Risk sentiment turns sour again as the arrangement for a Biden-Putin summit looks far from being promising. As the same time, there seems to be some scattered escalations in Russia-Ukraine situations. Major European indexes are trading mildly lower, together with US futures. Gold is holding in tight range slightly below 1900 handle. But in the currency markets, Swiss Franc surges sharply today on safe-haven flow. Meanwhile, Dollar and Euro are under some selling pressure. Economic data are largely ignored.

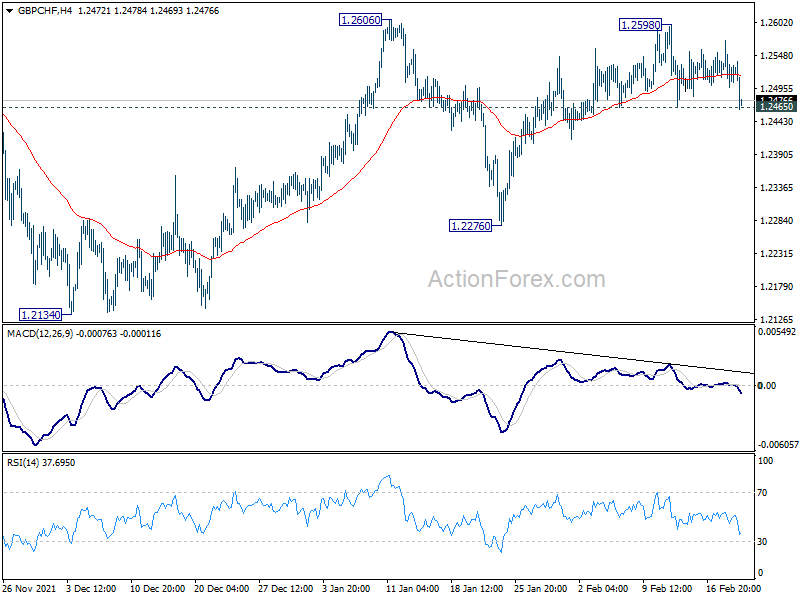

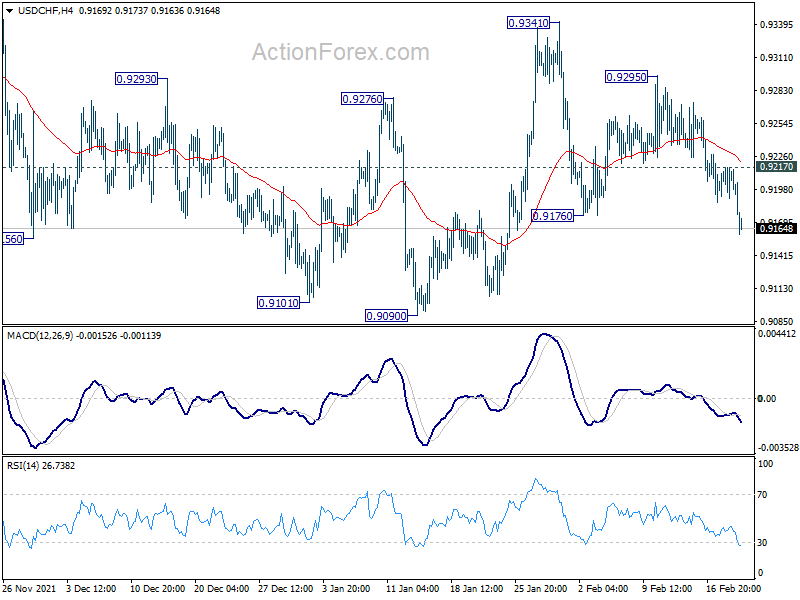

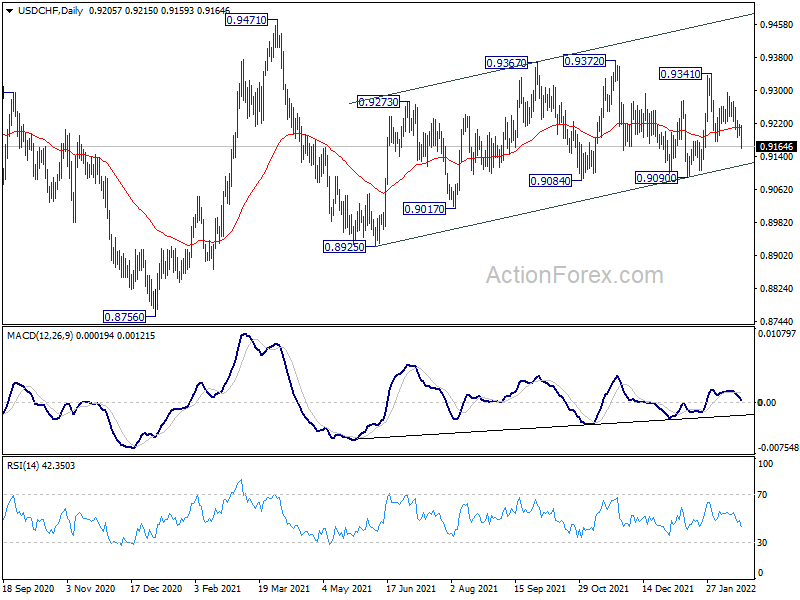

Technically, we’d continue to focus on developments in Swiss Franc crosses. USD/CHF’s break of 0.9176 minor support suggests that deeper fall is now in progress. But sustained break of 0.9090 support is still needed to turn near term outlook full bearish. EUR/CHF is heading towards 1.0298 low and firm break there will confirm medium term down trend resumption. Meanwhile, as noted earlier today, break of 1.2465 support in GBP/CHF will suggest that rise from 1.2276 has completed and bring deeper fall back to this level.

In Europe, at the time of writing, FTSE is down -0.56%. DAX is down -1.93%. CAC is down -2.08%. Germany 10-year yield is up 0.006 at 0.198. Earlier in Asia, Nikkei dropped -0.78%. Hong Kong HSI dropped -0.65% China Shanghai SSE dropped -0.00%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield dropped -0.0115 to 0.209.

UK PMI Manufacturing unchanged at 57.3, services jumped to 60.2

UK PMI Manufacturing was unchanged at 57.3 in February, below expectation of 57.5. PMI Services surged from 54.1 to 60.8, above expectation of 55.2, an 8-month high. PMI Composite rose from 54.2 to 60.2, also an 8-month high.

Chris Williamson, Chief Business Economist at IHS Markit, said:

“The latest PMI surveys indicate a resurgent economy in February, as business activity leapt as COVID-19 containment measures were relaxed.

“With the PMI’s gauge of output growth accelerating markedly in February and cost pressures intensifying to the second-highest on record, the odds of an increasingly aggressive policy tightening have shortened, with a third back-to-back rate rise looking increasingly inevitable in March.

“However, the indications of a growing plight for manufacturers will need to be watched, and the service sector’s new business index will need to be monitored for signs of the demand revival losing steam. Given the rising cost of living, higher energy prices and increased uncertainty caused by the escalating crisis in Ukraine, downside risks to the demand outlook have risen.”

