It looks like ECB is beating BoE in the race of hawkish surprise in a jam-packed day. Sterling spiked higher after four of the nine MPC members have indeed voted for a larger hike of 50bps. However, there was no clear follow through buying as BoE indicated there will only be “some further modest tightening” ahead.

On the other hand, ECB President Christine Lagarde admitted in the post-meeting press conference that inflation surprises caused unanimous concerns in the Governing Council. More importantly, she refused to repeat the talk that a rate hike in 2022 remain highly likely. It seems that Lagarde is leaving the door open to a change in forward guidance in March to reflect the chance of a rate hike within this year.

Elsewhere in the forex markets, Dollar is recovery mildly today but remains the weakest one for the week, followed by Yen. Aussie is still the strongest but it’s path would depend on overall risk sentiment.

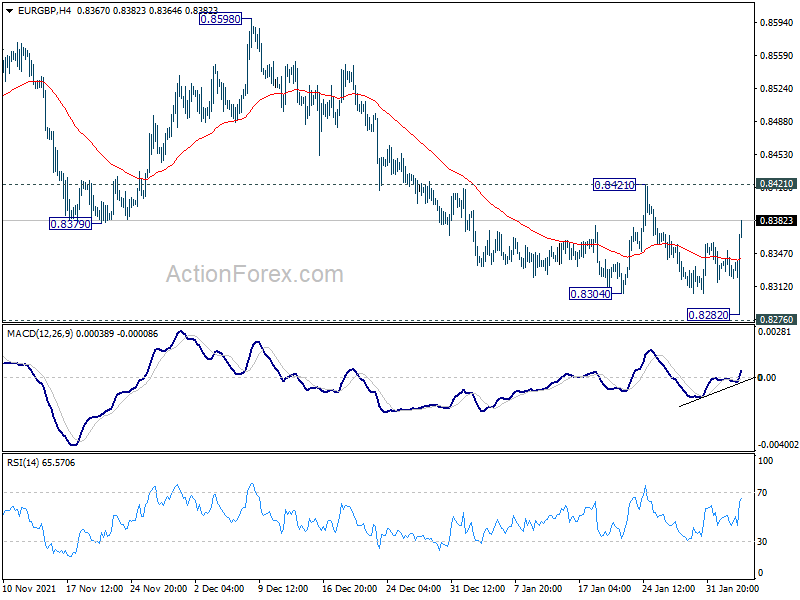

Technically, a major focus now is whether EUR/GBP could ride on the u-turn to power through 0.8421 resistance, to pave the way for bullish trend reversal just ahead of 0.8276 key long term support.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is down -0.28%. CAC is down -0.07%. Germany 10-year yield is up 0.039 at 0.081, marching towards 0.1 handle. Earlier in Asia, Nikkei dropped -1.06%. Japan 10-year JGB yield rose 0.001 to 0.180. Singapore Strait Times rose 2.04%. Hong Kong and China were on holiday.

US initial jobless claims dropped back to 238k

US initial jobless claims dropped -23k to 238k in the week ending January 29, much better than expectation of 264k. Four-week moving average of initial claims rose 8k to 255k.

Continuing claims dropped -44k to 1628k in the week ending January 22. Four-week moving average of continuing claims dropped -31k to 1620k, lowest since August 4, 1973.

BoE hikes 25bps to 0.50%, but four members want 50bps

BoE raises Bank Rate by 0.25% to 0.50% today, by a slight majority of 5-4 vote. Four hawks (Jonathan Haskel, Catherine L Mann, Dave Ramsden, Michael Saunders) voted for a more aggressive 50bps hike to 0.75%. The other five (Andrew Bailey, Ben Broadbent, Jon Cunliffe, Huw Pill, Silvana Tenreyro) won the vote.

Meanwhile, the MPC voted unanimously to begin to reduce stock of government bonds by ceasing to reinvest maturing assets. It also decided to start reducing stock of corporate bonds by ceasing to reinvest maturing assets and complete a bond sales program no earlier than towards the end of 2023.

Going forward, the extent of any further tightening in monetary policy will “depend on the medium-term prospects for inflation”. If the economy develops broadly in line with the February Report central projections, “some further modest tightening in monetary policy is likely to be appropriate in the coming months.”

In the new four-quarter GDP projections:

- 2022 Q1 was revised down from 9.5% to 7.8%.

- 2023 Q1 was revised down from 2.1% to 1.8%.

- 2024 Q1 was revised up from 1.0% to 1.1%.

- 2025 Q1 was at 0.9% (new).

CPI inflation projections:

- 2022 Q1 raised from 4.6% to 5.7%.

- 2023 Q1 raised from 3.3% to 5.2%.

- 2024 Q1 unchanged at 2.1%.

- 2025 Q1 to slow to 1.6%.

Unemployment rate projections:

- 2022 Q1 lowered from 4.2% to 3.8%.

- 2023Q1 raised from 4.0% to 4.2%.

- 2024 Q1 raised from 4.2% to 4.6%.

- 2025 Q1 to rise to 5.0%.

