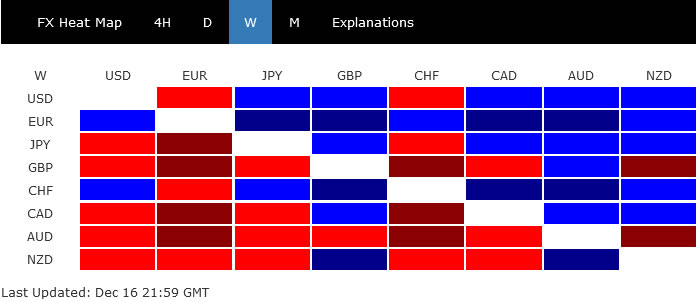

Risk sentiment took a U-turn last week after more hawkish than expected FOMC projections and, more important, ECB forward guidance. Euro ended as the biggest winner for the week, trained by Swiss Franc, and the Dollar. Australian Dollar was the worst performer, followed by Sterling, and then Kiwi. Canadian Dollar and Yen ended mixed.

The development could set up risk-off movements in the markets for the rest of the year, which could favor more upside in Dollar. The is also some downside risks in Aussie, depending on how situation in China unfolds. Euro’s strength was not totally convincing given the late pull back against Dollar and Yen. But the common currency looks more likely to outperform commodity currencies than not.

Sentiment U-turn on hawkish ECB and Fed

Last week’s central bank meetings were full of surprises. The biggest one came from ECB with President Christine Lagarde, in a rare fashion, indicating that there will be more 50bps hikes for a period of time. The judgement was probably based on expectation that recession in Eurozone would only be a shallow one. There are now expectations for at least two more 50bps hikes in February and March. Some economists raised their forecast of ECB terminal rate to 3.25-3.75% range, comparing to the current 2.50%.

Fed’s new economic projection was seen as more hawkish than expected, with median estimate of federal funds rate reading 5.1% in 2023, above 5% level. Indeed, 17 policy markets penciled in rate at 5.125% and above next year, with 7 expecting 5.375% and above. Comparing to the current 4.25-4.50%, there could be three to four 25bps hikes.

SNB didn’t rule out more rate hikes ahead. But with hawkish ECB, SNB will more likely follow than not, too keep exchange rate steady to counter inflation. BoE voting was some what dovish with two members voted for no change even though one voted for a 75bps hike.

The net result is an U-turn in market sentiment. DAX’s steep decline towards the end of the week confirmed short term topping at 14675.84. It’s now sitting close to support zone between 38.2% retracement of 11862.84 to 14675.84 at 13601.27, and 55 day EMA (now at 13828.58). Recovery from this support zone will keep the corrective pattern from 14675.84 as a ranging one. However, firm break of the zone will open up deeper decline back to 61.8% retracement at 12937.40, and possibly below.

In the US, NASDAQ’s decline raised the chance that consolidation from 10088.82 has completed at 11571.64, and the larger down trend from 16212.22 is ready to resume. Further decline is now in favor to retest 10088.82 low in the near term, or even further to double projection target 9660.62/9689.96 (61.8% projection of 13181.08 to 10082.82 from 11571.64 and 61.8% projection from 16212.22 to 10565.13 from 13181.08 at 9689.96). Stronger support is likely from there to complete the down trend. If that’s the case, then DOW’s pull back from 34595.51 should be contained well above 28600.94 low.

Dollar index continued to lose downside momentum, rebound overdue

Dollar index edged lower last week but continued to lose downside momentum. Euro’s strength is clearly limiting DXY’s recovery. Still, a rebound is overdue considering that it’s pressing 55 week EMA (now at 104.05). Break of 105.82 resistance should indicate short term bottoming and bring stronger rebound back to 55 day EMA (now at 107.43) and above. However, sustained trading below the 55 week EMA will open up deeper decline to 61.8% retracement of 89.20to 114.77 at 98.96.

