US stocks tumbled sharply overnight after the West unveiled a wave a sanctions on Russia’s invasion on Ukraine, and warned that more are underway. But other markets were pretty steady, with Asian markets trading mildly higher. Gold is struggling to stand above 1900 handle. WTI crude oil is also gyrating below 96.

In the currency markets, New Zealand dollar rises broadly after more hawkish than expected RBNZ rate hike. Aussie and Canadian Dollar are following next. Dollar is the softest for today, followed by Euro and Yen. Sterling and Swiss Franc are mixed. There is no clear safe-haven flow in the forex markets.

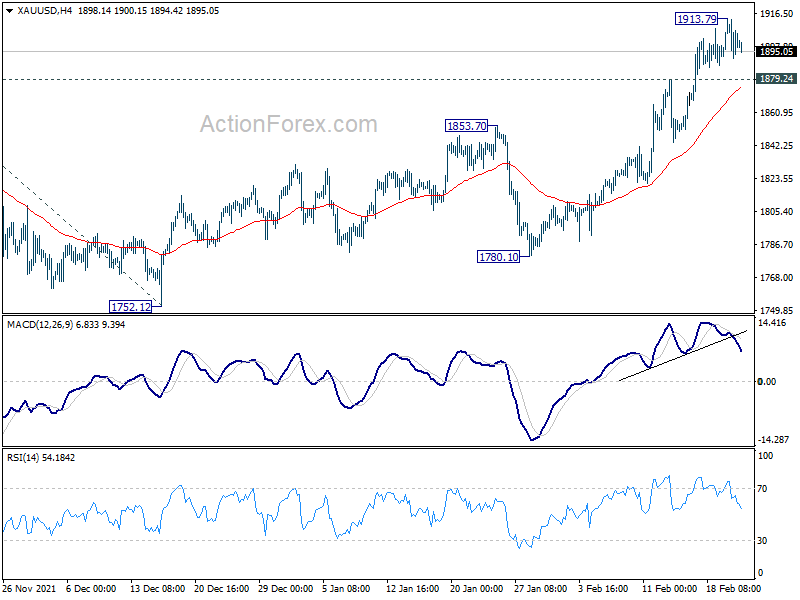

Technically, some attention will be paid to Gold. Firm break of 1879.24 minor support will confirm short term topping at 1913.79. Deeper pull back could be seen back to 1853.70 resistance turned support and possibly below. That, if happens, might be a sign of reverse safe-haven flows in other markets.

In Asia, at the time of writing, Hong Kong HSI is up 0.84%. China Shanghai SSE is up 0.78%. Singapore Strait Times is down -0.35%. Japan is on holiday. Overnight, DOW dropped -1.42%. S&P 500 dropped -1.01%. NASDAQ dropped -1.23%. 10-year yield rose 0.016 to 1.948.

RBNZ hikes rate to 1%, starts managed bond sales, raised OCR peak forecast

RBNZ raised OCR by 25bps to 1.00% as widely expected. Additionally, it will start to start reduction of the bond holdings under the Large Scale Asset Purchase program through “both bond maturities and managed sales.

The central bank also said “further removal of monetary policy stimulus is expected over time given the medium-term outlook for growth and employment, and the upside risks to inflation.”

In the minutes, it’s noted, “when deciding whether to move the OCR up by 25 or 50 basis points, many members saw this as a finely balanced decision.”

However, firstly, the active sales of bond holdings may “put some upward pressure on longer-term interest rates”. Also, the OCR is expected to “peak at a higher level than assumed” at the November MPC. The OCR peak was raised to around 3.4% in 2024, compared to 2.6% in November review.

Hence, the Committee came to a consensus of a 25bps hike, but “affirmed that it was willing to move the OCR in larger increments if required over coming quarters.”

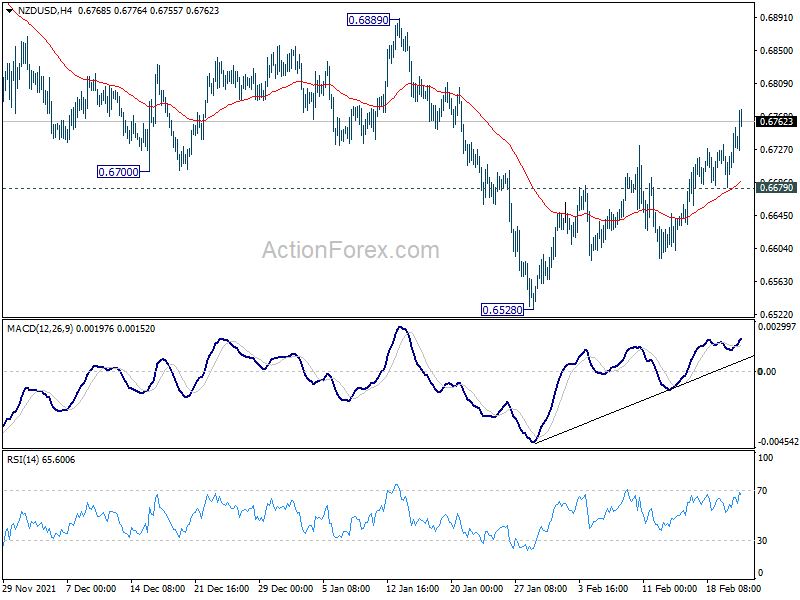

NZD/USD extends rebound after RBNZ, AUD/NZD dips

New Zealand Dollar rises broadly after more hawkish than expected RBNZ policy decision. NZD/USD is extending the rebound from 0.6528 short term bottom. Further rise is now expected as long as 0.6679 minor support holds, to 0.6889 resistance next.