Implied path for Bank Rate:

- 2022 Q1 lowered from 0.5% to 0.4%.

- 2023 Q1 raised from 1.0% to 1.3%.

- 2024 Q1 raised from 1.0% to 1.4%.

- 2025 Q1 at 1.3%.

UK PMI services finalized at 54.1, goods news about 2022 prospect

UK PMI Services was finalized at 54.1 in January, up from December’s 10-month low of 53.6. PMI Composite was finalized at 54.2, up from prior month’s 53.6. Markit said charges had fastest rise on record in more than 25 years. Output and new business picked up at the start of 2022. Growth projections were strongest since May 2021.

ECB stands pat, maintains forward guidance

ECB keeps interest rates unchanged today. The main refinancing rate, marginal lending facility rate and deposit facility rate are held at 0.00%, 0.25%, and -0.50% respectively.

It maintains the forward guidance that interest rates will “remain at their present or lower levels” until ECB sees inflation “reaching 2% well ahead of the end of tis projection horizon and durably for the rest of the projection horizon”. Also, ECB will need to judges that realized progress in underlying inflation is “sufficiently advanced to be consistent with inflation stabilizing at 2% over the medium term.”.

ECB also reiterated that it will discontinue net PEPP purchases at the end of march 2022, and reinvests until at least the end of 2024. APP net monthly purchases will amount to EUR 40B in Q2, then EUR 30B in Q3, and back to monthly pace of EUR 20B from October onwards, (for as long as necessary”.

Eurozone PPI rose 2.9% mom, 26.2% yoy in Dec

Eurozone PPI rose 2.9% mom, 26.2% yoy in December, slightly below expectation of 3.0% mom, 26.6% yoy. For the month, industrial producer prices increased by 7.0% mom in the energy sector, by 0.7% mom for intermediate goods, by 0.6% mom for non-durable consumer goods, by 0.3% mom for capital goods and by 0.2% mom for durable consumer goods. Prices in total industry excluding energy increased by 0.5% mom.

EU PPI rose 2.9% mom, 26.2% yoy. The highest monthly increases in industrial producer prices were recorded in Ireland (+13.3%), Estonia (+12.7%) and Greece (+8.0%), while the only decrease was observed in Czechia (-0.1%).

Eurozone PMI composite finalized at 52.3, economy slowed further

Eurozone PMI Services was finalized at 51.1 in January, down from December’s 53.1. PMI Composite was finalized at 52.3, down from prior month’s 53.3. Looking at some member states, Ireland PMI Composite was unchanged at 56.5, Germany dropped to 4-month low at 53.8, France dropped to 9-month low at 52.7, Italy dropped to 12-month low at 50.1, and Spain dropped to 11-month low at 47.9.

BoJ Wakatabe: Definitely too early to start tightening

BoJ Deputy Governor Masazumi Wakatabe said in a speech, “given the current situation where Japan’s economy has finally started to pick up from the pandemic, it is definitely too early for the Bank to start tightening monetary policy when the target has not yet been achieved as this could hinder the economic recovery.”

He reiterated the current policy as to continue with QQE with yield curve control, “as long as it is necessary” to maintain 2% inflation target in a “stable manner”. That is, CPI should remain at 2% while medium- to long-term inflation expectations are “anchored”.

Australia NAB business confidence rose to 18 in Q4

Australia NAB business confidence jumped from -2 to 18 in Q4. Current business conditions was unchanged at 12. Conditions for the next 3 months rose from 8 to 30. Conditions for the next 12 months also rose from 26 to 34. Capex plans rose from 26 to 34.

“The economy was showing considerable strength prior to the spread of the Omicron variant, and that translated into a positive outlook for the coming months,”Alan Oster, NAB Group Chief Economist. “We now know that Omicron has dampened that recovery somewhat but, fundamentally, we expect that positive trajectory to continue when the current virus outbreak recedes.”

Also released, goods and services export rose 1% mom to AUD 45.32B in December. Goods and services imports rose 5% mom to AUD 36.96B. Trade surplus narrowed to AUD 8.36B, below expectation of AUD 9.80B. AiG Performance of Construction index dropped from 57 to 45.9 in December. Building permits rose 8.2% mom in December.

