Australian Dollar rises broadly today after strong CPI data supports continuation of tightening by RBA. On the other hand, New Zealand CPI didn’t accelerate as RBNZ projected, and markets are lowering their expectation on the terminal rate. Kiwi, thus falls broadly. Canadian Dollar is firm as focus turns to BoC rate decision, where a final “insurance” hike is expected in the current cycle. As for the week, Aussie is the strongest, followed by Euro. Yen is the worst, followed by Sterling. Dollar is mixed in between.

In Asia, Nikkei closed up 0.35%. Japan 10-year JGB yield rose 0.249 to 0.437. Singapore Strait Times is up 1.66%. Hong Kong and China are still on holiday. Overnight, DOW rose 0.31%. S&P 500 dropped -0.07%. NASDAQ dropped -0.27%. 10-year yield fell -0.056 to 3.469.

New Zealand CPI unchanged at 7.2% yoy in Q4

New Zealand CPI rose 1.4% qoq in Q4, slightly below expectation of 1.5% qoq. Annual CPI was unchanged at 7.2% yoy, above expectation of 7.1% yoy, comparing to the peak at 7.3% yoy in Q2.

StatsNZ said, “Housing and household utilities was the largest contributor to the December 2022 annual inflation rate. This was due to rising prices for both constructing and renting housing.”

The quarterly rise in inflation was “influenced by rising prices in the housing and household utilities, food, and recreation and culture groups.”

Australia CPI rose to 8.4% yoy in Dec, 7.8% yoy in Q4

Australia CPI rose 1.9% qoq in Q4, above expectation of 1.7% qoq. Annual CPI accelerated from 7.3% yoy to 7.8% yoy, above expectation of 7.5% yoy. RBA trimmed mean CPI also accelerated from 6.1% yoy to 6.9% yoy, above expectation of 6.5% yoy.

Michelle Marquardt, ABS head of prices statistics, said “This is the fourth consecutive quarter to show a rise greater than any seen since the introduction of the Goods and Services Tax (GST) in 2000. The increase for the quarter was slightly higher than the quarterly movements for the September and June quarters last year (both 1.8 per cent).”

“The annual increase for the CPI is the highest since 1990. Annual inflation for goods such as new dwellings and automotive fuel steadied this quarter, however we saw an uptick in inflation for services such as holidays and restaurant meals,” Marquardt said.

Monthly CPI accelerated from 7.3% yoy to 8.4% yoy in December, well above expectation of 7.7% yoy.

Marquardt said, “The monthly indicator recorded the largest annual rise in the series in December. The most significant contributors in the 12 months to December were New dwellings, up 16.0 per cent, and Holiday travel and accommodation, up 29.3 per cent. Airfare and accommodation prices rose in response to strong demand over the Christmas holiday period.”

