Sterling climbed broadly today following the release of data showing that March’s inflation slowed less than expected, with CPI remaining in double digits. This development supports expectations of a further 25bps rate hike by BOE in May, with some speculating that an additional increase could bring the terminal rate to 4.75% in June. Despite this, Dollar is slightly strong due thanks to rising treasury yields. Canadian Dollar is currently the weakest performer for the day, followed by Japanese Yen and Euro, while Australian and New Zealand Dollars are mixed.

From technical perspective, 10-year treasury yield saw a notable rise in early US session. A close above 3.610 resistance level should confirm short-term bottoming at 3.351, increasing the likelihood that the whole corrective decline from 4.333 has completed with three waves down to 3.51. A stronger rally is expected to return to 4.091 resistance level. If realized, this development could provide additional lift to USD/JPY.

In Europe, at the time of writing, FTSE is down-0.21%. DAX is down -0.17%. CAC is up 0.01%. Germany 10-year yield is up 0.026 at 2.505. Earlier in Asia, Nikkei dropped -0.18%. Hong Kong HSI dropped -1.37%. China Shanghai SSE dropped -0.68%. Singapore Strait Times rose 0.44%. Japan 10-year JGB yield rose 0.0023 to 0.478.

ECB Lane: Markets expect rates to remain at elevated levels for an extended period

ECB Chief Economist Philip Lane noted in a speech that “since the cut-off date for the March 2023 projections, the incoming data have been mixed.”

Lane pointed out the ongoing divergence in sectoral performance, as services business activity experiences accelerated expansion due to strong reopening effects and increased incomes. In contrast, manufacturing output remained stagnant in the first quarter. He also indicated that the consistent improvement in business and consumer sentiment, despite remaining at low levels, appears to have reached a plateau.

Lane mentioned that market pricing and the ECB’s Survey of Monetary Analysts (SMA) foresee that the “policy rate will rise further in the near term and will remain at elevated levels for an extended period.”

He explained that once inflation stabilizes at the 2% target in the medium term, it is projected that the policy rate will settle around 2% instead of returning to ultra-low levels. This expectation is primarily driven by the re-anchoring of long-term inflation expectations at the ECB’s 2% target, indicating that market participants and monetary analysts anticipate the longer-term equilibrium real rate to hover around zero per cent.

Eurozone CPI finalized at 6.9% yoy in Mar, core CPI at 5.7% yoy

Eurozone CPI was finalized at 6.9% yoy in March, down from February’s 8.5% yoy. Core CPI (all items excluding energy, food, alcohol & tobacco) was finalized at 5.7%, up from prior month’s 5.6% yoy. The highest contribution to the annual Eurozone inflation rate came from food, alcohol & tobacco (+3.12%), followed by services (+2.10%), non-energy industrial goods (+1.71%) and energy (-0.05%).

EU CPI was finalized at 8.3% yoy, down from prior month’s 9.9% yoy. The lowest annual rates were registered in Luxembourg (2.9%), Spain (3.1%) and the Netherlands (4.5%). The highest annual rates were recorded in Hungary (25.6%), Latvia (17.2%) and Czechia (16.5%). Compared with February, annual inflation fell in twenty-five Member States and rose in two.

UK CPI slowed to 10.1% yoy, core CPI unchanged at 6.2% yoy

UK CPI slowed from 10.4% yoy to 10.1% yoy in march, above expectation of 9.8% yoy. CPI all goods index slowed from 13.4% yoy to 12.8% yoy. But CPI all services was unchanged at 6.6% yoy. On a monthly basis, CPI rose 0.8% mom, above expectation of 0.5% mom. Core CPI (CPI excluding energy, food, alcohol and tobacco) was unchanged at 6.2% yoy, above expectation of 6.0% yoy.

Also released, RPI was up 0.7% mom, 13.5% yoy, above expectation of 0.6% mom, 13.3% yoy. PPI input was at 0.2% mom, 7.6% yoy, versus expectation of -0.4% mom, 9.8% yoy. CPI output was at 0.1% mom, 8.7% yoy, versus expectation of -0.1% mom, 8.7% yoy. PPI core output was at 0.3% mom, 8/.5% yoy, versus expectation of 0.2% mom, 9.8% yoy.

Australia’s Westpac Leading Index signals below-trend growth, RBA expected to hike rates in May

Australia Westpac-Melbourne Institute Leading Index rose slightly from -0.79% to -0.75% in March, marking the eighth consecutive negative reading. This indicates below-trend growth throughout 2023. Westpac forecasts a modest 1% growth for Australia in 2023, while IMF recently revised its growth forecast for the country from 1.9% to 1.6%. RBA also predicts just 1.6% growth in 2023.

Westpac anticipates a further 25bps increase in the cash rate to 3.85% at RBA’s May 2 meeting. The April RBA minutes revealed additional concerns about the inflation outlook, including rising demand due to increased immigration, pressures in the housing market, and risks associated with growing wage growth, particularly in the public sector. The March quarter inflation report, scheduled for release on April 26, will be a crucial data point for the central bank’s decision-making process.

