Australian Dollar strengthens further with mildly positive risk sentiment in Asia. But other major currencies are sluggish. Yen is still recovery but apparently lacks committed buying. Canadian Dollar is staying soft after yesterday’s BoC hike, but selloff is relatively limited. Euro is having a slight upper hand against Dollar, but both are actually mixed. Focuses will now turn to US GDP today, and then PCE inflation tomorrow.

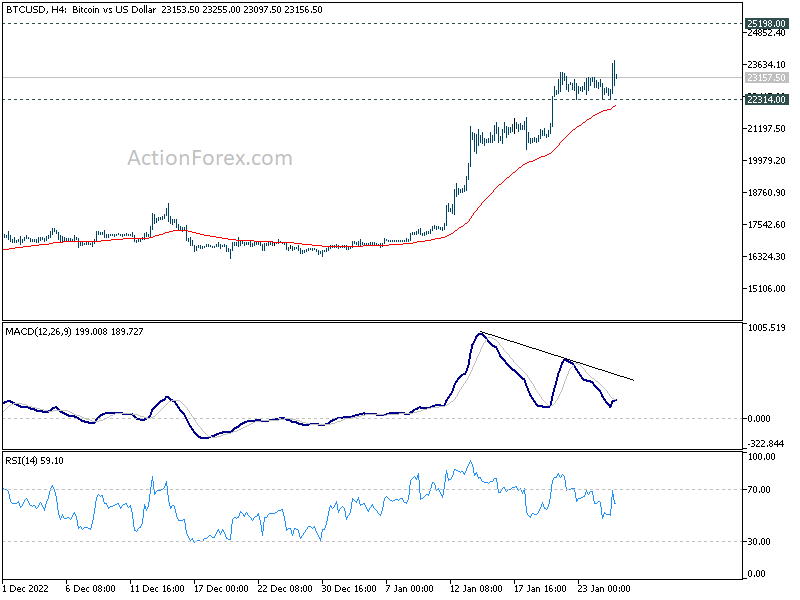

Technically, Bitcoin is extending near term rally today, but continues to lose upside momentum as seen in 4 hour MACD. For now further rise is in favor as long as 22314 support holds, towards 25198 medium term resistance. However, break of 22314 will indicate near term topping and bring some consolidations first. Bitcoin’s next move will be used as a hint on the development in broader risk sentiment.

In Asia, at the time of writing, Nikkei is down -0.20%. Hong Kong HSI is up 1.76%. Singapore Strait Times is up 0.65%. Japan 10-year JGB yield is up 0.0137 at 0.458. China is still on holiday. Overnight, DOW rose 0.03%. S&P 500 dropped -0.02%. NASDAQ dropped -0.18%. 10-year yield dropped -0.007 to 3.462.

BoJ Opinions: Necessary to take some time to examine effect of YCC change

In the Summary of Opinions at BoJ’s January 17-18 monetary policy meeting, it’s repeated noted that it’s important to continue with current monetary easing as well as yield curve control.

The modification of YCC at the December meeting was “aimed solely at making monetary easing more sustainable”. It is “necessary” to “take some time” to examine the effects of the change in YCC.

One member noted the “upward pressure” on long-term interest rates and the distortions on the yield curve. And, BoJ “should curb interest rate rises across the entire yield curve through measures”.

Regarding prices, CPI is expected to fall below 2% from fiscal 2023, and there is “still a long way to go to achieve the price stability target”.

But opinions were more upbeat as one noted that “momentum for wage hikes has grown, and it is possible that a certain degree of base pay increases will be realized”. But it still takes time for wages to see a “sustained increase”.

Firms’ stance has “shifted toward actively raising their selling prices” as seen in the outlook for output prices. Pace of rises in prices of both goods and services is “accelerating”. It’s possible that the significant price shocks since last week will “change the norm for prices”.

