Euro is trading mildly higher today following indications from a key ECB official that more interest rate hikes are in the pipeline for the central bank. Concurrently, the improving market sentiment across Europe is lending support to both Sterling and the Swiss Franc. However, Canadian Dollar emerges as the strongest for the day, fueled by robust oil prices.

Conversely, Yen is facing widespread pressure as European benchmark treasury yields continue their rebound. Australian and New Zealand Dollars trail closely behind as the next weakest. Dollar’s performance is mixed at the moment, but its recovery against Yen could potentially decelerate the greenback’s decline elsewhere.

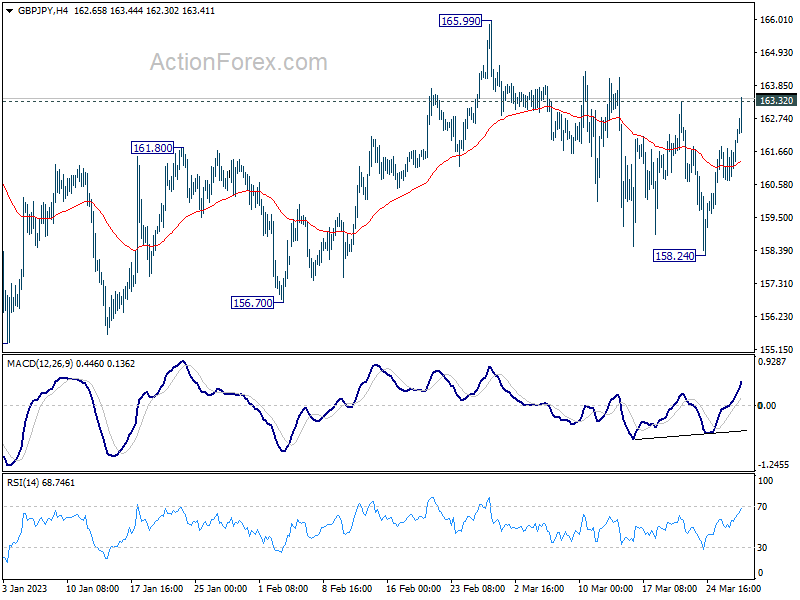

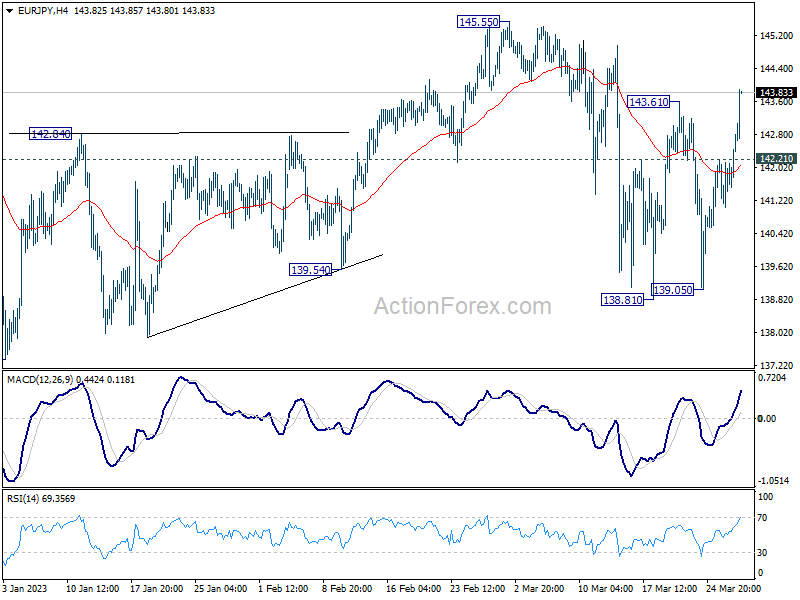

From a technical standpoint, EUR/JPY’s break of the 143.61 resistance level suggests that the pullback from 145.55 has already concluded. Further gains are expected to retest 145.55, with a break there extending the rebound from 137.37. Attention is also focused on GBP/JPY, which is currently pressing 163.32. A break at that level would align the outlook with EUR/JPY and trigger a more substantial rise to 165.99. A firm break there would resume the overall rebound from 155.33.

In Europe, at the time of writing, FTSE is up 0.93%. DAX is up 0.90%. CAC is up 1.26%. Germany 10-year yield is up 0.035 at 2.321. Earlier in Asia, Nikkei rose 1.33%. Hong Kong HSI rose 2.06%. China Shanghai SSE dropped -0.16%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield dropped -0.077 to 0.307.

ECB Lane indicates more hikes needed to tame inflation

ECB Chief Economist Philip Lane, in an interview with German newspaper Die Zeit, emphasized the necessity for further interest rate hikes to ensure that inflation returns to the 2% target. Lane stated, “Under our baseline scenario, in order to make sure inflation comes down to 2%, more hikes will be needed.”

He also suggested that even in cases of limited financial stress, interest rates would still need to rise. “If the financial stress we see is non-zero, but turns out to be still fairly limited, interest rates will still need to go up,” he said.

Meanwhile, Lane expressed optimism about moderating price pressures at earlier stages of production, which are expected to eventually impact consumer prices. “If you look at the earlier stages of production, at the farm gate prices, at the prices of the food ingredients, you will recognize: all of these have turned around,” he said.

The chief economist also dismissed the notion that a recession is required to bring inflation down, asserting that a soft landing for the economy is possible. Lane believes that the pandemic recovery can continue alongside decreasing inflation, as he noted, “We’ve lost so much growth momentum in the pandemic that it’s possible for the pandemic recovery to continue and for inflation to come down simultaneously.”

