The markets become rather directionless again in Asian session. Yen is paring some gains as the boost from BoJ faded. Swiss Franc, Aussie and Kiwi are on the weaker side too. On the other hand, Canadian and US Dollar are the stronger ones for the day. Both are awaiting economic data release, including Canadian CPI and US consumer confidence. Meanwhile, Euro and Sterling are mixed.

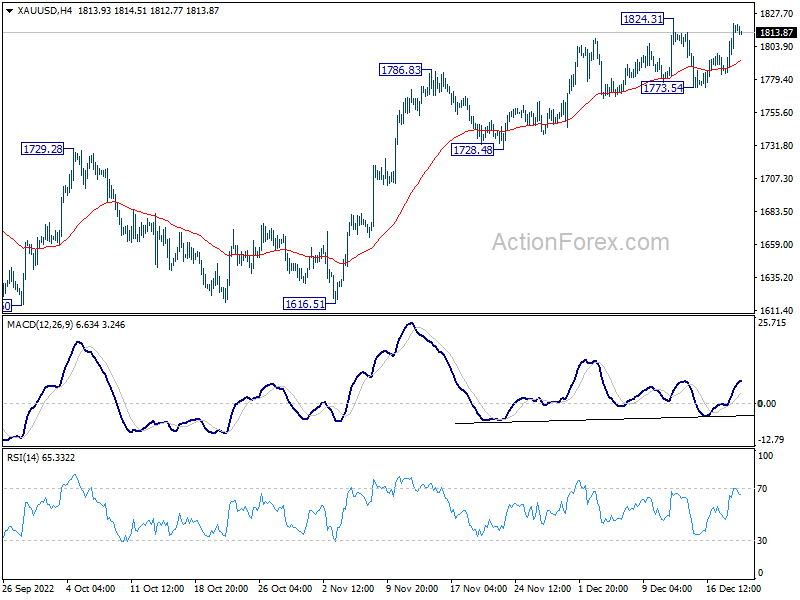

Technically, Gold rebounded strongly after retreating to 1773.54. Immediate focus is back on 1824.31 resistance. Firm break there will resume larger rise from 1616.51. On the downside, however, break of 1773.54 will bring deeper decline back to 1728.48 support, as a corrective move. The breakout in Gold could be an early indicate of the next move in Dollar, in particular in EUR/USD.

In Asia, Nikkei closed down -0.61%. Hong Kong HSI is up 0.13%. China Shanghai SSE is down -0.28%. Singapore Strait Times is up 0.06%. Japan 10-year yield is up 0.0686 at 0.486, getting closer to new cap at 0.50%. Overnight, DOW rose 0.28%. S&P 500 rose 0.10%. NASDAQ rose 0.01%. 10-year yield rose 0.103 to 3.684.

IMF: BoJ YCC adjustment a sensible step

Ranil Salgado, the IMF’s mission chief to Japan, said that “with uncertainty around the inflation outlook, the Bank of Japan’s adjustment of yield curve control settings is a sensible step including given concerns about bond market functioning.”

“Providing clearer communications on the conditions for adjusting the monetary policy framework would help anchor market expectations and strengthen the credibility of the Bank of Japan’s commitment to achieve its inflation target,” he said.

BoJ announced to raise the cap on 10-year JGB yield from 0.25% to 0.50% yesterday, to ” correct distortions in the yield curve”.

Australia leading index consistent with below trend growth well into 2023

Australia Westpac-MI leading index dropped from -0.84% to -0.92% in November. Growth rate was, thus, in negative territory for the fourth consecutive month. The data is consistent with below trend growth well into 2023. Drivers of weakness are the RBA interest rate and commodity prices.

Westpac expects another 25bps rate hike by RBA in February, “give the outlook for wages; inflation and economic growth”. It expects wages and inflation challenges to persist through early months of 2023, requiring “further increase of 25bps in both March and May.

Looking ahead

Germany Gfk consumer confidence and UK public sector net borrowing will be released in European session. Later in the day, Canada CPI and US consumer confidence will be the main features.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0582; (P) 1.0621; (R1) 1.0662; More…