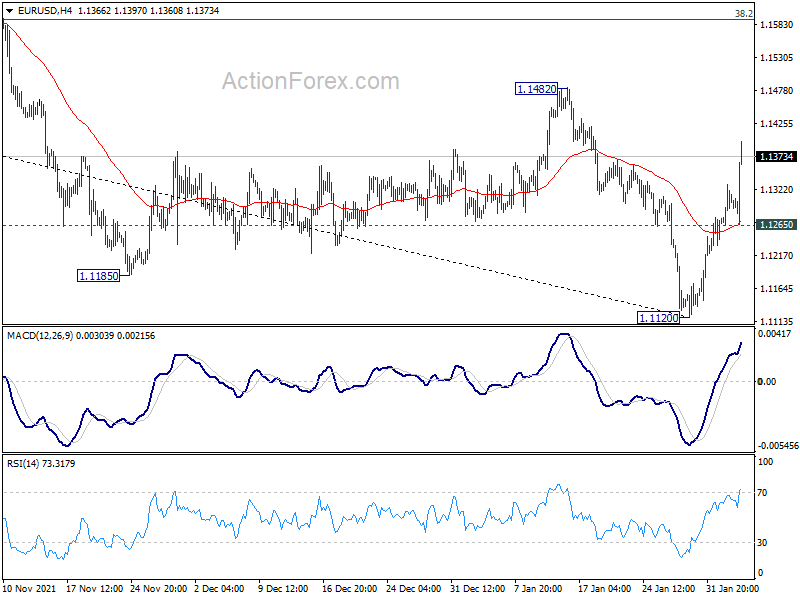

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1272; (P) 1.1301; (R1) 1.1335; More…

EUR/USD’s rebound from 1.1120 accelerates higher today and intraday bias stays on the upside for 1.1482 resistance. Considering bullish convergence condition in daily MACD, a medium term bottom could be in place already. Break of 1.1482 will affirm this case and target 38.2% retracement of 1.2348 to 1.1120 at 1.1639 next. On the downside however, break of 1.1265 minor support will retain near term bearishness, and flip bias back to the downside for retesting 1.1120 low instead.

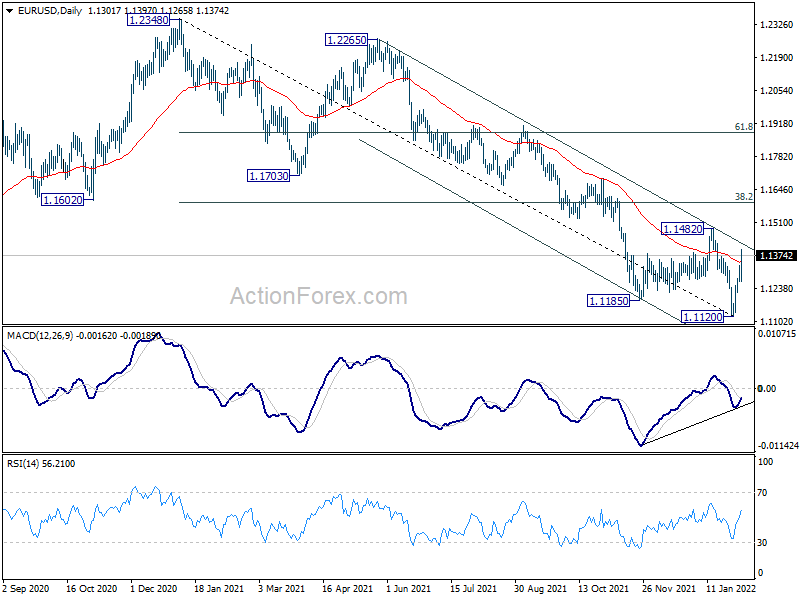

In the bigger picture, the strength of the the decline from 1.2348 (2021 high) suggests that it’s not a corrective move. But still, it could be the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1482 resistance holds. Next target would be 1.0635 low. However, firm break of 1.1482 will raise the chance that whole fall from 1.2348 has completed, and turn focus back to 1.1703 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Dec | 45.9 | 57 | ||

| 00:30 | AUD | Building Permits M/M Dec | 8.20% | -0.90% | 3.60% | 2.60% |

| 00:30 | AUD | Trade Balance (AUD) Dec | 8.36B | 9.80B | 9.42B | 9.76B |

| 08:50 | EUR | France Services PMI Jan F | 53.1 | 53.1 | 53.1 | |

| 08:55 | EUR | Germany Services PMI Jan F | 52.2 | 52.2 | 52.2 | |

| 09:00 | EUR | Eurozone Services PMI Jan F | 51.1 | 51.2 | 51.2 | |

| 09:30 | GBP | Services PMI Jan F | 54.1 | 53.5 | 53.3 | |

| 10:00 | EUR | Eurozone PPI M/M Dec | 2.90% | 3.00% | 1.80% | |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | 26.20% | 26.60% | 23.70% | |

| 12:00 | GBP | BoE Interest Rate Decision | 0.50% | 0.50% | 0.25% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 7–0–2 | 8–0–1 | |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -76.00% | -75.30% | ||

| 12:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | USD | Initial Jobless Claims (Jan 28) | 238K | 264K | 260K | 261K |

| 13:30 | USD | Nonfarm Productivity Q4 P | 6.60% | 2.80% | -5.20% | |

| 13:30 | USD | Unit Labor Costs Q4 P | 0.30% | 1.50% | 9.60% | |

| 14:45 | USD | Services PMI Jan F | 50.9 | 50.9 | ||

| 15:00 | USD | ISM Services PMI Jan | 58.7 | 62 | ||

| 15:00 | USD | ISM Services Prices Paid Jan | 83 | 82.5 | ||

| 15:00 | USD | Factory Orders M/M Dec | 0.10% | 1.60% | ||

| 15:30 | USD | Natural Gas Storage | -280B | -219B |