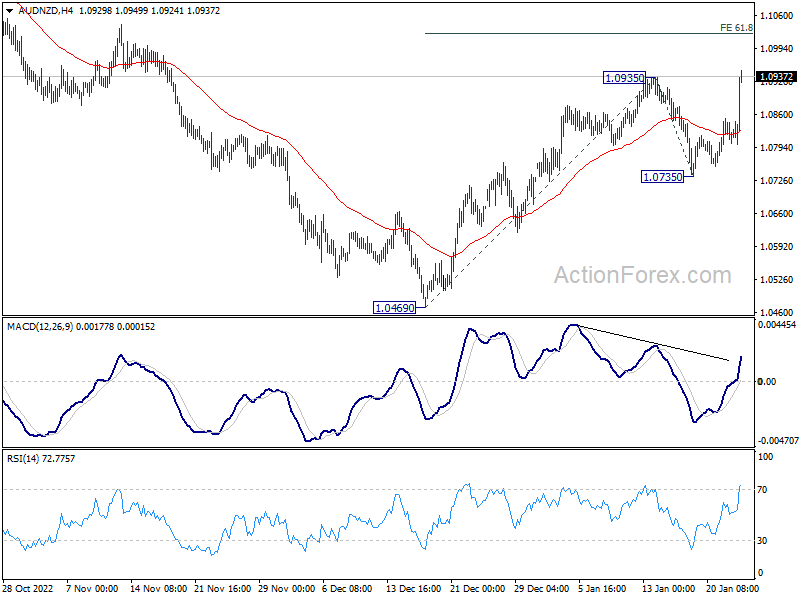

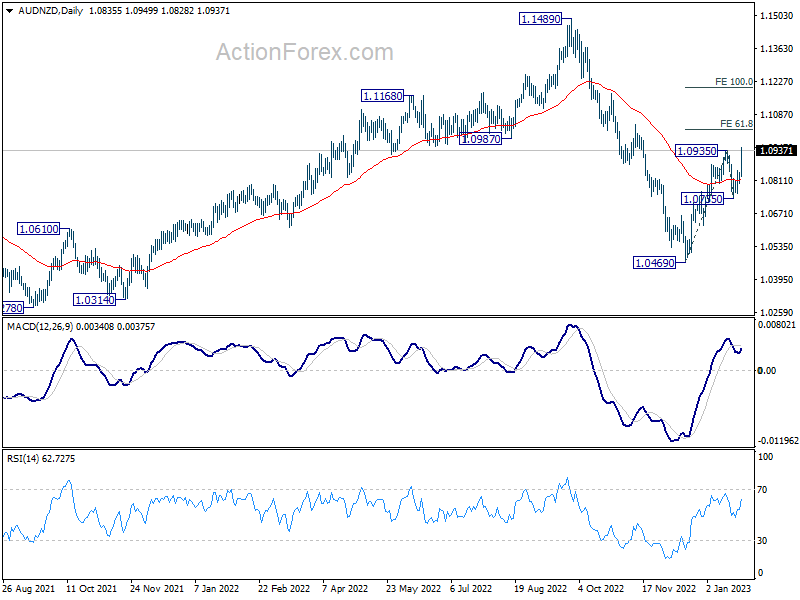

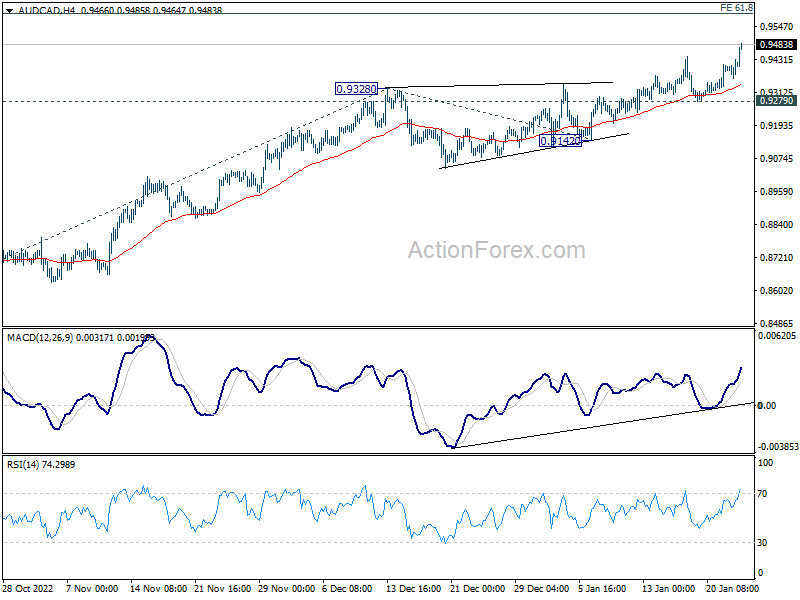

AUD/NZD and AUD/CAD extends up trend

Australian Dollar surges broadly after much stronger than expected CPI reading in December in particular dented any hope for an imminent RBA pause. Meanwhile, New Zealand Dollar is just mixed as CPI didn’t accelerate as RBNZ projected, raising hope of a lower terminal rate.

AUD/NZD breaks through 1.0935 resistance to resume the whole rally from 1.0469. The support from 55 day EMA is seen as a near term bullish favor. Further rise is now expected as long as 1.0735 support holds. Next target is 61.8% projection of 1.0469 to 1.0935 from 1.0735 at 1.1023. Firm break there would prompt upside acceleration to 100% projection at 1.1201 next.

AUD/CAD also breaks through 0.9442 temporary top to resume the rally from 0.8596. Near term outlook will stay bullish as long as 0.9279 support holds. Next target is 61.8% projection of 0.8596 to 0.9328 from 0.9142 at 0.9594. Sustained break there would also prompt upside acceleration to 100% projection at 0.9874 next.

ECB Simkus backs hikes of 50bps in the coming meetings

ECB Governing Council member Gediminas Simkus said yesterday, “core inflation remains strong and demonstrates that the fight against inflation is not over.”

“There’s a strong case for staying on the course that’s been set for the coming meetings of 50 basis-point increases. In my opinion, these 50 basis-point increases must be taken unequivocally,” he added.

“Pressures in wage growth are increasing — I expect wage increases to exceed historical averages in the euro area,” he said. “It’s something that’s happening and something we need to take into account because it affects core inflation.”

