Mood is generally positive in Asian session today, with Hong Kong HSI leading other major indexes higher. While the G7 communique released after the meeting in Hiroshima drew furious response from both China and Russia, there was little reactions among investors. Dollar is trading mildly lower, followed by Canadian and Aussie. Kiwi is currently the stronger one as markets await this week’s RBNZ rate hike. Yen is also recovering, followed by Euro and Swiss Franc. But overall, almost all major pairs and crosses are bounded inside Friday’s range.

Investors are likely to focus on a scheduled meeting between US President Joe Biden and Republican House Speaker Kevin McCarthy concerning the contentious issue of raising the debt ceiling. Reiterating her cautionary stance, Treasury Secretary Janet Yellen warned on Sunday that the “hard deadline” of June 1 remains in place for augmenting the debt limit. Yellen expressed concern about the looming deadline, stating, “my assessment is that the odds of reaching June 15 while being able to pay all of our bills is quite low.” Any updates regarding this matter are expected to significantly sway the market.

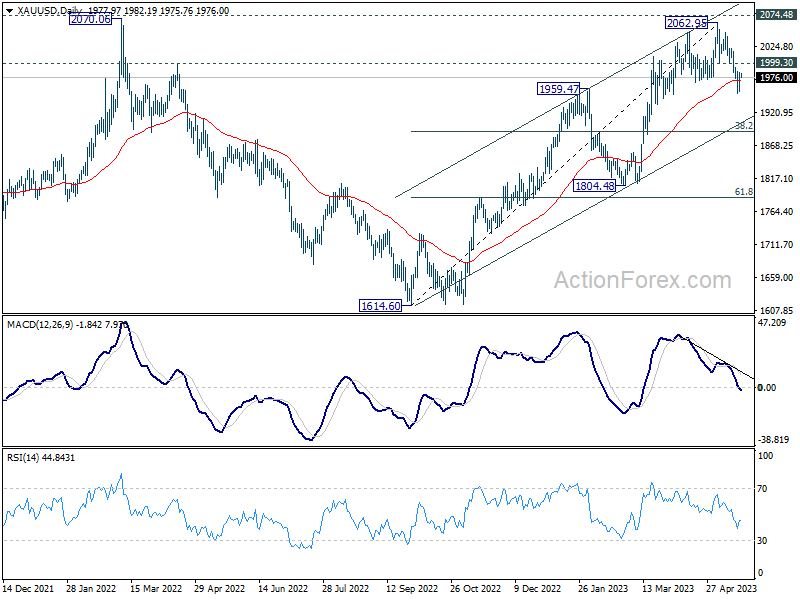

On a technical front, Gold’s recent drop from 2062.95 stalled after hitting a low of 1951.77 last week. Nonetheless, outlook remains the same – the precious metal is seen to be in the process of correcting the rally from its 2022 low at 1614.50. Deeper fall is expected, with a break below 1951.77 targeting 38.2% retracement of 1614.60 to 2062.95 at 1891.68. Yet, breaking minor resistance of 1999.30 would dampen this bearish view, potentially sparking a robust rebound back to 2062.95, or even challenging the record high of 2074.48. The next move in Gold will be used to gauge, or at least confirm, that of Dollar’s as usual.

In Asia, at the time of writing, Nikkei is up 0.39%. Hong Kong HSI is up 1.30%. China Shanghai SSE is up 0.11%. Singapore Strait Times is up 0.08%. Japan 10-year JGB yield is down -0.0185 at 0.389.

ECB’s Lagarde:We are not done yet, we are not pausing

In am interview on the Buitenhof TV show, ECB President Christine Lagarde discussed the bank’s progress in tackling inflation, but refrained from giving forward guidance on the monetary policy.

Lagarde noted significant strides have been made in controlling inflation and bringing it in line with ECB’s target. However, she cautioned that the journey isn’t over yet. “I think we covered a large chunk of the journey toward taming inflation and bringing it back to our target,” she said.

Despite this progress, she made it clear “We are not done yet, we are not pausing based on the information I have today.” And, “inflation outlook is too high and for too long.”

When asked about providing forward guidance, Lagarde expressed caution, citing the potential for various unforeseen factors that could disrupt the economic outlook. “So many things can go wrong that we cannot give what we call forward guidance,” she said. “I don’t have a predetermined number in my mind.”

