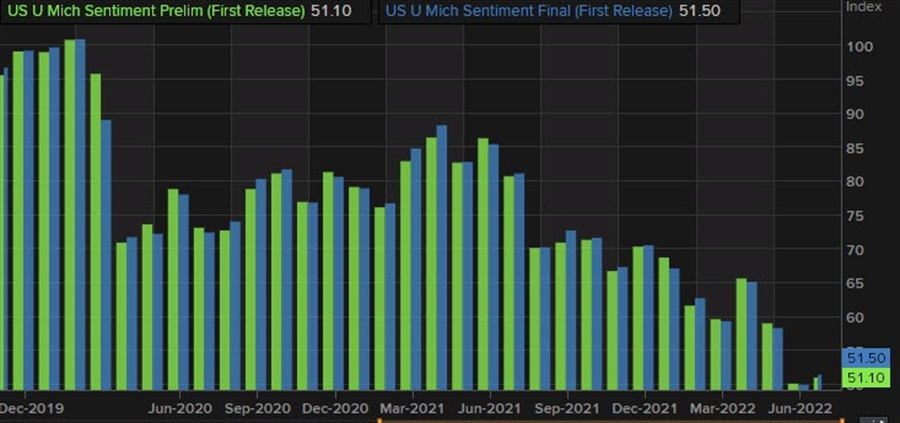

The University of Michigan sentiment data is out (final) for July:

- preliminary report

- consumer sentiment 51.5 vs. 51.1 estimate and 50.0 preliminary

- current conditions 58.1 vs. preliminary 53.8

- expectations 47.3 vs. preliminary 47.5

- one year inflation 5.2% vs. preliminary 5.3%. Last month 5.2%

- 5 year inflation 2.9% vs. preliminary 3.1%. Last month 2.8%

The University of Michigan final sentiment came in a little bit stronger than estimate and higher than the preliminary. However, the data still remains near historic low levels.

Current conditions were also higher and above last month 57.1. The expectations Index however remained near preliminary and last month levels.

Inflation remains elevated but a little lower than the preliminary 5.3% for the one year. The 5 year inflation expectations came in at 2.9% which was lower than the preliminary estimate of 3.1%

Joanne Hsu from the survey committee commented:

“The final July reading showed little change in consumer sentiment from its historic low in June. The one-year economic outlook fell to its lowest reading since 2009. At the same time, concerns over global factors have eased somewhat. This easing provided some limited support to buying conditions for durables, which remained near the all-time low reached last month, as well as a modest retreat in long run inflation expectations. However, inflation continued to dominate consumers’ attention, and labor market expectations continued to soften. This month’s Sentiment Index was the second lowest reading on record, and the Q2 slowdown in personal consumption expenditures was no surprise. The final July reading of the median expected year-ahead inflation rate was 5.2%, little changed from mid-month or the preceding two months. Long run expectations came in at 2.9%, remaining within the 2.9-3.1% range seen in the past 11 months.”

US stocks are trading near their highs for the day. The data is still sufficiently bad to be good for the Fed rate path outlook, and was also better than expectations (although still at historically record low levels). Bad is good in the stocks at least for now:

- Dow industrial average is up 127 points or 0.39% at 32652

- S&P index is up 37.36 points or 0.91% at 4109.13

- NASDAQ index is up 150 points or 1.23% 12312.94

- Russell 2000 is still modestly lower at -0.25 points or -0.01% at 1872.77