Euro rises broadly after ECB raising interest rate by 50bps, and front-loads the exit from negative deposit rate. The central bank also maintains tightening bias. Swiss Franc is taken up by Euro too. Meanwhile, New Zealand Dollar is the worst performing one for today, together with Canadian and Yen. Dollar is mixed for now, and would need more guidance from overall risk sentiments, or even FOMC rate decision next week.

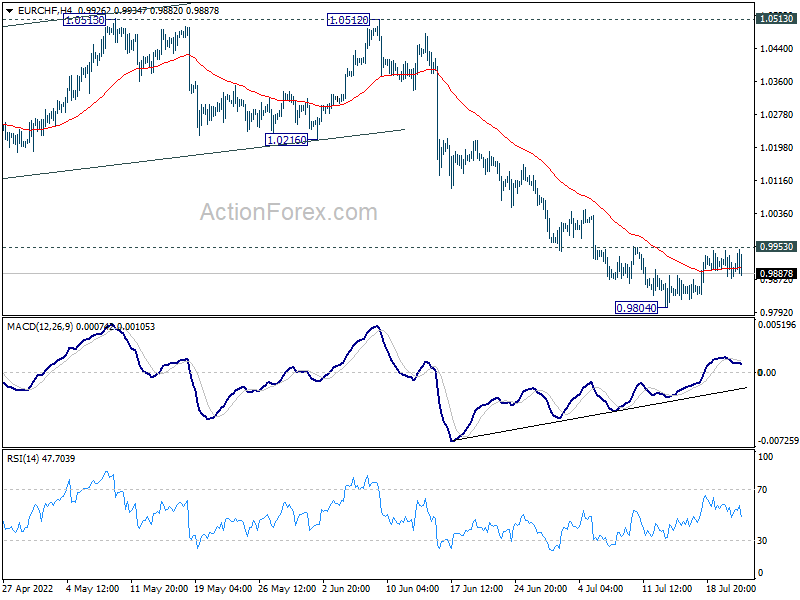

Technically, the sluggishness in EUR/CHF is putting some doubts over underlying strength in Euro. Firm break of 0.9953 minor resistance will confirm short term bottoming at 0.9083 and target 55 day EMA (now at 1.0108). However, rejection by 0.9953 will maintain near term bearishness. Break of 0.9804 will resume larger up trend. The next move in EUR/CHF is most important in confirming Euro’s direction.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is down -0.34%. CAC is up 0.54%. Germany 10-year yield is up 0.019 at 1.278. Earlier in Asia, Nikkei rose 0.44%. Hong Kong HSI dropped -1.51%. China Shanghai SSE dropped -0.99%. Singapore Strait Times dropped -0.57%. Japan 10-year JGB yield dropped -0.0036 to 0.241.

ECB hikes 50bps, frontloading exit from negative deposit rate

ECB announced to raise the three key interest rates by 50bps today. The main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be increased to 0.50%, 0.75% and 0.00% respectively, with effect from 27 July 2022.

The “larger first step” in policy normalization was based on the “updated assessment of inflation risks and the reinforced support provided by the TPI for the effective transmission of monetary policy.” The “frontloading” of exit from negative deposit rate ” allows the Governing Council to make a transition to a meeting-by-meeting approach to interest rate decisions.” Future policy path will continue to be “data-dependent”.

Also, the Governing Council approved the Transmission Protection Instrument (TPI), to “ensure that the monetary policy stance is transmitted smoothly across all euro area countries”.

At the post meeting press conference, President Christine Lagarde said that inflation continues to be “undesirably high” and is expected to remain above target for some time. While latest data indicate a slowdown in growth, this slowdown is “being cushioned by a number of supportive factors”.

“At our upcoming meetings, further normalization of interest rates will be appropriate,” she said. “Our future policy rate path will continue to be data-dependent and will help us deliver on our two per cent inflation target over the medium term.”

US initial jobless claims rose to 251k, continuing claims rose to 1.384m

US initial jobless claims rose 7k to 251k in the week ending July 16, above expectation of 240k. Four-week moving average of initial claims rose 4.5k to 240.5k.

Continuing claims rose 51k to 1384k in the week ending July 9. Four-week moving average of continuing claims rose 13k to 1353k.

