Dollar rally continues today and it’s set to end the week on a high note. Risk aversion and rising benchmark yield are both helping the greenback. Swiss Franc is also strengthening a lot. Selling focuses are mainly concentrated on Sterling, Euro, and Yen, even though commodity currencies are also soft.

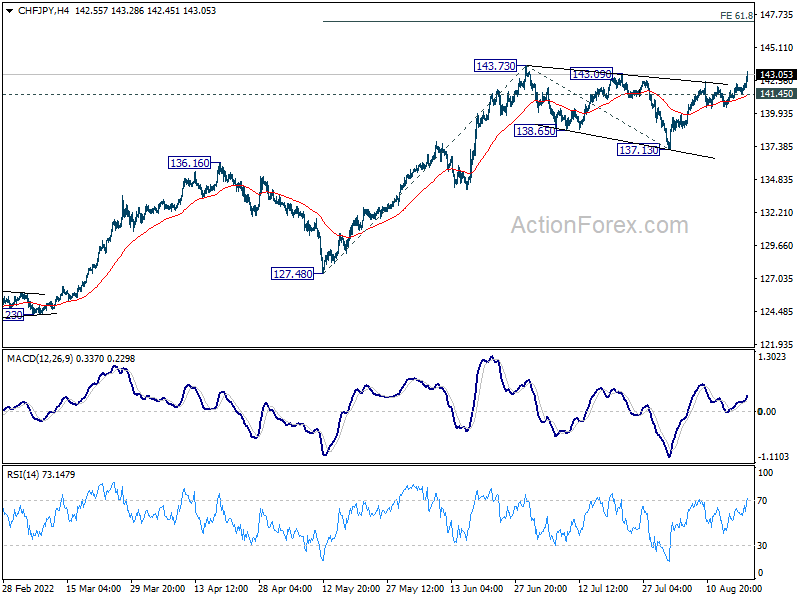

Technically, the rally in CHF/JPY is rather impressive, and it affirms the case that correction from 143.73 has completed with three waves down to 137.13. That is, larger up trend is ready to resume. For now, further rally is expected as long as 141.45 support holds. Firm break of 143.73 (probably next week) will pave the way to 61.8% projection of 127.48 to 143.73 from 137.13 at 147.17.

In Europe, at the time of writing, FTSE is up 0.17%. DAX is down -0.66%. CAC is down -0.55%. Germany 10-year yield is up 0.1122 at 1.214. Earlier in Asia, Nikkei dropped -0.04%. Hong Kong HSI rose 0.05%. China Shanghai SSE dropped -0.59%. Singapore Strait Times dropped -0.82%. Japan 10-year JGB yield rose 0.0011 to 0.201.

Canada retail sales rose 1.1% mom in Jun, core sales up 0.2% mom

Canada retail sales rose 1.1% mom to CAD 63.1B in June, above expectation of 0.4% mom. That’s also the sixth consecutive monthly increase. Sales were up in 8 of 11 subsectors, representing 76.8% of retail trade. Core retail sales, excluding gasoline stations and motor vehicle and parts, rose 0.2% mom.

In the advance estimate, retail sales dropped -2.0% mom in July.

UK retail sales volume rose 0.3% mom in Jul

In volume term, UK retail sales rose 0.3% mom in July, better than expectation of -0.2% mom. Ex-auto sales rose 0.4% mom. Comparing to a year ago, retail sales dropped -3.4% yoy while ex-auto sales dropped -3.0% yoy.

In value term, retail sales rose 1.3% mom, 7.8% yoy. Ex-auto sales rose 1.4% mom, 5.7% yoy.

From Germany, PPI rose 5.3% mom, 37.2% yoy in July, above expectation of 0.5% mom, 31.5% yoy.

UK Gfk consumer confidence drooped to -44, another record low

UK Gfk consumer confidence dropped from -41 to -44 in August, hitting another record low. Personal financial situation over the next 12 months dropped from -26 to -31. General economic situation over the next 12 months dropped from -57 to -60, setting a new record low.

Joe Staton, Client Strategy Director, GfK says: “The Overall Index Score dropped three points in August to -44, the lowest since records began in 1974. All measures fell, reflecting acute concerns as the cost-of-living soars. A sense of exasperation about the UK’s economy is the biggest driver of these findings.”

Japan CPI core rose to 2.4% yoy, highest since 2014

Japan headline CPI rose from 2.4% yoy to 2.6% yoy in July, above expectation of 2.2% yoy. CPI core (all items ex-fresh food) rose from 2.2% yoy to 2.4% yoy, matched expectations. CPI core-core (all items ex-food, energy) rose from 1.0% yoy to 1.2% yoy, above expectations of 0.6% yoy.

Core inflation has now exceeded BoJ’s 2% target for four straight months, and hit the highest level since December 2014. The core-core reading was also the fastest since December 2015, while the headline reading was the strongest since 2008.

Both Prime Minister Fumio Kishida and BoJ Governor Haruhiko Kuroda have called for robust wage gains to ensure that inflation is sustainable. But the markets are expecting some pressure on the BoJ for acting on monetary policy if CPI hits 3%.

New Zealand goods exports rose 16% yoy in Jul, imports rose 26% yoy

New Zealand goods exports rose 16% yoy to NZD 6.7B in July. Goods imports rose 26% yoy to NZD 7.8B. Trade deficit came in at NZD -1.1B, comparing expectation of NZD 105m surplus.