Lagarde also addressed the ongoing US debt ceiling standoff, emphasizing its potential consequences for both the US and the global economy. “If the United States was to default on its debt it would be a catastrophic development for its economy and for the global economy because of the size of the US economy, because of the depth of its financial sector and because of the totally unpredictable situation that they are facing,” she explained.

Despite these risks, Lagarde expressed optimism that common sense would prevail among US leaders, thus avoiding a severely negative economic development. “I have trust in the common sense and the civic sense of the leaders to reach an agreement — which otherwise would take us into a very, very negative development,” she said.

Fed’s Kashkari: Skipping a meeting is different from “we’re done”

Minneapolis Fed President Neel Kashkari, in an interview with Wall Street Journal, suggested that Fed could afford to adopt a slower pace in its current policy trajectory, while emphasizing that this should not be construed as the end of their monetary tightening efforts.

Expressing his openness to a slower approach, Kashkari stated, “I’m open to the idea that we can move a little bit more slowly from here,”. However, he strongly disagreed with any sentiment that suggested the Fed’s task was complete. “I would object to any kind of declaration that we’re done,” he clarified.

Kashkari went on to argue that skipping a meeting to gather more data could be a sensible decision. “If the committee chooses to skip a meeting because we want to get more information, I could make the argument why that makes sense,” he explained.

He further distinguished this action from an implied cessation of the Fed’s work, saying, “A skip to get more information is very different in my mind than [saying], ‘Hey, we think we’re done.’”

RBNZ shadow board divided on rate hike this week

NZIER disclosed that its RBNZ Shadow Board is in disagreement over whether RBNZ should raise OCR the Official Cash Rate (OCR) this week. A “large number” of the Shadow Board members viewed a 25bps to 5.50% as “warranted”. But “the rest” recommended to hold at 5.25%.

This discord was extended to future projections, as NZIER noted a divergence of opinion regarding where OCR should stand in twelve months.

The Shadow Board acknowledged several recent economic developments that indicated a slowing pace in New Zealand economy, including weaker government tax revenue, decreased consumer spending, and ongoing declines in business profitability.

However, members also recognized potential inflation risks from rising net migration inflows and any new fiscal stimulus in the new Budget.

RBNZ rate hike and FOMC minutes: The week ahead

As we look forward to the forthcoming week, RBNZ is widely anticipated to raise the Official Cash Rate by 25bps to 5.50%, which matches the peak indicate in the February Monetary Policy Statement. The case for a pause following this increment is bolstered by recent economic indicators. Notably, annual inflation in the first quarter receded more than RBNZ projected, dropping to 6.7%. Meanwhile, inflation expectation also fell sharply two-year-ahead inflation expectation also fell to 2.79%, back inside RBNZ’s target band for the first time since December 2021.

However, other developments could prompt RBNZ to prolong the tightening cycle. The newly proposed government budget, perceived by many as inflationary, projects a 2% fiscal impulse of GDP over the 2023/24 period. The repercussions of the recovery from Cyclone Gabrielle and the uptick in net migration also warrant re-evaluation. Therefore, the risks of a 50bps hike – mirroring RBNZ’s action in April – or hints of further tightening, remain plausible.

Turning our gaze to the US, Fed is set to release the minutes from the May FOMC meeting. There are several key questions among market participants. Firstly, is Fed pivoting towards a pause mode? If not, how much further could tightening extend? Finally, when might Fed initiate interest rate cuts? Though these minutes will be under intense scrutiny for answers, they are unlikely to unearth fresh insights unknown to market observers. More significant information may only come to light with new economic projections in June, at the earliest.

In terms of economic data, inflation figures and Purchasing Managers’ Indexes will take centre stage this week. Notable releases include UK CPI and US PCE inflation data. PMIs will be reported by Australia, Japan, Eurozone, UK, and US. Additionally, New Zealand retail sales, Germany’s Ifo business climate index, and US durable goods orders are among the key data points to watch.

Here are some highlights for the week:

- Monday: Japan machine orders; Eurozone consumer confidence.

