Yen is so far the clearly weaker one in otherwise ranging markets. Rebound in US stocks and treasury yield overnight was a factor in Yen’s selling. But after all, there is no follow through weakness for now. Traders are generally still cautious ahead of the four central bank meetings later in the week. Before that, US CPI release today might also trigger some interim volatility.

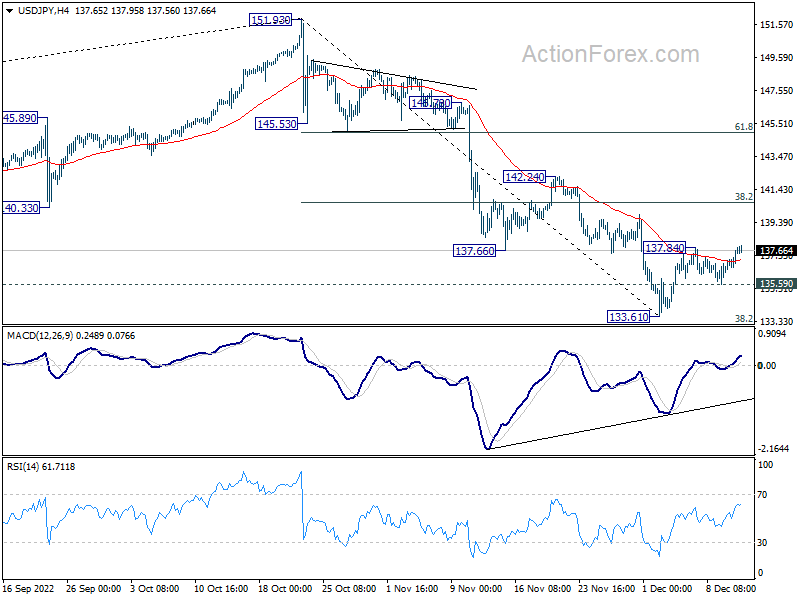

Technically, USD/JPY’s breach of 137.84 temporary top suggests that rebound from 133.61 is resuming. While upside momentum is weak, further rise will remain mildly in favor as long as 135.59 minor support holds. Next target is 38.2% retracement of 151.93 to 133.61 at 140.60, which is close to 55 day EMA (now at 140.80).

In Asia, at the time of writing, Nikkei is up 0.37%. Hong Kong HSI is up 0.36%. China Shanghai SSE is down -0.07%. Singapore Strait Times is up 0.90%. Japan 10-year JGB yield is down -0.0037 at 0.253. Overnight DOW rose 1.58%. S&P 500 rose 1.43%. NASDAQ rose 1.26%. 10-year yield rose 0.044 to 3.611.

BoC Macklem: Higher interest rates are working to rebalance the economy

BoC Governor Tiff Macklem said in a speech yesterday, “Higher interest rates are working to rebalance the economy. Domestic demand is slowing, and we expect growth in gross domestic product will be close to zero through to the middle of next year as the economy adjusts to higher interest rates. This will relieve domestic price pressures, and inflation will come down.”

He reiterated the position that the central bank will be considering “whether there is a need to increase the policy rate further”. He explained, “This means that decisions to raise the rate or to pause and assess the impact of past rate increases will depend on incoming data and our judgments about the outlook for inflation.”

Macklem also said BoC is “watching very closely to see how the economy is responding to higher interest rates”. It is looking at an job market data, how supply chains are resolving, how business are passing on costs, measures of core inflation, and inflation expectations.

Australia Westpac consumer sentiment bounced from near record low

Australia Westpac Consumer Sentiment Index bounced from near record low and rose 3% from 78.0 to 80.3 in December. But the level remains comparable to the lows see during the pandemic and the Global Financial Crisis.

Concerns over inflation remained dominant among respondents, followed by budget and taxation, economic conditions and interest rates.

Westpac expects RBA to continue to deliver on its “strong tightening bias” in February and hike by 25bps, and signal that there is still more work to be done.

Australia NAB business conditions hold up, but confidence turned negative

Australia NAB Business Confidence dropped from 0 to -4 in November, below zero for the first time since December 2021. Business Conditions dropped from 22 to 20, but remained elevated. Looking at some details, trading conditions dropped from 30 to 28. Profitability conditions dropped from 21 to 20. Employment conditions dropped from 14 to 13.

NAB Chief Economist Alan Oster. “There was a slight softening across a number of industries but the level of business conditions really still remains elevated across the board including in key consumer-facing sectors such as retail and recreation & personal services, and across the states.”

“Confidence is now negative, for the first time this year, despite the strength in conditions,” said Oster. “The gap between current business conditions and business confidence is now at a record level in the history of the survey – with the exception of March 2020 – pointing to heightened concerns about the resilience of the economy in the period ahead as inflation and higher rates begin to weigh on consumers.”

Looking ahead

UK employment data, Germany ZEW economic sentiment will be the main focus in European session. Swiss SECO will also publish economic forecasts. Later in the day, US CPI will take center stage.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 144.14; (P) 144.62; (R1) 145.52; More….