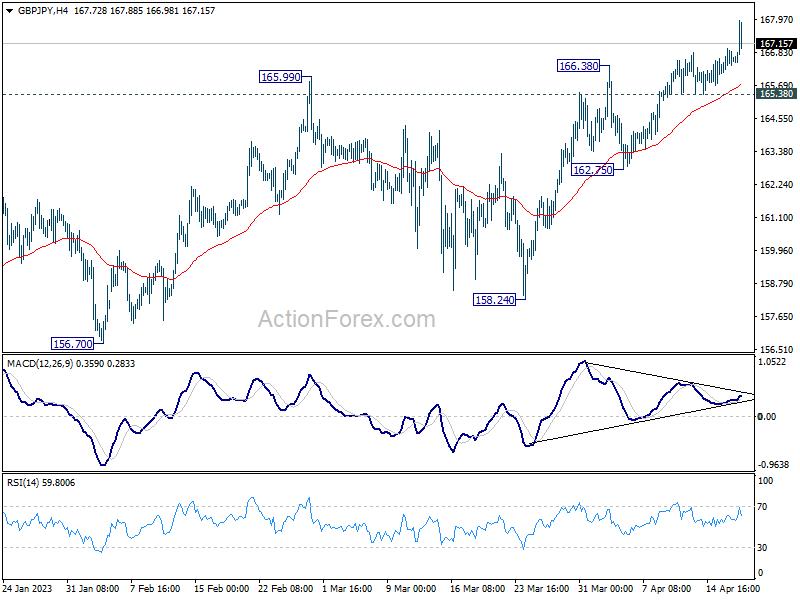

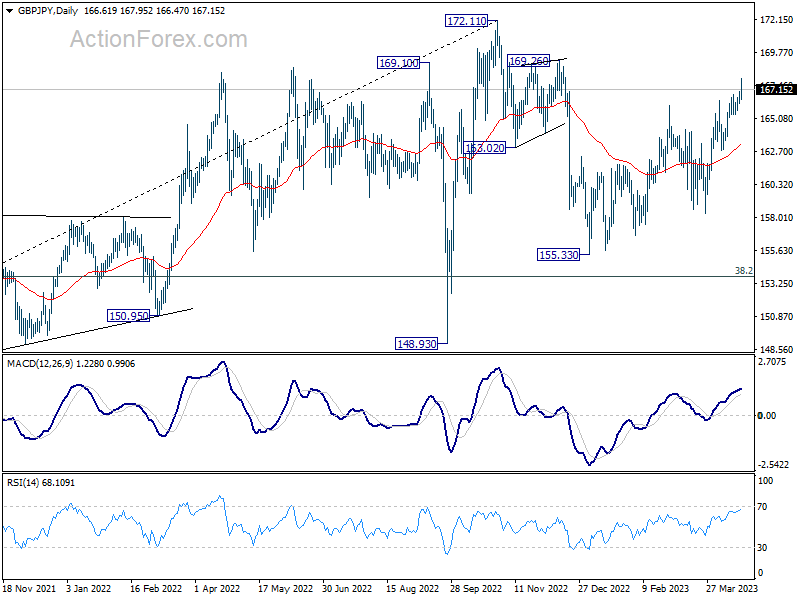

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 166.20; (P) 166.60; (R1) 167.04; More…

GBP/JPY’s rally continues today and hit as high as 167.95 so far. Intraday bias remains on the upside for the moment. Current rally is part of the whole rise from 155.33. Next target is 169.26 resistance first. However, considering bearish divergence condition 4 H MACD. Break of 165.38 minor support will argue that a short term top was already formed. Intraday bias will be turned back to the downside for 162.75 support instead.

In the bigger picture, as long as 38.2% retracement of 123.94 (2020 low) to 172.11 (2022 high) at 153.70 holds, medium term bullishness is retained. That is, larger up trend from 123.94 (2020 low) is still in progress. Break of 172.11 high to resume such up trend is expected at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Mar | 0.00% | -0.06% | ||

| 04:30 | JPY | Industrial Production M/M Feb F | 4.60% | 4.50% | 4.50% | |

| 06:00 | GBP | CPI M/M Mar | 0.80% | 0.50% | 1.10% | |

| 06:00 | GBP | CPI Y/Y Mar | 10.10% | 9.80% | 10.40% | |

| 06:00 | GBP | Core CPI Y/Y Mar | 6.20% | 6.00% | 6.20% | |

| 06:00 | GBP | RPI M/M Mar | 0.70% | 0.60% | 1.20% | |

| 06:00 | GBP | RPI Y/Y Mar | 13.50% | 13.30% | 13.80% | |

| 06:00 | GBP | PPI Input M/M Mar | 0.20% | -0.40% | -0.10% | 0% |

| 06:00 | GBP | PPI Input Y/Y Mar | 7.60% | 9.80% | 12.70% | 12.80% |

| 06:00 | GBP | PPI Output M/M Mar | 0.10% | -0.10% | -0.30% | -0.40% |

| 06:00 | GBP | PPI Output Y/Y Mar | 8.70% | 8.70% | 12.10% | 11.90% |

| 06:00 | GBP | PPI Core Output M/M Mar | 0.30% | 0.20% | -0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y Mar | 8.50% | 9.80% | 10.40% | 10.20% |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 24.3B | 10.3B | 17.1B | 18.6B |

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 6.90% | 6.90% | 6.90% | |

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 5.70% | 5.70% | 5.70% | |

| 12:15 | CAD | Housing Starts Mar | 214K | 260K | 244K | 241K |

| 12:30 | CAD | Industrial Product Price M/M Mar | 0.10% | -0.40% | -0.80% | |

| 12:30 | CAD | Raw Material Price Index Mar | -1.70% | -0.70% | -0.40% | |

| 14:30 | USD | Crude Oil Inventories | -0.4M | 0.6M | ||

| 18:00 | USD | Fed’s Beige Book |