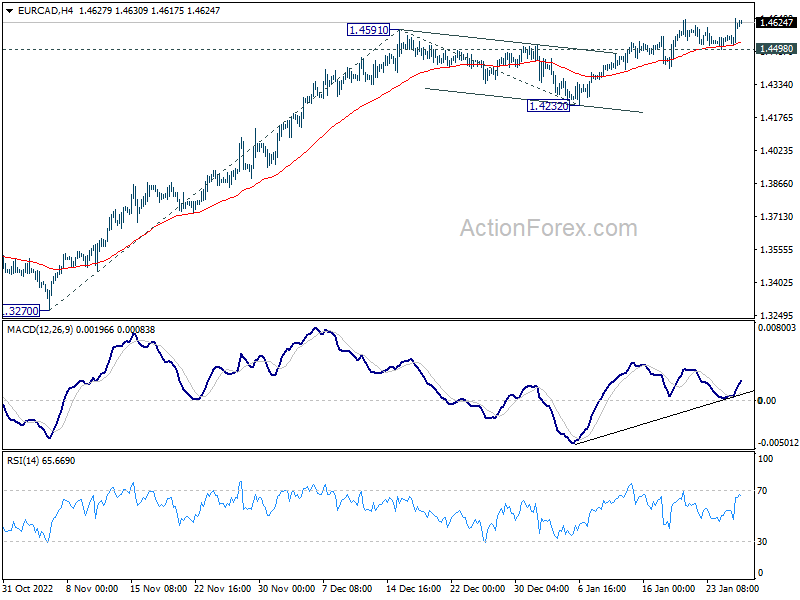

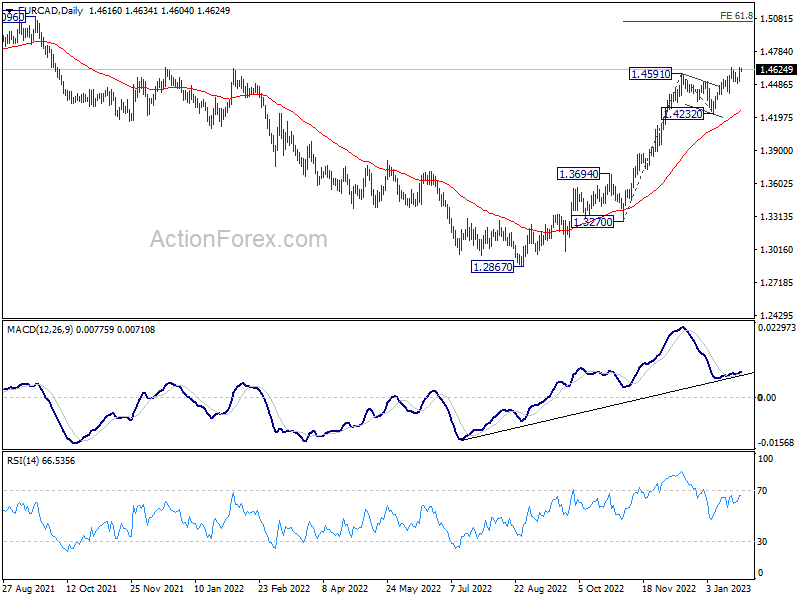

EUR/CAD resuming up trend, CAD softens after BoC

Canadian Dollar is trading as the worst performer for the week so far, after BoC raised interest rate by a final 25bps in the current cycle. A pause will follow for the impacts of previous tightening to pass through to the economy.

EUR/CAD’s breach of 1.4639 temporary top suggests that larger up trend from 1.2867 is resuming. Further rally is now expected as long as 1.4498 support holds. Next target is 61.8% projection of 1.3270 to 1.4591 from 1.4232 at 1.5048. Break of 1.4498 will bring more consolidations before staging another rally.

Looking ahead

The European calender is empty today. Focuses are on US Q4 GDP, durable goods orders, jobless claims, goods trade balance and new home sales.