Bundesbank: German economy to decline in Winter, pick up again in Spring

Bundesbank said in the latest monthly report that German economic output is likely to decline noticeably again in the winter quarter of 2022.

But economic prospects are “good”. It said, “in view of the very good demand situation, the German economy should pick up speed again in the spring, provided that the pandemic subsides and the supply bottlenecks continue to ease.”

“Thus, from today’s perspective, the economic outlook is only slightly less favorable than expected in the projections from December 2021, despite the increased burden caused by the pandemic and high inflation,”conclude the experts.

Eurozone PMI manufacturing dipped to 58.4, but services jumped to 55.8

Eurozone PMI Manufacturing dipped slightly from 58.7 to 58.4 in February, below expectation of 58.7. PMI Services, on the other hand, jumped from 51.1. to 55.8, above expectation of 51.7. PMI Composite rose from 52.3 to 55.8, a 5-month high.

Chris Williamson, Chief Business Economist at IHS Markit said:

“The eurozone economy regained momentum in February as an easing of virus-fighting restrictions led to renewed demand for many consumer services, such as travel, tourism and recreation, and helped alleviate supply bottlenecks. Business optimism in the outlook has likewise improved as companies look to the further reopening of the economy, encouraging increased hiring.

“However, although easing, supply constraints remain widespread and continue to cause rising backlogs of work. As such, demand has again outstripped supply, handing pricing power to producers and service providers. At the same time, soaring energy costs and rising wages have added to inflationary pressures, resulting in the largest rise in selling prices yet recorded in a quarter of a century of survey data history.

“The strength of the rebound in business activity signalled by the PMI provides welcome evidence that the economy has so far shown encouraging resilience in the face of the Omicron wave, but the intensification of inflationary pressures will add to speculation of an increasing hawkish stance at the ECB.”

Germany PMI Manufacturing dropped from 59.8 to 58.5 in February, below expectation of 59.4. PMI Services rose from 52.2 to 56.6 in February, above expectation of 53.2, highest in six months. PMI Composite rose from 53.8 to 56.2, also the highest in six months.