It’s still too early to conclude that NZD/USD’s down trend from 0.7463 has completed. Rejection by 0.6889 resistance will maintain medium term bearishness for another decline through 0.6528 low. Nevertheless, firm break of 0.6889 will raise then chance of bullish reversal and turn focus to trend line resistance at around 0.7080.

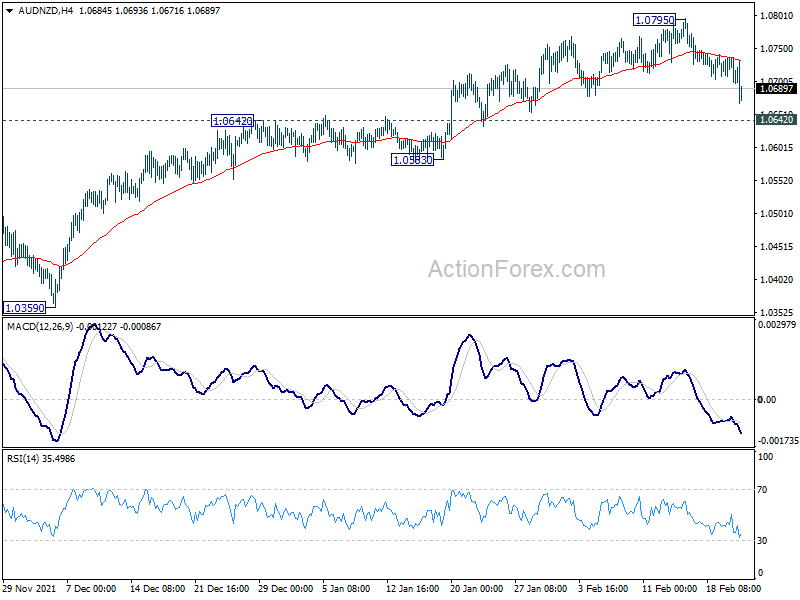

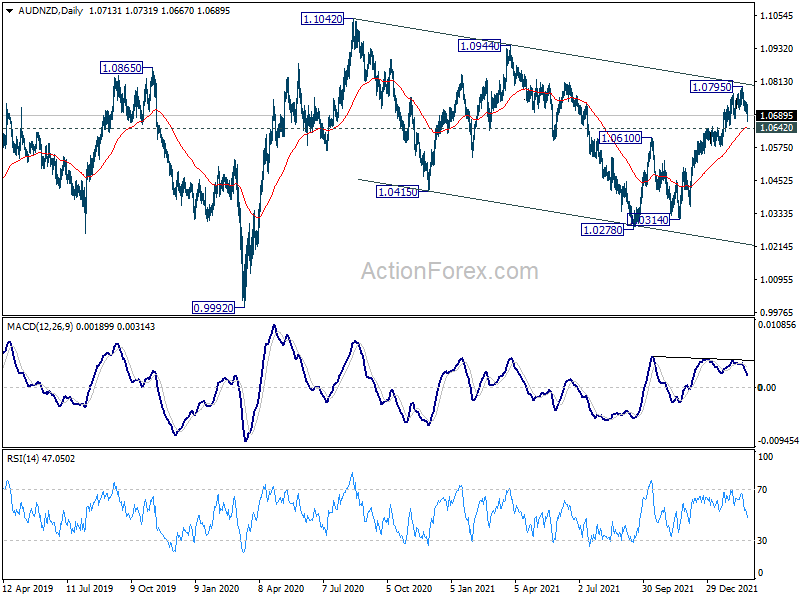

AUD/NZD dips notably too and immediate focus is now on 1.0642 resistance turned support, which is also close to 55 day EMA (now at 1.0649). Sustained break there will argue that whole rise from 1.0278 has completed at 1.0795, after rejection by medium term channel resistance. In this case, fall from 1.0795 should develop into another falling leg to the whole down trend from 1.1042, targeting 1.0278 low again.

Fed Bostic: Fed can pull back some support without jeopardizing employment

Atlanta Fed President Raphael Bostic said yesterday that the US economy is “still quite strong”. It’s in a situation “where it can stand on its own”. Thus, Fed can pull back some emergency support “without jeopardizing employment.”

Bostic also noted that the new sanctions on Russia provided some uncertainty. And, “that kind of uncertainty is a downward risk to economic output” that will be factored into how he thinks about monetary policy.

