Trading in the currency markets continues to be rather subdued. Canadian Dollar remains the weakest together Yen. The dovish rate hike by BoC overnight didn’t trigger more selloff, though. Yen is having little reaction to falling US and European benchmark yields. Dollar and Euro are the firmer ones but stay inside familiar range. Aussie and Kiwi are soft but, again, there is no follow through selling.

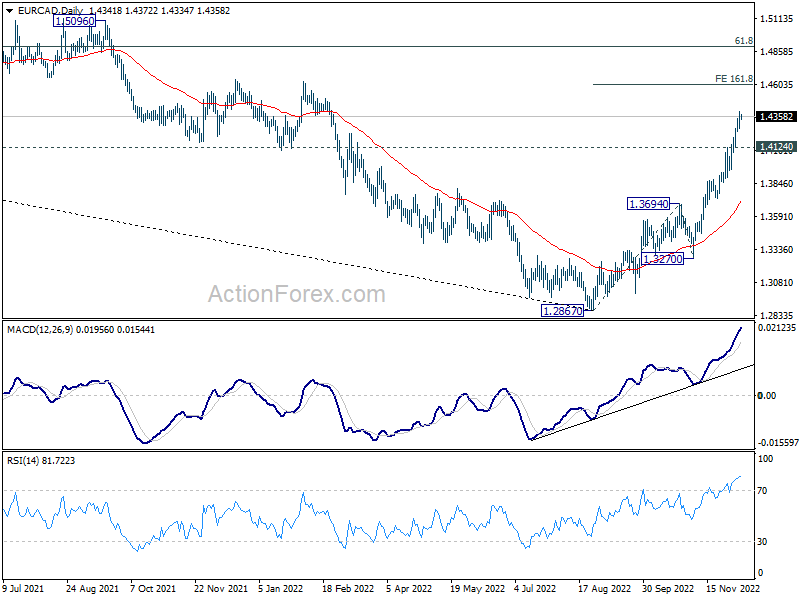

Technically, EUR/CAD’s rally from 1.2867 is making progress, a rare exception in the dull market. As long as 1.4124 support holds, further rise should be seen to 161.8% projection of 1.2867 to 1.3694 from 1.3270 at 1.4608. However, break of 1.4124 support should indicate short term topping and bring consolidations first.

In Asia, at the time of writing, Nikkei is down -0.53%. Hong Kong HSI is up 2.68%. China Shanghai SSE is down -0.10%. Singapore Strait Times is up 0.39%. Japan 10-year JGB yield is down -0.0026 at 0.252. Overnight, DOW closed flat, S&P 500 dropped -0.19%. NASDAQ dropped -0.51%. 10-year yield dropped -0.105 to 3.408.

Australia trade surplus little change at AUD 12.22B in Oct

Australia exports of goods and services dropped -0.9% mom to AUD 60.01B in October. Imports dropped -0.7% mom to AUD 47.85B. Trade surplus narrowed slightly from AUD 12.44B to AUD 12.22B, slightly above expectation of AUD 12.10B.

Looking at some details, the decline in exports was driven mainly by AUD -0.6B fall in gold while imports decline was driven by AUD -0.5B fall in energy. Fuel exports, dominated by LNG, rose AUD 0.3B to AUD 11.2B, and hit a new record high. Rural goods exports rose AUD 0.1B to AUD 7.2B, also a record high.