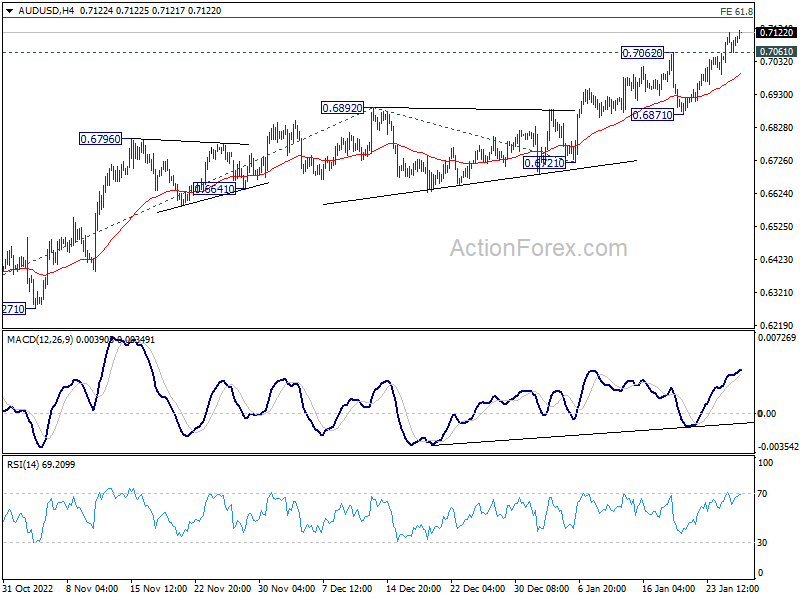

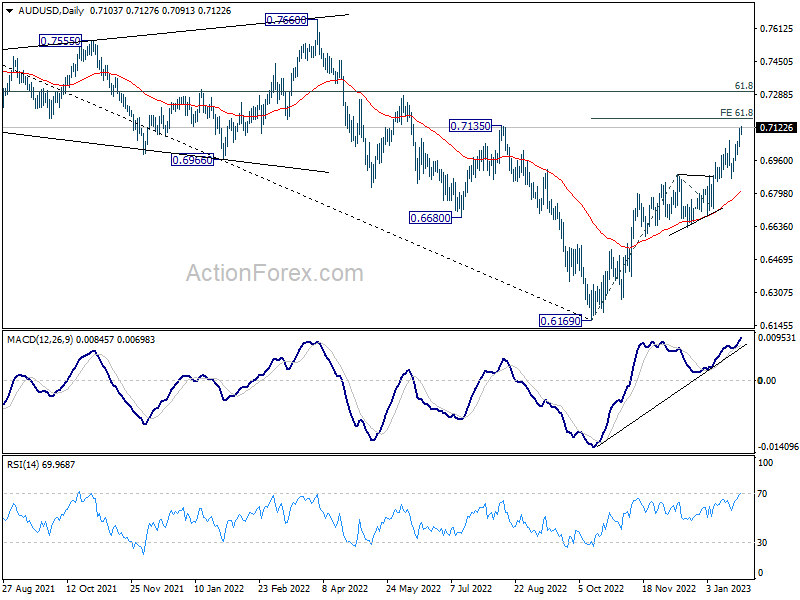

AUD/USD Daily Report

Daily Pivots: (S1) 0.7050; (P) 0.7086; (R1) 0.7141; More…

Intraday bias in AUD/USD remains on the upside at this point. Current rise from 0.6169 should target 61.8% projection of 0.6169 to 0.6892 from 0.6721 at 0.7168 next. Break there will target 0.7304 fibonacci level. On the downside, below 0.7061 minor support will turn bias neutral and bring consolidations. But outlook will stay bullish as long as 0.6871 support holds, in case of retreat.

In the bigger picture, corrective decline from 0.8006 (2021 high) should have completed with three waves down to 0.6169 (2022 low). Further rally should be seen to 61.8% retracement of 0.8006 to 0.6169 at 0.7304. Sustained break there will pave the way to retest 0.8006. This will now remain the favored case as long as 0.6721 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Corporate Service Price Index Y/Y Dec | 1.50% | 1.60% | 1.70% | |

| 13:30 | USD | Initial Jobless Claims (Jan 20) | 211K | 190K | ||

| 13:30 | USD | GDP Annualized Q4 P | 2.80% | 3.20% | ||

| 13:30 | USD | GDP Price Index Q4 P | 6.20% | 4.40% | ||

| 13:30 | USD | Goods Trade Balance (USD) Dec P | -88.8B | -83.3B | ||

| 13:30 | USD | Wholesale Inventories Dec P | 0.50% | 1.00% | ||

| 13:30 | USD | Durable Goods Orders Dec | 2.50% | -2.10% | ||

| 13:30 | USD | Durable Goods Orders ex Trans Dec | 0.00% | 0.20% | ||

| 15:00 | USD | New Home Sales Dec | 615K | 640K | ||

| 15:30 | USD | Natural Gas Storage | -79B | -82B |