As disinflation process in the US picks up steam, Dollar continues its relentless descent, fueling the belief that Fed’s tightening cycle is close to its curtain call. This evolving sentiment has not only lifted US stocks overnight but also spilled over into Asian session, painting a positive picture for the markets. Despite its recent woes, the greenback is not this week’s weakest performer; that dubious honor goes to Yen, bogged down by unwavering dovish stance of the new BoJ Governor. Meanwhile, Swiss Franc basks in the limelight as the strongest contender, trailed by Aussie, Euro, and Sterling. Amid BoC’s pause earlier in the week, Canadian Dollar remains a mixed bag.

On the technical front, USD/CHF is quickly approaching an important support level at 0.8756 (2021 low). A test on the level could happen in weeks, or even days depending on the intensity of the current selloff in the greenback. Robust support is expected there to bring sustainable rebound back to 0.9058/9439 resistance zone, at least on the first attempt. However, decisive break of the support will break USD/CHF out of a long term range that started back in early 2010s. That would be a significant development if realized.

In Asia, at the time of writing, Nikkei is up 1.14%. Hong Kong HSI is up 0.09%. China Shanghai SSE is up 0.43%. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is down-0.0048 at 0.461. Overnight, DOW rose 1.14%. S&P 500 rose 1.33%. NASDAQ rose 1.99%. 10-year yield rose 0.11 to 3.452.

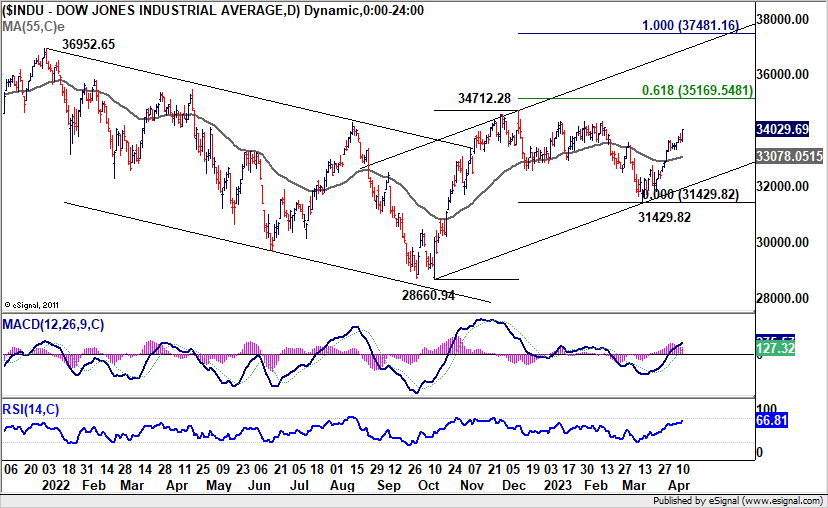

DOW surges as disinflation gains momentum and fed’s tightening cycle nears end

US stocks closed significantly higher overnight, with DOW and S&P 500 extending their near-term rallies. This week’s data supported the view that disinflation is gaining momentum in the US, as evidenced by the notable downside surprise in US PPI and the below-expectation headline CPI readings for March. Additionally, jobless claims data indicated that job market remains stable rather than overheated. The overall picture suggests that while inflation is slowing, the economy isn’t crashing. These factors also contribute to the case that Fed’s tightening cycle is nearing its end, although it remains uncertain when Fed will reverse course.

Technically, DOW’s corrective pattern from 34712.28 should have completed with three waves down to 31429.82. Further rise is now expected as long as 55 D EMA (now at 33078.05) holds. Break of 34712.28 resistance is envisaged as the rally continues. The test for the near term lies in 61.8% projection of 28660.94 to 34712.28 from 31429.82 at 35169.54. Decisive break there could add more fuel to the rally and prompt upside acceleration through. 36952.65 high later in the year.

BoJ Ueda foresees core inflation slowing, reiterates commitment to ultra-loose monetary policy

BoJ Governor Kazuo Ueda, who recently attended the G20 finance leaders’ meeting in Washington, expects core consumer inflation in Japan, currently around 3%, to slow below 2% by the latter half of this fiscal year. Ueda emphasized the central bank’s commitment to maintaining ultra-loose monetary policy in order to achieve its 2% inflation target in a stable and sustainable manner.

Ueda believes that “as our base scenario is for global growth to pick up after a period of slowdown, Japan’s wages will likely keep rising.” He added that the BoJ’s forecasts already factor in the possibility of a global economic slowdown, but a severe global recession is not considered in the baseline projection.

As for the upcoming April policy meeting, Ueda said, “It’s been just a week since I took office and now I am on a business trip. I’ll think about it closely once I’m back.” Market participants are closely watching the BoJ’s first policy meeting under Ueda’s leadership on April 27-28, where the board will release fresh quarterly growth and inflation forecasts extending through fiscal 2025.

NZ BNZ manufacturing dropped to 48.1, sector faces headwinds

New Zealand’s BusinessNZ Performance of Manufacturing Index fell from 51.7 in February to 48.1 in March, slipping back into negative territory after briefly reaching positive levels in January and February. The decline in the index signals challenges for the manufacturing sector.

A closer look at the data reveals that production dropped from 48.7 to 43.3, its lowest level since August 2021. Employment shrank from 55.2 to 47.1, while new orders dipped from 51.5 to 46.7, matching November 2022 levels. Finished stocks decreased from 55.1 to 48.4, and deliveries rose slightly from 52.2 to 53.8.