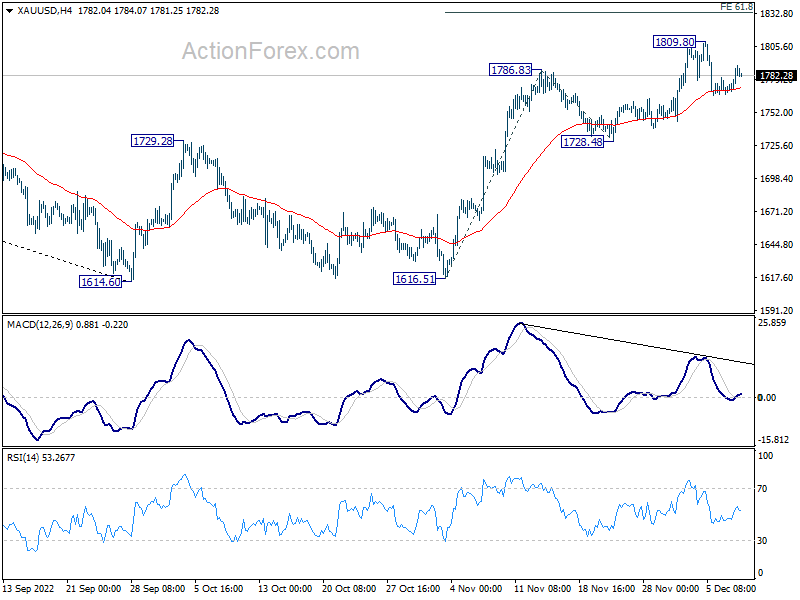

Gold fails 1800 handle for now

Gold’s rally halted after hitting 1809.80 earlier in the week, but failed to sustain above 1800 handle and turned into consolidations. Dollar’s recovery is capping Gold’s strength. Traders in the currency markets are generally cautious ahead of next week’s FOMC rate decision, and more importantly, the new dot plot.

Technically, Gold is feeling some support from 4 hour 55 EMA, which is a positive sign. Break of 1809.80 will resume the rise from 1616.51 to 61.8% projection of 1616.51 to 1786.83 from 1728.48 at 1833.73. However, sustained trading below 4 hour 55 EMA (now at 1772.44) will at least bring deeper fall back to 1728.48 support for a test.

Looking ahead

The economic calendar is rather light today with US jobless claims as the main feature.

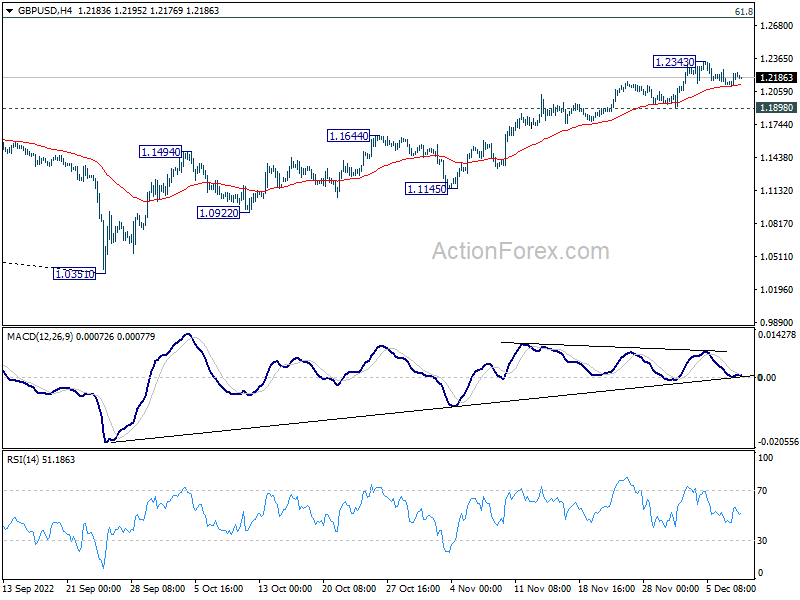

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2133; (P) 1.2184; (R1) 1.2261; More…

GBP/USD is staying in consolidation from 1.2343 and intraday bias remains neutral for the moment. Further rise remains mildly in favor as long as 1.1898 support holds. On the upside, break of 1.2343 will resume the rally from 1.0351 and target 1.2759 medium term fibonacci level next. However, firm break of 1.1898 support will confirm short term topping and turn bias back to the downside.

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q3 | -0.20% | -0.30% | -0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | -0.30% | -0.50% | -0.50% | |

| 23:50 | JPY | Bank Lending Y/Y Nov F | 2.70% | 2.50% | 2.70% | 2.60% |

| 23:50 | JPY | Current Account (JPY) Oct | -0.61T | 0.35T | 0.67T | |

| 00:01 | GBP | RICS Housing Price Balance Nov | -25% | -2% | ||

| 00:30 | AUD | Trade Balance (AUD) Oct | 12.22B | 12.10B | 12.44B | |

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 48.1 | 49.3 | 49.9 | |

| 13:30 | USD | Initial Jobless Claims (Dec 2) | 245K | 225K | ||

| 15:30 | USD | Natural Gas Storage | -38B | -81B |