- Tuesday: Australia PMIs; Japan PMI manufacturing; UK public sector net borrowing, PMIs; Eurozone PMIs; Swiss trade balance; Canada IPPI, RMPI; US PMIs, new home sales.

- Wednesday: New Zealand retail sales; RBNZ rate decision; UK CPI, PPI; Germany Ifo business climate; FOMC minutes.

- Thursday: Germany GDP final, Gfk consumer climate; US GDP revision, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI, corporate services price index; Australia retail sales; UK retail sales; US durable goods orders, personal income and spending with PCE inflation, goods trade balance.

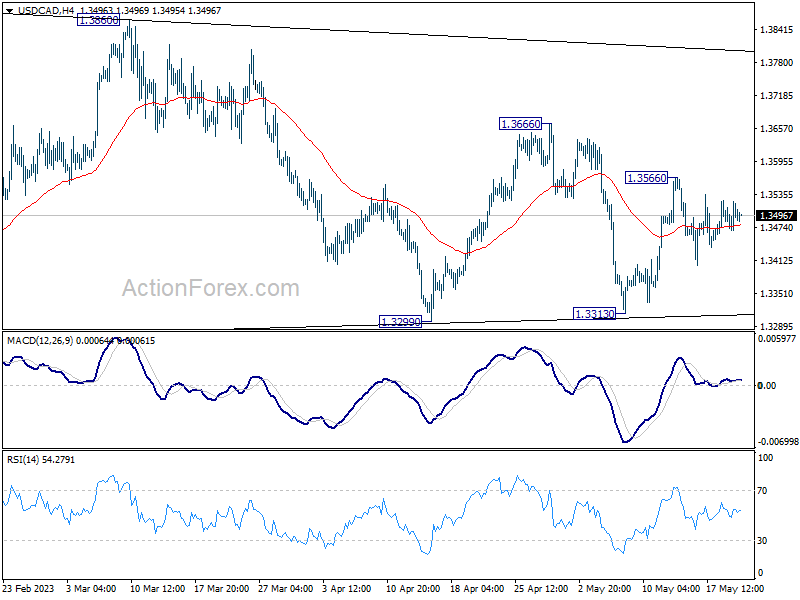

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3470; (P) 1.3496; (R1) 1.3524; More….

Intraday bias in USD/CAD remains neutral as range trading continues. Overall, the pair is seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound from 1.3313 towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

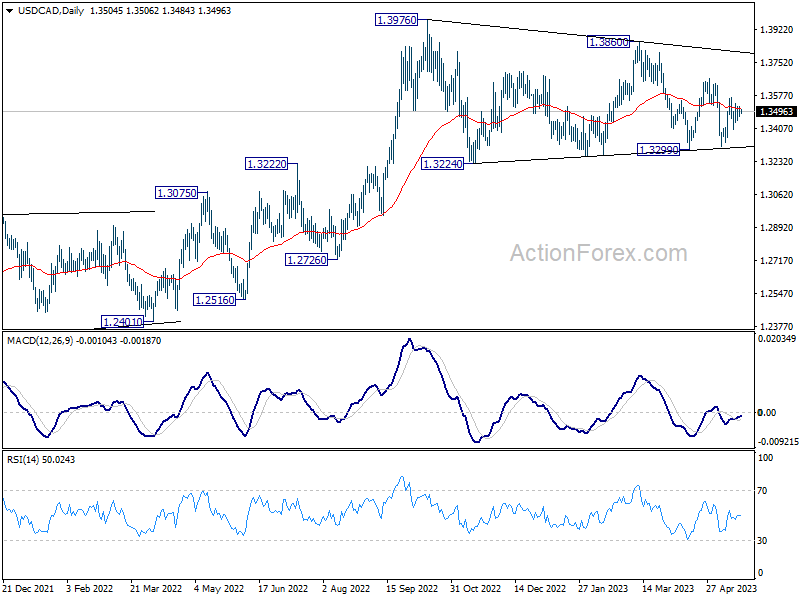

In the bigger picture, as long as 55 W EMA (now at 1.3333) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Mar | -3.90% | 0.70% | -4.50% | |

| 10:00 | EUR | German Buba Monthly Report | ||||

| 14:00 | EUR | Eurozone Consumer Confidence May P | -17 | -18 |