Catherine Beard, BusinessNZ’s Director of Advocacy, pointed out that the numbers behind the main March result indicate the manufacturing sector is facing significant headwinds. BNZ Senior Economist Craig Ebert added that although New Zealand’s March PMI was disappointing, it was “not especially negative in the longer-term context” and was in line with global manufacturing readings.

Looking ahead

Swiss PPI is the only feature in the European session. Later in the day, main focus in US retail sales, and import prices, industrial production and U of Michigan consumer sentiment will be released. Canada will also release manufacturing sales.

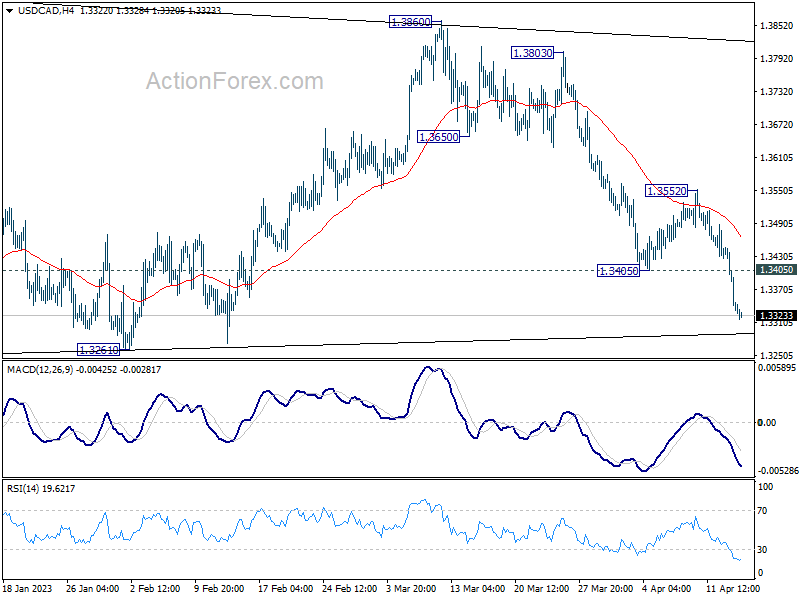

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3299; (P) 1.3373; (R1) 1.3414; More….

Intraday bias in USD/CAD stays on the downside fall the momentum. Fall from 1.3860, which is seen as the third leg of the corrective pattern from 1.3976, is in progress for 1.3224/61 support zone. Strong support is expected there to complete the corrective pattern and bring rebound. On the upside, above 1.3405 support turned resistance will turn intraday bias neutral first. Further break of 1.3552 will indicate near term reversal.

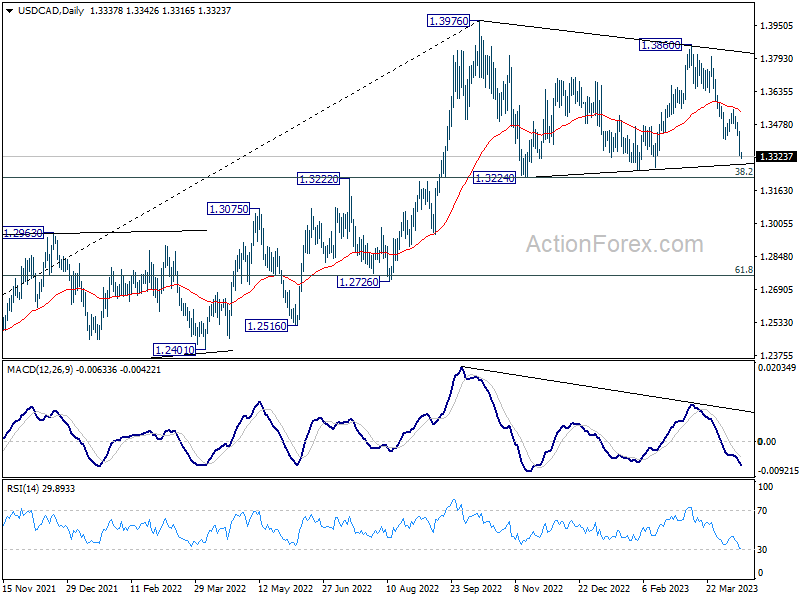

In the bigger picture, the up trend from 1.2005 (2021 low) is still in progress. Break of 1.3976 will confirm resumption and target 61.8% projection of 1.2401 to 1.3976 from 1.3261 at 1.4234. Firm break there will pave the way to long term resistance zone at 1.4667/89 (2016, 2020 highs). On the downside, sustained break of 55 week EMA (now at 1.3282) is needed to confirm medium term topping. Otherwise, outlook will remain bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Mar | 48.1 | 51 | 52 | |

| 06:30 | CHF | Producer and Import Prices M/M Mar | -0.20% | -0.20% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Mar | 2.70% | 2.70% | ||

| 12:30 | CAD | Manufacturing Sales M/M Feb | -2.50% | 4.10% | ||

| 12:30 | USD | Retail Sales M/M Mar | -0.50% | -0.40% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Mar | -0.40% | -0.10% | ||

| 12:30 | USD | Import Price Index M/M Mar | -0.20% | -0.10% | ||

| 13:15 | USD | Industrial Production M/M Mar | 0.20% | 0.00% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr P | 62.7 | 62 | ||

| 14:00 | USD | Business Inventories Feb | 0.20% | -0.10% |