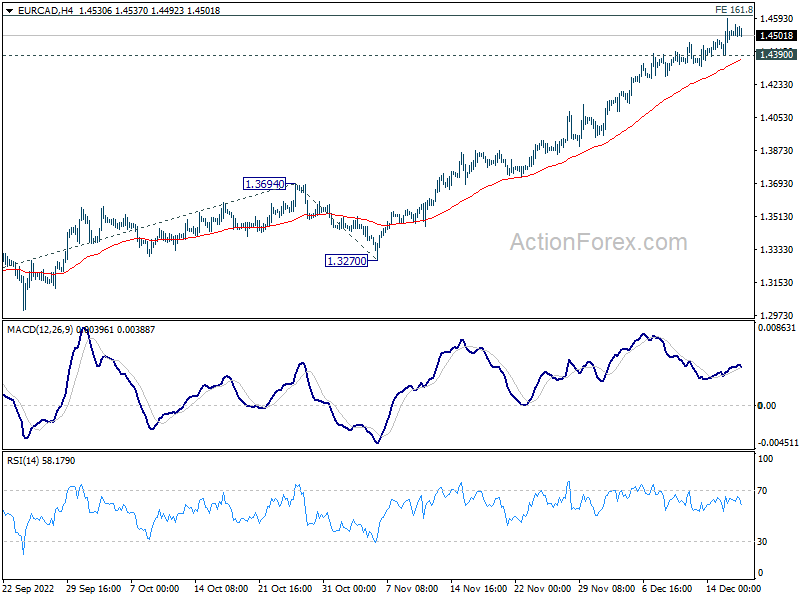

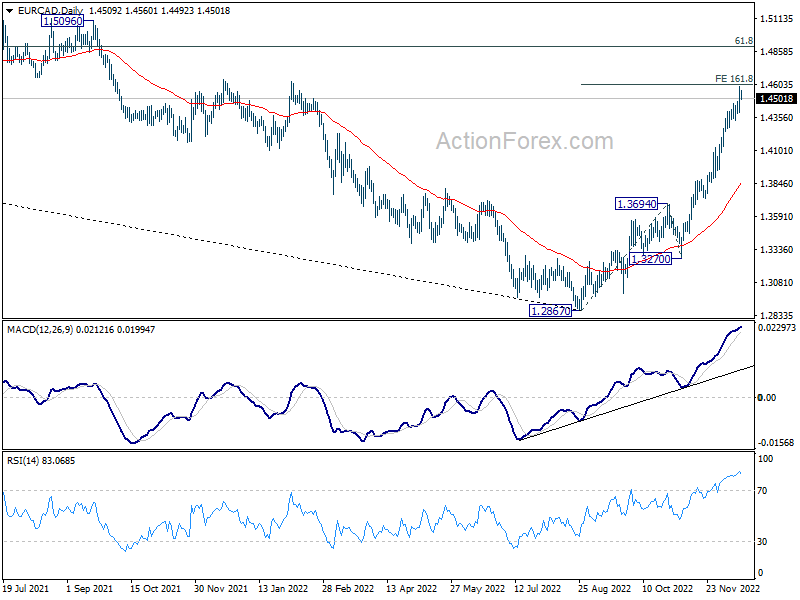

Will overbought condition cap EUR/CAD’s up trend?

Euro ended as the winner of the week. Its strength was rather clear against commodity currencies, but relatively less certain against others. EUR/CAD’s up trend from 1.2867 continued to as high as 1.4591 last week, just inch below 161.8% projection of 1.2867 to 1.3694 from 1.3270 at 1.4608. For now, further rise is expected as long as 1.4390 minor support holds. Sustained break of 1.4608 will put focus to key long term fibonacci level of 1.6151 to 1.2867 at 1.4897.

However, break of 1.4390 will indicate the short term topping, on overbought condition as seen in daily RSI. Some corrective trading should be seen with bias mildly on the downside, before the up trend resumes at a later stage. Such development, if happens, could be a sign of some weakness in Euro elsewhere, like against Dollar and Yen.