“It’s clear to me that the current economic environment requires us to deliver increases of 50 basis points in the coming meetings,” he said. “When we move to the more distant periods of the summer or next autumn, we need to wait and see.”

SNB Schlegel: Cannot rule out further interest increases

SNB Vice Chairman Martin Schlegel said yesterday, “we cannot rule out further interest increases at present,” even though inflation is forecast to fall back to 2.4% in 2023, and 1.8% in 2024.

“The maintenance of price stability has absolute priority for the SNB,” he added.

Meanwhile, Schlegel also expects a weak growth dynamic in the coming quarters.

BoC Previews: One more insurance hike before pausing

BoC is expected to deliver an “insurance” rate hike of 25bps today, to bring policy rate to 4.50%. After this eighth consecutive increase, the central bank is expected to pause the tightening cycle.

It’s already indicated in the December statement that the bank will be “considering whether the policy interest rate needs to rise further”. BoC should more explicitly indicate that it’s now the time to let pass rate hikes work through the economy.

The question would then shift to the time interest rate is going to stay at this level, but no answer is expected any time soon.

Here are some previews on BoC:

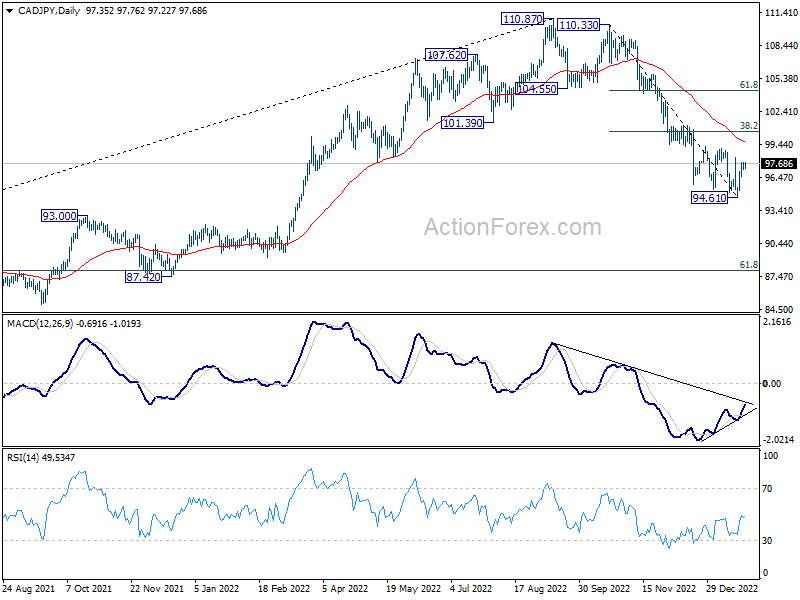

CAD/JPY has been losing downside momentum for some time, as seen in daily MACD and a bounce is overdue. Yet, even in case of a rebound, strong resistance could be seen between 55 day EMA (now at 99.65) and 38.2% retracement of 110.33 to 94.61 at 100.61 to cap upside. Until 100.61 is taken out decisively, any bounce is more of a short opportunity than a turnaround.

Elsewhere

UK PPI, Swiss Credit Suisse economic expectations and Germany Ifo business climate will also be featured today.

