near term it seems logical that delaying the tightening for another month, to assess more data, seems unnecessary”.

Australia NAB business confidence fell to -4, conditions down to -8

Australia’s NAB Business Confidence Index reported a decline in May, dropping from 0 to -4. Furthermore, Business Conditions witnessed a significant drop from 15 to 8. Looking at some details, trading conditions fell from 22 to 14, profitability conditions went down from 12 to 7, and employment conditions also experienced a drop, going from 11 to 4.

“Business conditions recorded a solid decline in May, and it appears the gradual easing we have seen through early 2023 appears to be strengthening,” said NAB Chief Economist Alan Oster. “That said, conditions remain above average reflecting just how strong the economy was through 2022.”

Oster highlighted that “all three sub-components eased in the month, suggesting that demand growth is now moderating, and trading conditions, profitability and employment are beginning to reflect this.”

Business confidence fell back into the negative zone, oscillating within the 0 to -4 index point range in recent months. “Our bigger worry is the sharp decline in forward orders in the month,” Oster noted.

Meanwhile, price measures inched upwards again, yet they remain notably below their mid-2022 peaks. “The trend over the coming months will be important as the RBA tries to assess whether it has done enough and if underlying inflation pressures are easing in a timely way,” Oster noted.

China cuts key short-term policy rate, Yuan depreciation continues

China’s central bank PBOC cut a key short-term policy rate, the seven-day reverse repurchase rate, by -10bps from 2% to 1.9%. The policy change is anticipated to infuse an additional CNY 2B of liquidity into the economy through its seven-day repos.

This marks the first move in the past 10 months, dating back to last August. It follows hot on the heels of the country’s major banks slashing deposit rates last week, which included a decrease in interest rate for five-year time deposits from 2.65% to 2.5%.

The timing of this decision is particularly notable, as it precedes PBoC’s medium-lending facility interest rate announcement, which is set to be unveiled this Thursday. Moreover, the bank’s loan prime rate is scheduled for release on June 20.

Adding to this week’s financial developments, China is expected to publish its May credit lending data along with several key activity indicators such as retail sales and industrial production.