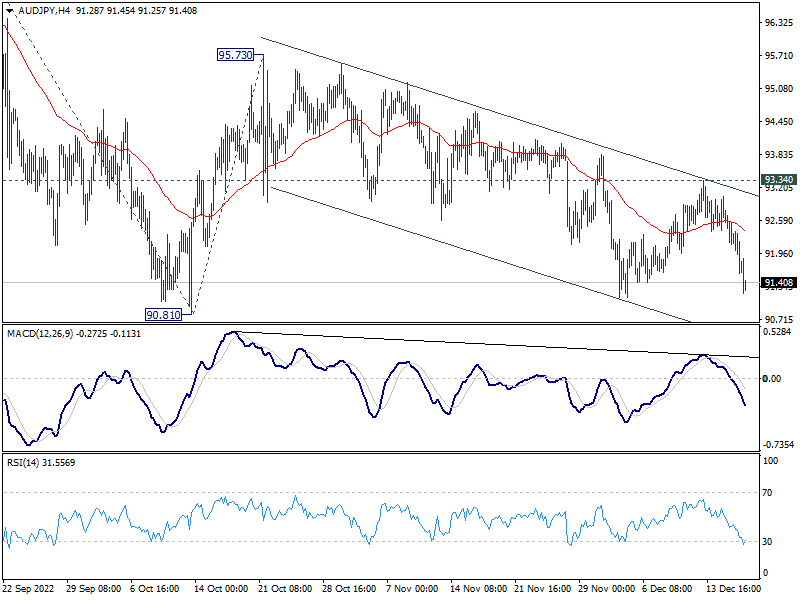

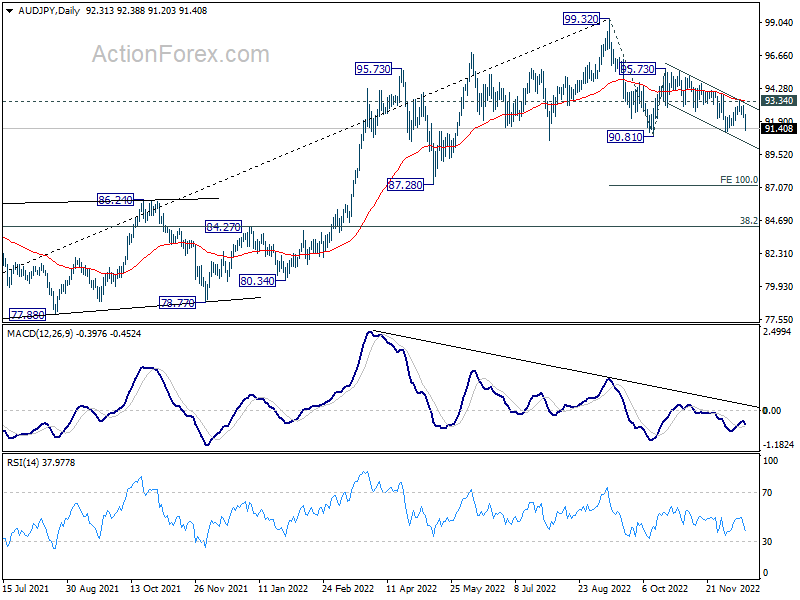

AUD/JPY finally ready for downside breakout?

Australian Dollar ended as the worst performer, on expectation of lower RBA terminal rate comparing with others, return of risk-off sentiment, and uncertainty over China’s infection situations.

AUD/JPY’s price actions from 95.73 has been rather indecisive. Yet, being capped below falling 55 day EMA was clearly a bearish sign. Further decline is expected as long as 93.94 resistance holds. Firm break of 90.81 support will resume the fall form 99.32 to 100% projection of 99.32 to 90.81 from 95.73 at 87.22, which is close to 87.28 structural support.