BoJ stands part, downgrades 2022 growth forecasts, upgrades inflation

BoJ left monetary policy unchanged today as widely expected. Under the yield curve control frame work, short-term policy rate is held at -0.10%. BoJ will also will continue to purchase JGBs, without setting upper limit, to keep 10-year yield at around 0%. It will continue to offer to purchase 10-year JGBs at 0.25% yield every business day through fixed rate operations. Goushi Kataoka dissented again, pushing for further strengthening monetary easing.

In the new economic projections, BoJ downgraded fiscal 2022 GDP forecasts, but upgraded both fiscal 2023 and 2024. CPI forecasts was upgraded across the horizon. Here are the new projections.

- Fiscal 2022 GDP growth at 2.4% (downgraded from April’s 2.9%).

- Fiscal 2023 GDP growth at 2.0% (up from 1.9%).

- Fiscal 2024 GDP growth at 1.3% (up from 1.1%).

- Fiscal 2022 CPI at 2.3% (up from 1.9%).

- Fiscal 2023 CPI at 1.4% (up from 1.1%).

- Fiscal 2024 CPI at 1.3% (up from 1.1%).

- Fiscal 2022 CPI core-core (ex-fresh food and energy) at 1.3% (up from 0.9%).

- Fiscal 2023 CPI core-core at 1.4% (up from 1.2%).

- Fiscal 2024 CPI core core at 1.5% (unchanged).

New Zealand good imports jumped 25% yoy on petroleum, imports rose 7.7% yoy

New Zealand goods exports rose 7.7% yoy to NZD 6.4B in June. Goods imports rose 25.0% yoy to NZD 7.1B. Trade balance came in at NZD -701m deficit, versus expectation of NZD 204m surplus.

“Petroleum and products imports rose $795 million to reach a new high of $1.2 billion,” Stats NZ. “This rise lead the sharp increase in total imports for the month compared with June 2021.”

US leads monthly export rise, up 22%. Exports to EU were up 28% and Japan up 24%. Exports to China were down -6% and to Australia down -12%.

Import form all top partners rose, with China up 12%, EU up 11%, Australia up 6%, US up 30%, and Japan up 4.1%.

Australia NAB business condition rose to 20 in Q2, but confidence dropped to 5

Australia NAB quarterly business confidence dropped from 15 to 5 in Q2. Current business conditions rose from 11 to 20. Next 3 months business conditions was unchanged at 26. next 12 months business conditions dropped from 34 to 29. Capex plan for next 12 months dropped from 33 to 31.

Alan Oster, NAB Group Chief Economist, “Conditions strengthened in Q2 as the disruptions related to the virus receded. Trading, profitability, and employment were all higher with conditions approaching the high levels seen in early 2021.”

“Confidence eased in Q2, down to around long-run average levels,” said Oster. “That likely reflects the waning of some of the pandemic-recovery optimism, as well as the mounting challenges of rising inflation and also rising interest rates that businesses are confronting.”

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8481; (P) 0.8510; (R1) 0.8528; More…

EUR/GBP’s break of 0.8552 minor resistance argues that corrective fall from 0.8720 has completed at 0.8401. The development also revived near term bullishness. Intraday bias is back on the upside for retesting 0.8720 resistance first. Firm break there will resume larger rally from 0.8201. On the downside, below 0.8491 minor support will bring retest of 0.8401 support instead.

In the bigger picture, attention remains on 38.2% retracement of 0.9499 to 0.8201 at 0.8697. Sustained break there will affirm the case that rise from 0.8201 is a medium term up trend itself. Further rally would then be seen to 61.8% retracement at 0.9003. However, rejection by 0.8697 will confirm medium term bearishness for another fall through 0.8201.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jun | -701M | 240M | 263M | 195M |

| 23:50 | JPY | Trade Balance (JPY) Jun | -1.93T | -2.01T | -1.93T | -1.89T |

| 01:30 | AUD | NAB Business Confidence Q2 | 5 | 14 | 15 | |

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 22.1B | 21.3B | 13.2B | 11.8B |

| 12:15 | EUR | ECB Interest Rate Decision | 0.50% | 0.25% | 0.00% | |

| 12:30 | CAD | New Housing Price Index M/M Jun | 0.20% | 0.40% | 0.50% | |

| 12:30 | USD | Initial Jobless Claims (Jul 15) | 251K | 240K | 244K | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jul | -12.3 | -0.5 | -3.3 | |

| 12:45 | EUR | ECB Press Conference | ||||

| 14:30 | USD | Natural Gas Storage | 45B | 58B |