Elsewhere

Australia wage price index rose 0.7% qoq in Q4, matched expectations. Construction work down dropped -0.4% in Q4, below expectation of 2.1%.

Looking ahead, Germany Gfk consumer confidence, Swiss ZEW expectations, and Eurozone CPI final will be released in European session. The US calendar is empty today.

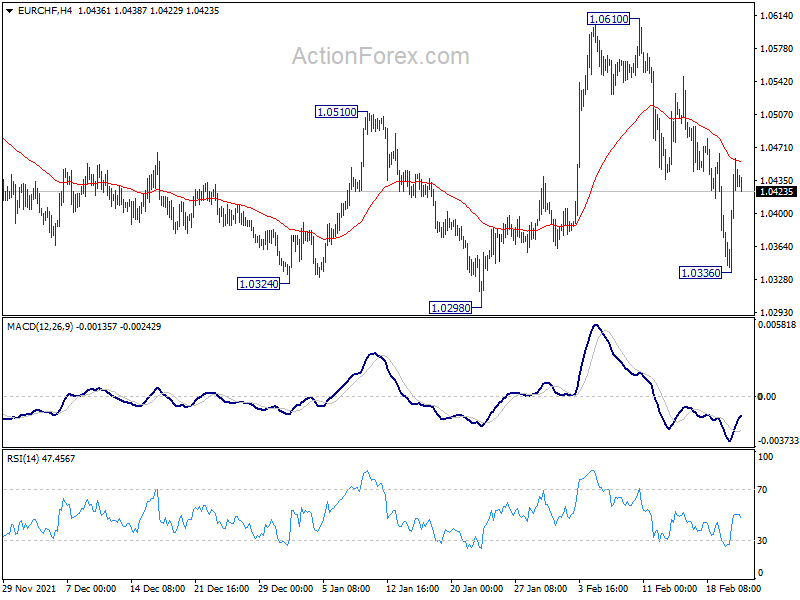

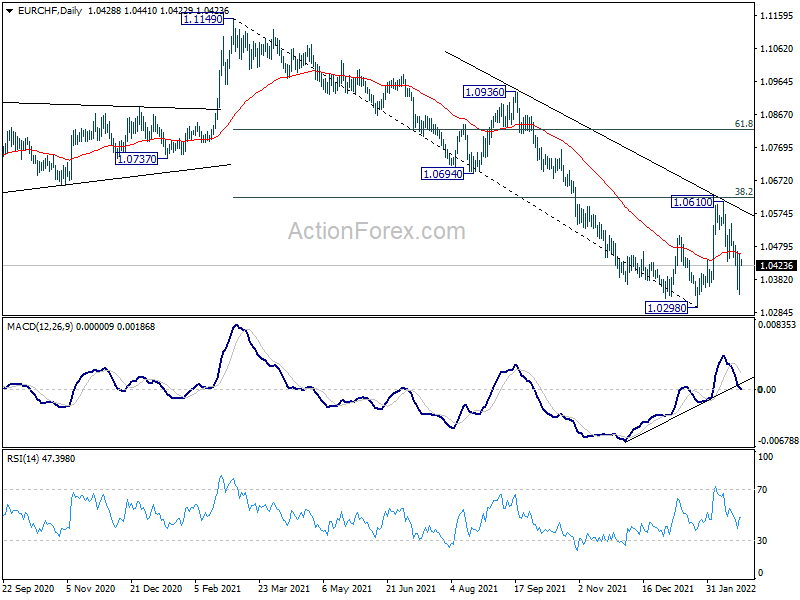

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0364; (P) 1.0413; (R1) 1.0487; More….

EUR/CHF rebounded strongly after hitting 1.0336 and intraday bias is turned neutral first. Corrective pattern from 1.0298 might be extending with another leg. But even in case of stronger rise, up side should be limited by 38.2% retracement of 1.1149 to 1.0298 at 1.0623. On the downside, below 1.0336 will target 1.0298 low first. Firm break there will confirm larger down trend resumption.

In the bigger picture, a medium term bottom was formed at 1.0298 on bullish convergence condition in daily MACD. Rebound from there is still tentatively viewed part of a corrective pattern. That is, larger down trend from 1.2004 (2018) could still extend through 1.0298 to 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223. However, sustained trading above 55 week EMA (now at 1.0667) will argue that the down trend is over, and bring stronger rise back to 1.1149 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q4 | 0.70% | 0.70% | 0.60% | |

| 00:30 | AUD | Construction Work Done Q4 | -0.40% | 2.10% | -0.30% | -1.20% |

| 01:00 | NZD | RBNZ Interest Rate Decision | 1.00% | 1.00% | 0.75% | |

| 02:00 | NZD | RBNZ Press Conference | ||||

| 07:00 | EUR | Germany Gfk Consumer Confidence Mar | -6.2 | -6.7 | ||

| 09:00 | CHF | ZEW Expectations Feb | 9.5 | |||

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 5.10% | 5.10% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 2.30% | 2.30% |