China led the monthly rise in exports, up 13%. Exports to Australia was down -1.1%, USA up 5.8%, EU up 7.5%, Japan up 18%. Imports from China was up 19%, EU up 3.0%, Australia up 16%, USA up 34%, and Japan up 54%.

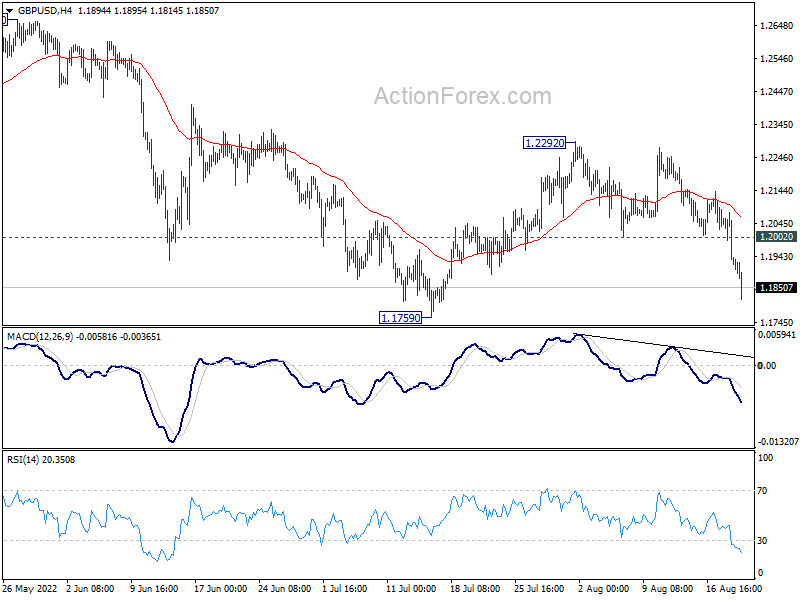

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1876; (P) 1.1978; (R1) 1.2033; More…

GBP/USD’s fall accelerates to as low as 1.1814 so far and intraday bias stays on the downside for retesting 1.1759 support. Firm break there will resume larger down trend Next target is 1.1409 low. On the upside, above 1.2002 support turned resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.2292 resistance holds.

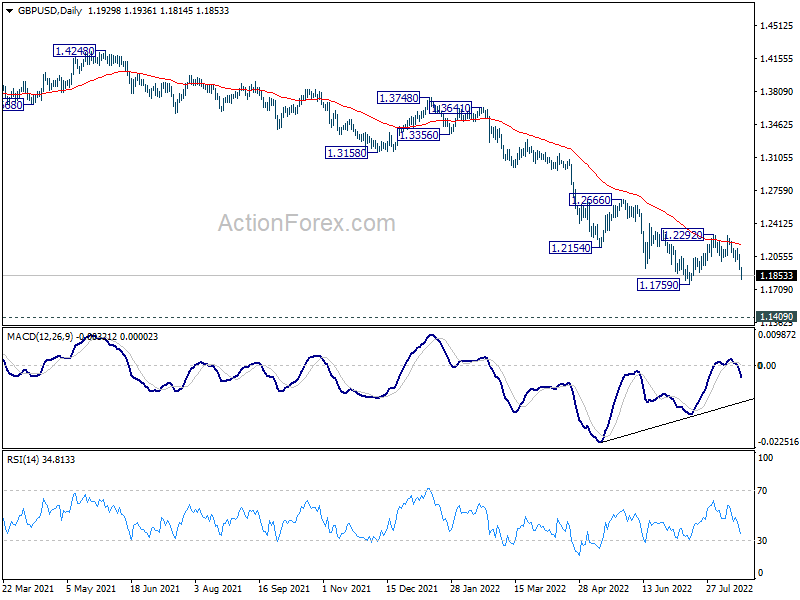

In the bigger picture, fall from 1.4248 (2018 high) could be a leg inside the pattern from 1.1409 (2020 low), or resuming the longer term down trend. Deeper decline is expected as long as 1.2666 resistance holds. Next target is 1.1409 low. However, firm break of 1.2666 will bring stronger rise back to 55 week EMA (now at 1.2897).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jul | -1092M | 105M | -701M | -1102M |

| 23:01 | GBP | GfK Consumer Confidence Aug | -44 | -42 | -41 | |

| 23:30 | JPY | National CPI Core Y/Y Jul | 2.40% | 2.40% | 2.20% | |

| 06:00 | EUR | Germany PPI M/M Jul | 5.30% | 0.50% | 0.60% | |

| 06:00 | EUR | Germany PPI Y/Y Jul | 37.20% | 31.50% | 32.70% | |

| 06:00 | GBP | Retail Sales M/M Jul | 0.30% | -0.20% | -0.10% | -0.20% |

| 06:00 | GBP | Retail Sales Y/Y Jul | -3.40% | -3.30% | -5.80% | -6.10% |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Jul | 0.40% | -0.20% | 0.40% | 0.20% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Jul | -3.00% | -2.80% | -5.90% | -6.20% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jul | 4.2B | 25.3B | 22.1B | 20.1B |

| 08:00 | EUR | Eurozone Current Account(EUR) Jun | 4.2B | -3.3B | -4.5B | -6.9B |

| 12:30 | CAD | Retail Sales M/M Jun | 1.10% | 0.40% | 2.20% | 2.30% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | 0.80% | 0.90% | 1.90% |