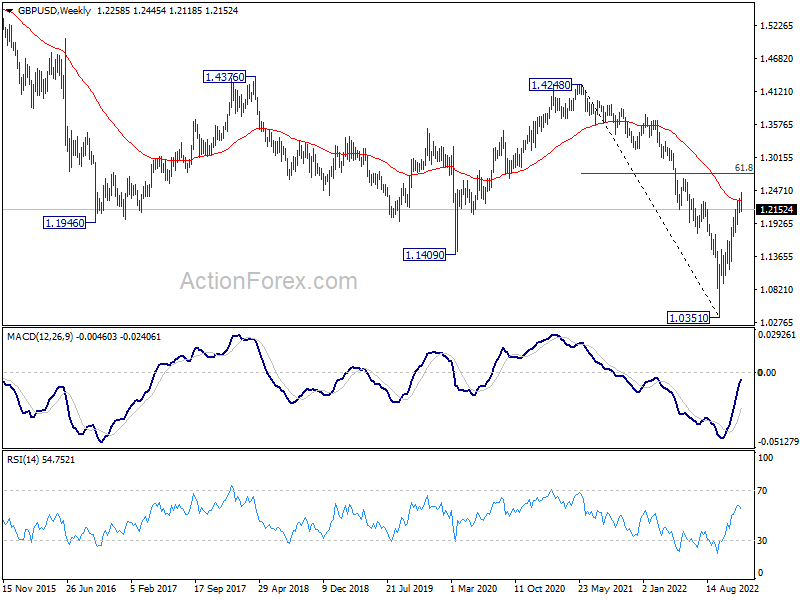

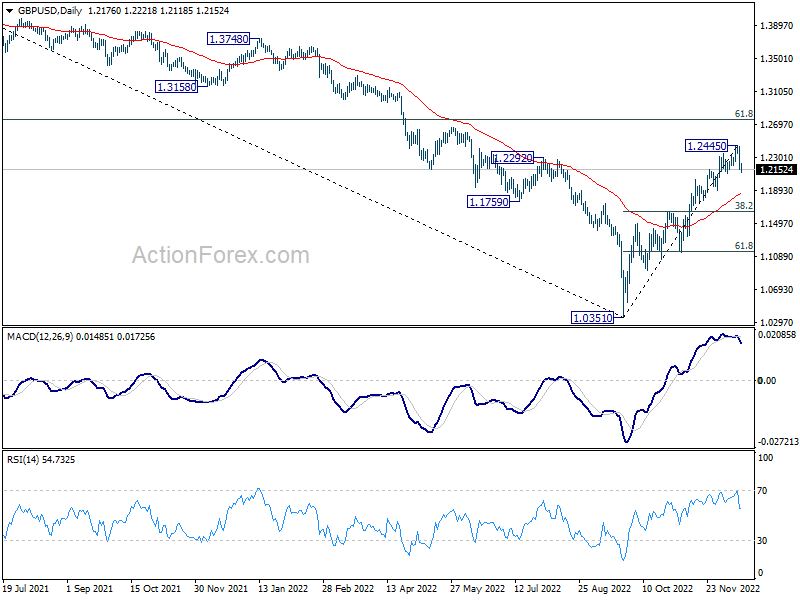

GBP/USD Weekly Outlook

GBP/USD rose further to 1.2445 last week but formed a short term top there and reversed. Initial bias is mildly on the downside this week for 55 day EMA (now at 1.1853). Firm break there will target 38.2% retracement of 1.0351 to 1.2445 at 1.1645. For now, risk will stay on the downside as long as 1.2445 resistance holds, in case of recovery.

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248. This will remain the favored case as long as 55 day EMA (now at 1.1853) holds.

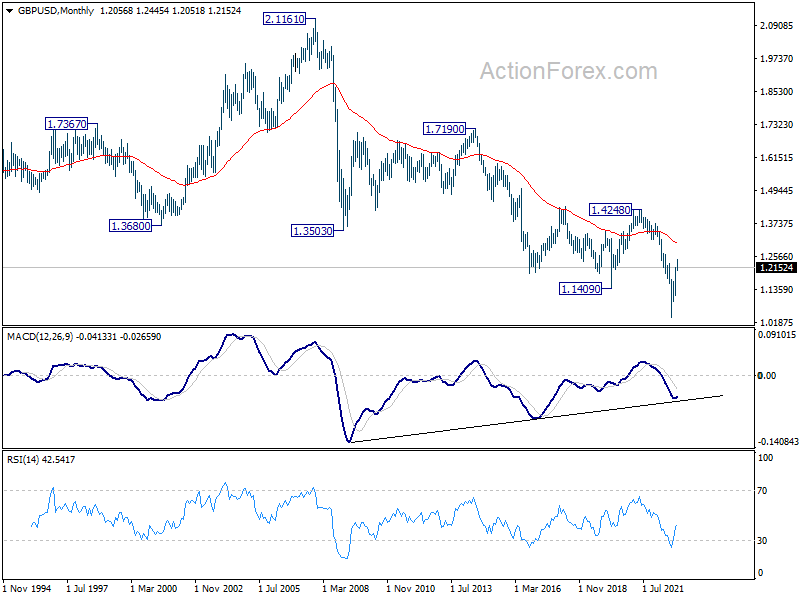

In the longer term picture, as long as 1.4248 resistance holds (2021 high), long term outlook will remain neutral at best. Down trend from 2.1161 (2007) could still resume for another low through 1.0351 at a later stage.