The forex markets are rather steady in Asia today. While stocks in China and Hong Kong extending last week’s strong rebound, Aussie and Kiwi are not following for now. Some traders are on guard to rumors of reopening in China, in particular with a district in Guangzhou still extending tough lockdown. The economic calendar is relative light this week. Main focus will be on consumer inflation data in the US.

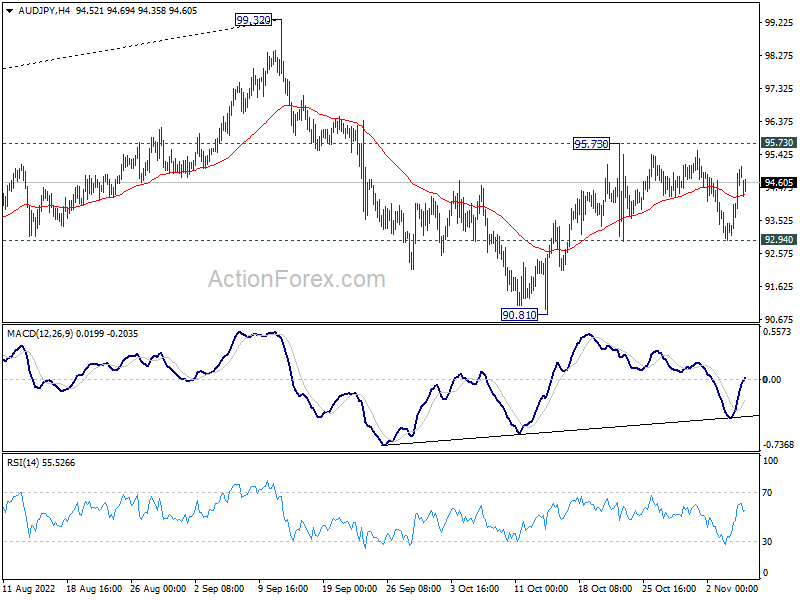

Technically, it’s possible that AUD/JPY’s consolidation from 95.73 has completed with three waves to 92.94. That is, rebound from 90.81 might be ready to resume. Break of 95.73 resistance will confirm this case and target 99.32 high. For now, a break of 99.32 is not envisaged given the threat of intervention in USD/JPY. But that could depend on the momentum in AUD/USD upon breaking through 0.6521 resistance to complete a head and should bottom pattern.

In Asia, at the time of writing, Nikkei is up 1.30%. Hong Kong HSI is up 3.42%. China Shanghai SSE is up 0.46%. Singapore Strait Times is up 0.21%. Japan 10-year JGB yield is down -0.0074 at 0.250.

China exports dropped -0.3% yoy in Oct, imports down -0.7% yoy

In USD term, China’s exports dropped -0.3% yoy to USD 298.37B in October, well below expectation of 4.3% yoy. That’s the worst performance since May 2020.

Imports dropped -0.7% yoy to USD 213.22B, below expectation of 0.1% yoy. That’s the the worst since August 2020.

The simultaneous contraction in both exports and imports was the first since May 2020.

Trade surplus widened slightly from USD 84.74B to USD 85.15B, short of expectation of USD 95.95.

US CPI to highlight a “relatively” light week

US CPI highlights a “relatively” light week. Fed Chair Jerome Powell indicated clearly that tightening pace could slow as soon as in December, but the terminal rate could be higher than earlier expected. Chicago Fed President Charles Evans later said the projection of peak rate might be revised “slightly higher” in the upcoming forecasts. But after all, the path will remain heavily data dependent, especially on whether inflation shows more signs of cooling.

Other data to be watched closely include US U of Michigan consumer sentiment; Eurozone Sentix investor confidence, UK GDP. In term of central bank activities, BoJ will publish summary of opinions. ECB will publish monthly bulletin.

Here are some highlights for the week:

- Monday: China trade balance; Swiss unemployment rate, foreign currency reserves; Germany industrial production; Eurozone Sentix investor confidence.

- Tuesday: Australia AiG services, Westpac consumer sentiment, NAB business confidence; New Zealand inflation expectations; Japan average cash earnings, household spending, leading indicators, BoJ summary of opinions; France trade balance; Eurozone retail sales.

- Wednesday: Japan current account, bank lending; China CPI, PPI; US wholesale inventories.

- Thursday: Australia MI inflation expectations, UK RICS house price balance; ECB economic bulletin; US CPI, jobless claims.

- Friday: New Zealand BusinessNZ manufacturing index; Japan PPI; Germany CPI final; UK GDP, production, trade balance, NIESR GDP estimate; US U of Michigan consumer sentiment.

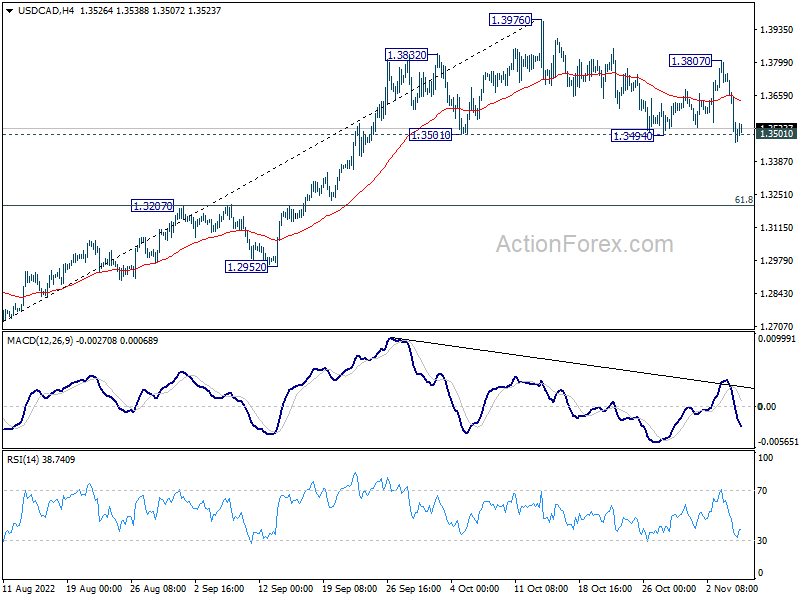

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3383; (P) 1.3567; (R1) 1.3808; More….

Intraday bias in USD/CAD stays on the downside at this point. A head and should top pattern (1.3832; h: 1.3976; rs: 1.3807) should be formed already. Sustained trading below 1.3494 will confirm, and bring deeper fall to .3207 cluster support (61.8% retracement of 1.2726 to 1.3976 at 1.3204. Strong support should be seen there to bring rebound. But for now, risk will stay on the downside as long as 1.3807 resistance holds, in case of recovery.

In the bigger picture, up trend from 1.2005 (2021 low) is still in progress. Based on current impulsive momentum, it could be resuming long term up trend from 0.9056 (2007 low). Whether it is or it isn’t, retest of 1.4689 (2016 high) should be seen next. This will now remain the favored case as long as 1.3222 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | CNY | Trade Balance (USD) Oct | 85.2B | 96.0B | 84.7B | |

| 02:00 | CNY | Trade Balance (CNY) Oct | 85.2B | 702B | 574B | |

| 06:00 | JPY | Machine Tool Orders Y/Y Oct | 4.30% | |||

| 07:00 | EUR | Germany Industrial Production M/M Sep | -0.20% | -0.80% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | 807B | |||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -35 | -38.3 |