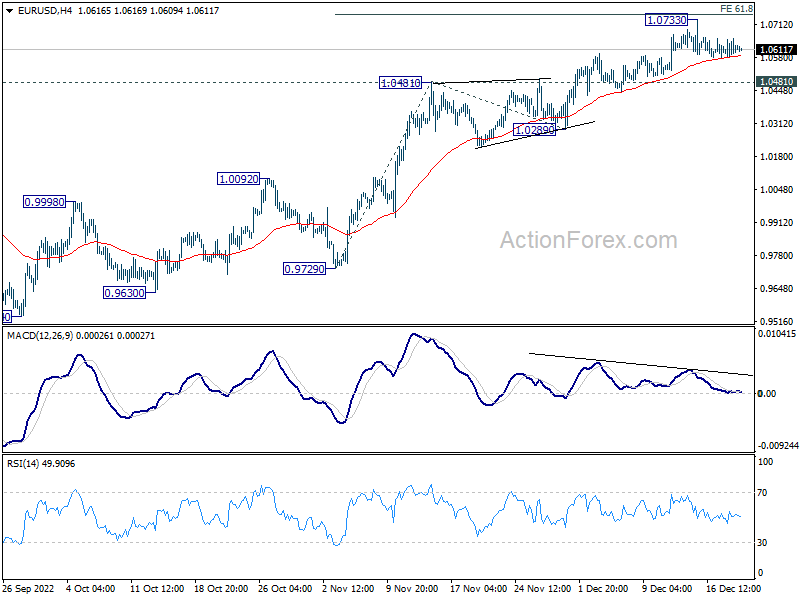

EUR/USD still bounded in sideway trading below 1.0733 and intraday bias remains neutral for the moment. Further rally is expected as long as 1.0481 resistance turned support holds. Firm break of 61.8% projection of 0.9729 to 1.0481 from 1.0289 at 1.0754 will pave the way to 100% projection at 1.1041. However, firm break of 1.0481 will confirm short term topping and bring deeper fall to 1.0289 support.

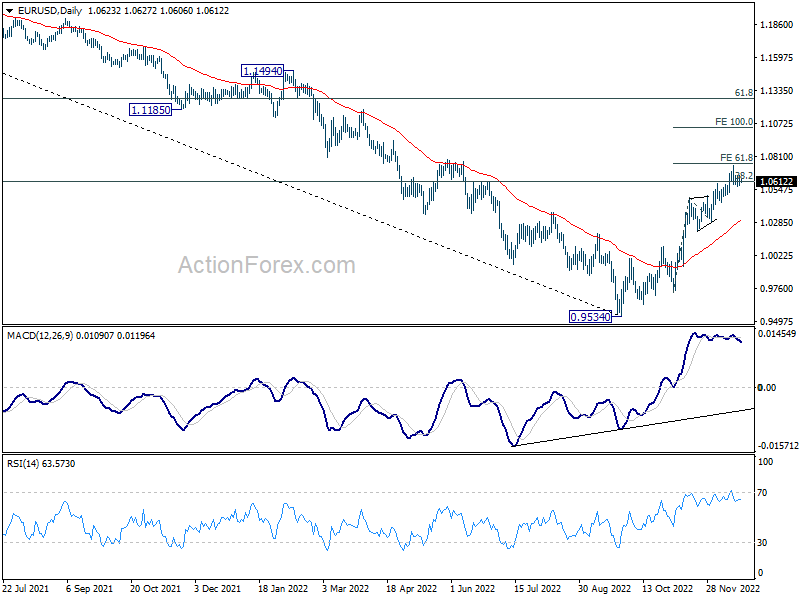

In the bigger picture, focus stays on 38.2% retracement of 1.2348 (2021 high) to 0.9534 at 1.0609. Rejection by 1.0609 will suggest that price actions from 0.9534 medium term bottom are developing into a corrective pattern. Thus, medium bearishness is retained for another fall through 0.9534 at a later stage. However, sustained break of 1.0609 will raise the chance of trend reversal and target 61.8% retracement at 1.1273.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Nov | -1863M | -2062M | -2129M | -2298M |

| 23:30 | AUD | Westpac Leading Index Nov | -0.10% | -0.10% | 0.00% | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Jan | -38 | -40.2 | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Nov | 10.3B | 12.7B | ||

| 13:30 | CAD | CPI M/M Nov | 0.40% | 0.70% | ||

| 13:30 | CAD | CPI Y/Y Nov | 7.40% | 6.90% | ||

| 13:30 | CAD | CPI Median Y/Y Nov | 4.90% | 4.80% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Nov | 5.30% | 5.30% | ||

| 13:30 | CAD | CPI Common Y/Y Nov | 6.10% | 6.20% | ||

| 13:30 | USD | Current Account (USD) Q3 | -222B | -251B | ||

| 15:00 | USD | Existing Home Sales Nov | 4.20M | 4.43M | ||

| 15:00 | USD | Consumer Confidence Dec | 101 | 100.2 | ||

| 15:30 | USD | Crude Oil Inventories | 2.5M | 10.2M |