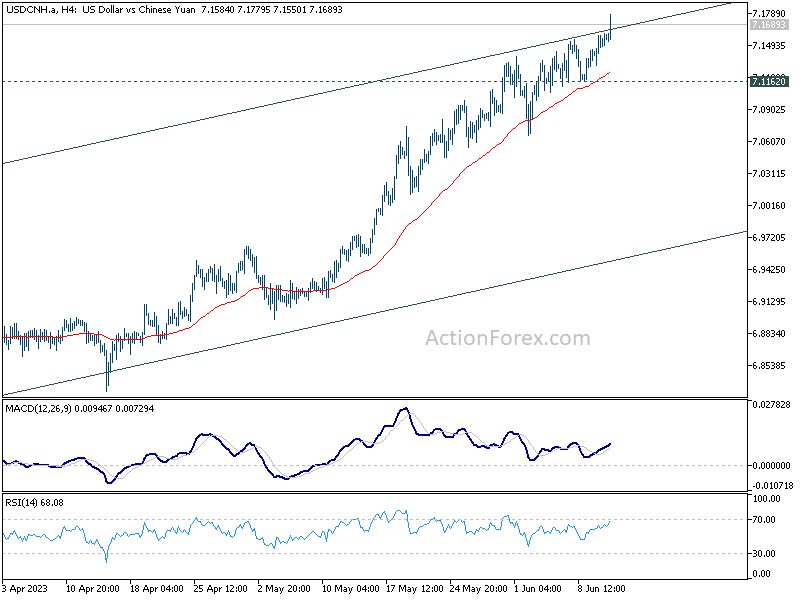

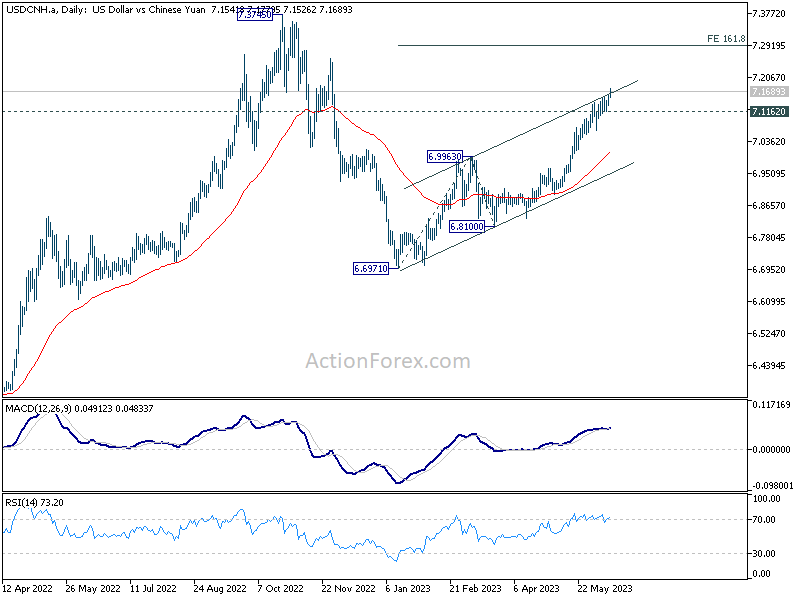

USD/CNH extends recent up trend further to as high as 7.177 after the release, as Yuan’s depreciation continues. From a pure technical perspective, the break of medium term channel resistance is taken as a sign of upside acceleration. Near term outlook will stay bullish as long as 7.1162 support holds. Next target is 161.8% projection of 6.6971 to 6.9963 from 6.8100 at 7.2941. For now, there is no hints that the authority would allow Yuan falls through 7.3 handle, which is close to prior trough at 7.3745.

Looking ahead

UK Employment, Germany CPI final and ZEW economic sentiment will be released in European session. US CPI will be the main feature later in the day.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0731; (P) 1.0760; (R1) 1.0788; More…

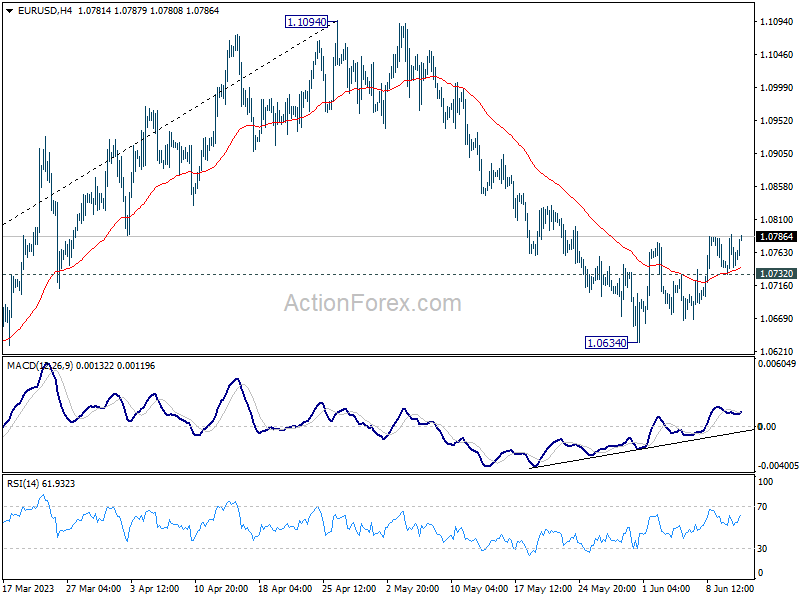

EUR/USD’s rebound from 1.0634 short term bottom is still in progress and intraday bias stays on the upside at this point. Sustained trading above 55 EMA (now at 1.0810) will pave the way back to retest 1.1094 high. Nevertheless, break of 1.0732 minor support should resume the fall from 1.1094 through 1.0634 support.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Index Q2 | -0.4 | -10.5 | ||

| 00:30 | AUD | Westpac Consumer Confidence Jun | 0.20% | -7.90% | ||

| 01:30 | AUD | NAB Business Conditions May | 8 | 14 | ||

| 01:30 | AUD | NAB Business Confidence May | -4 | 0 | ||

| 06:00 | GBP | Claimant Count Change May | 21.4K | 46.7K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Apr | 4.00% | 3.90% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Apr | 6.90% | 6.70% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Apr | 6.10% | 5.80% | ||

| 06:00 | EUR | Germany CPI M/M May F | -0.10% | -0.10% | ||

| 06:00 | EUR | Germany CPI Y/Y May F | 6.10% | 6.10% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jun | -14.7 | -10.7 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jun | -40 | -34.8 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | -13.1 | -9.4 | ||

| 10:00 | USD | NFIB Business Optimism Index May | 88.8 | 89 | ||

| 12:30 | USD | CPI M/M May | 0.30% | 0.40% | ||

| 12:30 | USD | CPI Y/Y May | 4.20% | 4.90% | ||

| 12:30 | USD | CPI Core M/M May | 0.40% | 0.40% | ||

| 12:30 | USD | CPI Core Y/Y May | 5.30% | 5.50% |