France PMI Manufacturing rose from 55.5 to 57.6 in February, above expectation of 55.5, highest in 7 months. PMI Services rose from 53.1 to 57.9, above expectation of 53.5, highest in 49 months. PMI Composite rose from 52.7 to 57.4, highest in 8 months.

Australia PMI composite jumped to 55.9, economy bounced back quickly

Australia PMI Manufacturing rose from 55.1 to 57.6 in February. PMI Services jumped from 46.6 to 56.4, an 8-month high. PMI Composite rose from 46.7 to 55.9, also an 8-month high.

Jingyi Pan, Economics Associate Director at IHS Markit, said:

“The Australian economy bounced back quickly in February, according to the IHS Markit Flash Australia Composite PMI, after contracting sharply at the start of 2022, hit by the COVID-19 Omicron wave.

“Demand and output both returned to growth, boding well for hiring activity in February. That said, shortages of input materials and labour persisted as issues for private sector firms. This led to input prices continuing to increase sharply while selling price inflation hit a record according to the latest PMI survey. While this perhaps comes as no surprise in the initial recovery phase from the latest COVID-19 wave, the lingering impact on overall inflation and wages will have to be closely followed.

“Business confidence amongst private sector firms improved once again in February after briefly dipping in January, reflecting the short-lived nature of the latest COVID-19 wave, which was a positive sign.”

Japan PMI manufacturing dropped to 52.9 in Feb, services dropped to 42.7

Japan PMI Manufacturing dripped from 55.4 to 52.9 in February, below expectation of 55.0. PMI Services dropped sharply from 47.6 to 42.7, worst reading since May 2020. PMI Composite dropped from 49.9 to 44.6.

Usamah Bhatti, Economist at IHS Markit, said:

“Activity at Japanese private sector businesses contracted sharply during February as the Omicron variant of COVID-19 led to record case numbers and renewed restrictions in Japan. The decline was the second in successive months though was the sharpest recorded for 20 months and came amid the steepest downturn in the services sector since the first wave of the pandemic in May 2020. Moreover, manufacturers signalled a reduction in output for the first time in five months, though the rate of contraction was considerably softer than that seen in the dominant services sector, and was only mild overall.

“Private sector firms also noted a decrease in aggregate new business for the first time since September, largely driven by domestic reductions while new export orders broadly stagnated. Firms continued to report that rising input prices and material shortages, notably in fuel and metals continued to dampen private sector activity. In fact, February saw the strongest rise in average cost burdens since August 2008.

“Companies were optimistic that activity would improve in the year ahead, though the continued resurgence of COVID-19 had clouded the outlook and drove optimism to a six-month low.”

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9197; (P) 0.9208; (R1) 0.9223; More….

Intraday bias in USD/CHF mildly on the downside with break of 0.9176 support. Fall from 0.9341 could now target 0.9090 near term support. Firm break there will argue that choppy rise from 0.8925 has completed and bring deeper decline to this support. Nevertheless, above 0.9217 minor resistance will turn intraday bias neutral again, and retain some mild near term bullish flavor.

In the bigger picture, medium term outlook will be neutral at best as long as 0.9471 resistance holds. Larger down trend could still extend through 0.8756 (2021 low). However, firm break of 0.9471 will argue that the trend has already reversed and rebound the rally from 0.8756 with another impulsive move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | CBA Manufacturing PMI Feb P | 57.6 | 55.1 | ||

| 22:00 | AUD | CBA Services PMI Feb P | 56.4 | 46.6 | ||

| 00:30 | JPY | Manufacturing PMI Feb P | 52.9 | 55 | 55.4 | |

| 07:00 | EUR | Germany PPI M/M Jan | 2.20% | 1.50% | 5.00% | |

| 07:00 | EUR | Germany PPI Y/Y Jan | 25.00% | 24.20% | 24.20% | |

| 08:15 | EUR | France Manufacturing PMI Feb P | 57.6 | 55.5 | 55.5 | |

| 08:15 | EUR | France Services PMI Feb P | 57.9 | 53.5 | 53.1 | |

| 08:30 | EUR | Germany Manufacturing PMI Feb P | 58.5 | 59.4 | 59.8 | |

| 08:30 | EUR | Germany Services PMI Feb P | 56.6 | 53.2 | 52.2 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb P | 58.4 | 58.7 | 58.7 | |

| 09:00 | EUR | Eurozone Services PMI Feb P | 55.8 | 51.7 | 51.1 | |

| 09:30 | GBP | Manufacturing PMI Feb P | 57.3 | 57.5 | 57.3 | |

| 09:30 | GBP | Services PMI Feb P | 60.8 | 55.2 | 54.1 |