Germany Gfk consumer sentiment ticked up to -29.5, hindered by purchasing power concerns

Germany’s GfK consumer sentiment index for April posted a modest improvement for the sixth consecutive month, rising from -30.6 to -29.5, although it fell short of the expected -29.0. In March, economic expectations for dipped from 6.0 to 3.7, while income expectations increased from -27.3 to -24.3. Propensity to buy also saw a slight uptick from -17.3 to -17.0.

GfK consumer expert Rolf Bürkl attributes the improved income expectations to the recent decline in energy prices, particularly for gas and heating oil. However, Bürkl cautions that inflation will remain elevated this year, albeit lower than the 6.9% recorded in 2022.

He explains, “The expected loss of purchasing power is preventing a sustained recovery in domestic demand. Accordingly, private consumption is unlikely to make a positive contribution to economic growth in Germany this year.” This outlook is reinforced by the persistently low level of consumer sentiment.

Australia CPI slowed to 6.8% yoy, supports RBA pause next week

Australia’s monthly CPI in February eased from 7.4% yoy to 6.8% yoy, below expectation of 7.2% yoy. CPI excluding volatile items such as fruit, vegetables, and automotive fuel also slowed from 7.5% yoy to 6.9% yoy.

Michelle Marquardt, Head of Prices Statistics at the Australian Bureau of Statistics (ABS), noted that “this marks the second consecutive month of lower annual inflation, also known as ‘disinflation’, from the peak of 8.4% in December 2022.”

Although inflation remains well above RBA’s target band of 2-3%, the start of disinflation process could increase the likelihood of a pause in the RBA’s tightening cycle during their next meeting. The continued easing of inflationary pressures may prompt the central bank to take a more cautious approach in the near term.

Incoming BoJ Deputy Governor Uchida Stresses Importance of Trend Inflation in Monetary Policy

Incoming BoJ Deputy Governor Shinichi Uchida emphasized the significance of trend inflation in a parliamentary session today, stating that the central bank will conduct a comprehensive assessment of various data, including trend inflation developments, to guide monetary policy.

Uchida said that “trend inflation is an extremely important factor for us in judging on achievement of 2% inflation target in a stable manner.” He also mentioned that the BoJ will “make comprehensive judgment by looking at various price indicators.”

In addition, Uchida highlighted the importance of communication between the central bank and the markets, saying, “We will strive to communicate firmly with markets to gain understanding” regarding the BoJ’s policy approach. This statement underscores the commitment of the BoJ to transparency and open dialogue in shaping its monetary policy.

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.30; (P) 141.73; (R1) 142.40; More….

EUR/JPY’s break of 143.61 resistance now argues that pull back form 15.55 has completed at 138.81 already. Intraday bias is back on the upside for 145.55 resistance first. Break there will resume the whole rebound from 137.37 and target a test on 148.38 high. On the downside, though, below 142.21 minor support will mix up the outlook again and turn intraday bias neutral.

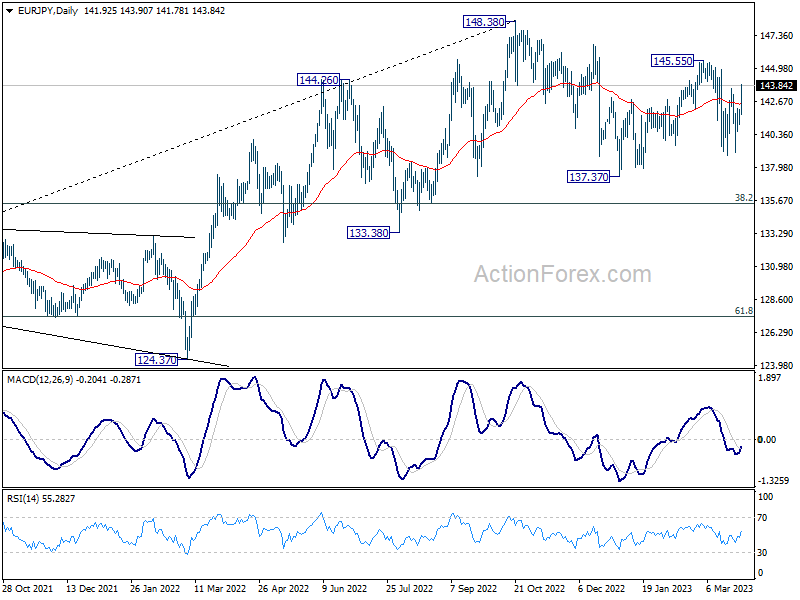

In the bigger picture, as long as 55 week EMA (now at 139.58) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance. However, sustained break of 55 week EMA will bring deeper fall to 38.2% retracement of 114.42 to 148.38 at 135.40. Decisive break there will raise the chance of trend reversal, and target 61.8% retracement at 127.39.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Feb | 6.80% | 7.20% | 7.40% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Apr | -29.5 | -29 | -30.5 | -30.6 |

| 08:00 | CHF | Credit Suisse Economic Expectations Mar | -41.3 | -12.3 | ||

| 08:30 | GBP | Mortgage Approvals Feb | 44K | 42K | 40K | |

| 08:30 | GBP | M4 Money Supply M/M Feb | -0.40% | 0.90% | 1.30% | 1.20% |

| 13:00 | CHF | SNB Quarterly Bulletin | ||||

| 14:00 | USD | Pending Home Sales M/M Feb | -2.20% | 8.10% | ||

| 14:30 | USD | Crude Oil Inventories | 1.8M | 1.1M |