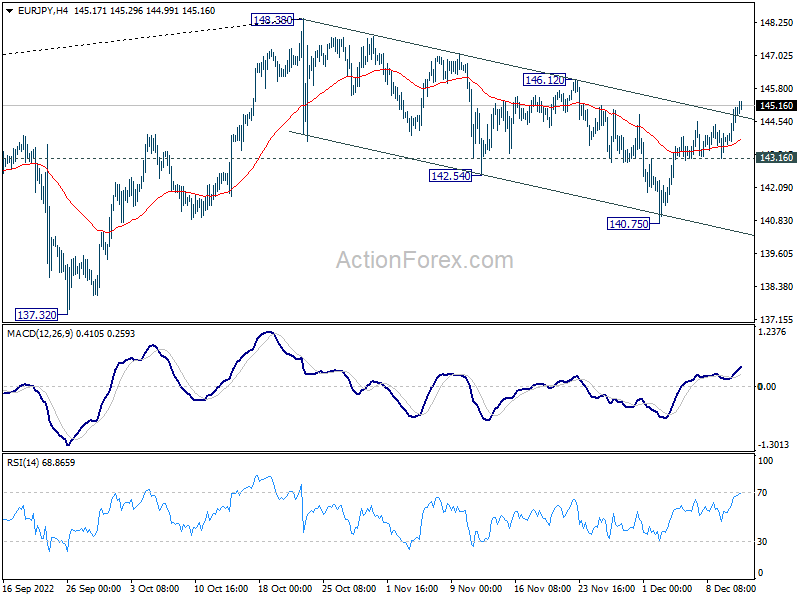

Intraday bias in EUR/JPY remains on the upside for the moment. Correction from 148.38 could have completed with three waves down to 140.75. Further rally would be seen to 146.12 resistance first. Firm break there will bring retest of 148.38 high. On the downside, however, break of 143.16 minor resistance will dampen this bullish case and turn intraday bias neutral again.

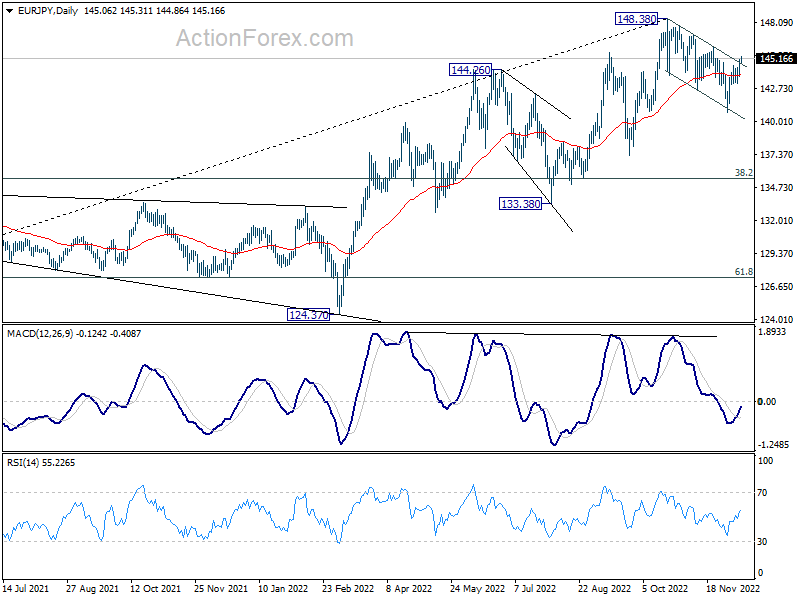

In the bigger picture, considering bearish divergence condition in weekly MACD, 148.38 could be a medium term top already. Fall from there is probably correcting whole up trend from 114.42 (2020 low). Deeper decline would be seen to 55 week EMA (now at 138.08), or further to 38.2% retracement of 114.42 to 148.38 at 135.40 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | 3.00% | -6.90% | ||

| 00:30 | AUD | NAB Business Confidence Nov | -4 | 0 | ||

| 00:30 | AUD | NAB Business Conditions Nov | 20 | 22 | ||

| 07:00 | GBP | Claimant Count Change Nov | 3.5K | 3.3K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | 3.70% | 3.60% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 5.70% | 5.70% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 6.20% | 6.00% | ||

| 07:00 | EUR | Germany CPI M/M Nov F | -0.50% | -0.50% | ||

| 07:00 | EUR | Germany CPI Y/Y Nov F | 10.00% | 10.00% | ||

| 08:00 | CHF | SECO Economic Forecasts | ||||

| 09:00 | EUR | Italy Industrial Output M/M Oct | -0.30% | -1.80% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | -26.3 | -36.7 | ||

| 10:00 | EUR | Germany ZEW Current Situation Dec | -64.5 | |||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | -25.3 | -38.7 | ||

| 11:00 | USD | NFIB Business Optimism Index Nov | 90.8 | 91.3 | ||

| 13:30 | USD | CPI M/M Nov | 0.50% | 0.40% | ||

| 13:30 | USD | CPI Y/Y Nov | 7.70% | 7.70% | ||

| 13:30 | USD | CPI Core M/M Nov | 0.60% | 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Nov | 6.40% | 6.30% |