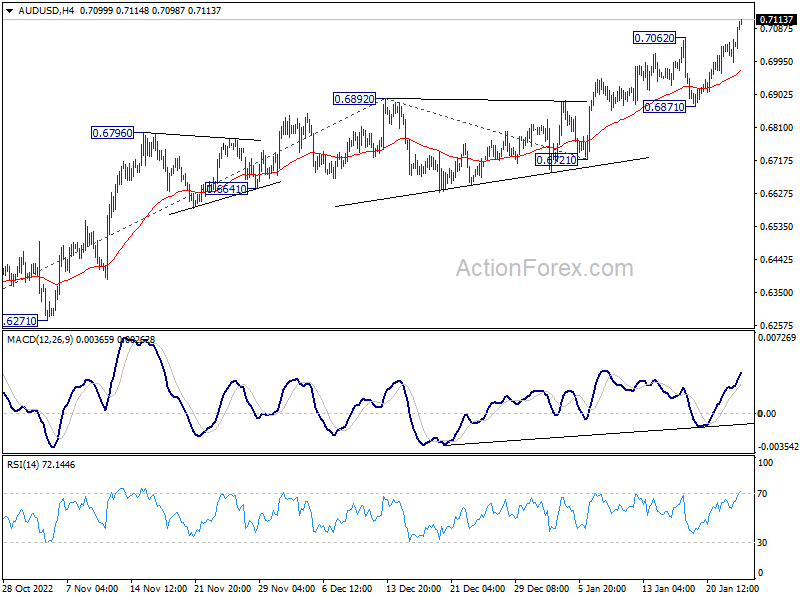

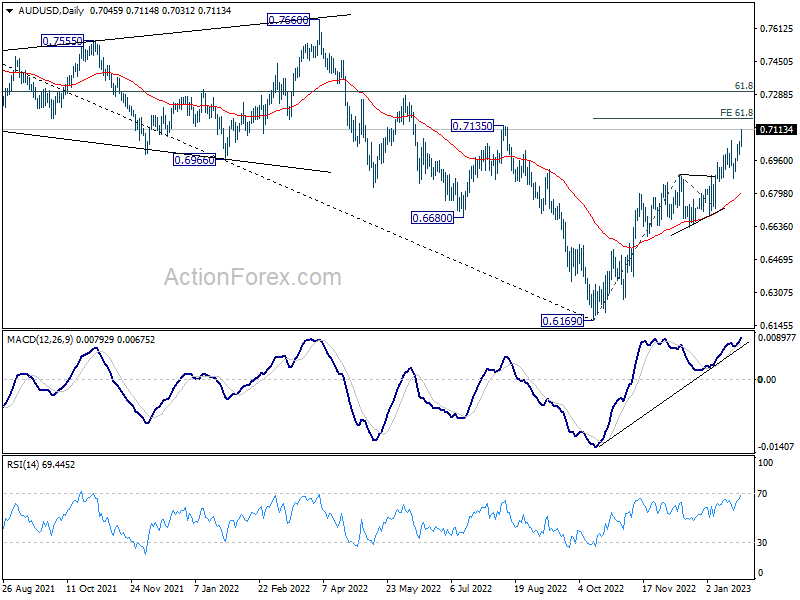

AUD/USD Daily Report

Daily Pivots: (S1) 0.7007; (P) 0.7032; (R1) 0.7071; More…

AUD/USD’s rally resumes by breaking through 0.7062 and intraday bias is back on the upside. Current rise from 0.6169 should target 61.8% projection of 0.6169 to 0.6892 from 0.6721 at 0.7168 next. Break there will target 0.7304 fibonacci level. On the downside, break of 0.6871 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, corrective decline from 0.8006 (2021 high) should have completed with three waves down to 0.6169 (2022 low). Further rally should be seen to 61.8% retracement of 0.8006 to 0.6169 at 0.7304. Sustained break there will pave the way to retest 0.8006. This will now remain the favored case as long as 0.6721 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 1.40% | 1.50% | 2.20% | |

| 21:45 | NZD | CPI Y/Y Q4 | 7.20% | 7.10% | 7.20% | |

| 23:30 | AUD | Westpac Leading Index M/M Dec | -0.10% | -0.10% | ||

| 00:30 | AUD | CPI Q/Q Q4 | 1.90% | 1.70% | 1.80% | |

| 00:30 | AUD | CPI Y/Y Q4 | 7.80% | 7.50% | 7.30% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | 1.70% | 1.60% | 1.80% | 1.90% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | 6.90% | 6.50% | 6.10% | |

| 00:30 | AUD | Monthly CPI Y/Y Dec | 8.40% | 7.70% | 7.30% | |

| 07:00 | GBP | PPI Input M/M Dec | 0.90% | 0.60% | ||

| 07:00 | GBP | PPI Input Y/Y Dec | 19.20% | 19.20% | ||

| 07:00 | GBP | PPI Output M/M Dec | 0.70% | 0.30% | ||

| 07:00 | GBP | PPI Output Y/Y Dec | 13.90% | 14.80% | ||

| 07:00 | GBP | PPI Core Output M/M Dec | 1.10% | 0.50% | ||

| 07:00 | GBP | PPI Core Output Y/Y Dec | 13.90% | 13.30% | ||

| 09:00 | CHF | Credit Suisse Economic Expectations Jan | -42.8 | |||

| 09:00 | EUR | Germany IFO Business Climate Jan | 90.5 | 88.6 | ||

| 09:00 | EUR | Germany IFO Current Assessment Jan | 95 | 94.4 | ||

| 09:00 | EUR | Germany IFO Expectations Jan | 85 | 83.2 | ||

| 15:00 | CAD | BoC Rate Decision | 4.50% | 4.25% | ||

| 15:30 | USD | Crude Oil Inventories | 1.2M | 8.4M | ||

| 16:00 | CAD | BoC Press Conference |