Dollar’s strong post-FOMC rally is given another boost in early US session by much better than expected Q4 GDP data. Latest jobless claims figures also suggest stabilization from the impact of Omicron. But for now, the strength is mainly centered against European majors and Yen. Canadian Dollar is indeed lifted slightly as oil prices extend recent up trend. In other markets, US future bent upward from earlier slump and now point to recovery. Gold is pressing 1800 handle while WTI oil at around 88.8.

Technically, EUR/USD’s break of 1.1185 support confirms resumption of down trend from 1.2348. USD/JPY’s break of 115.05 minor resistance revives near term bullishness. Focuses are now on 1.3158 low in GBP/USD, 0.6692 low in AUD/USD and 115.05 high in USD/JPY to further confirm Dollar’s underlying bullishness.

In Europe, at the time of writing, FTSE is up 0.88%. DAX is up 0.04%. CAC is up 0.15%. Germany 10-year yield i up 0.025 at -0.048. Earlier in Asia, Nikkei dropped -3.11%. Hong Kong HSI dropped -1.99%. China Shanghai SSE dropped -1.78.% Singapore Strait Times dropped -0.35%. Japan 10-year JGB yield rose 0.0192 to 0.159.

US GDP grew 6.9% annualized in Q4, well above expectations

US GDP grew at 6.9% annualized rate in Q4, faster than Q3’s 2.3%, well above expectation of 5.6%. The increase in real GDP primarily reflected increases in private inventory investment, exports, personal consumption expenditures (PCE), and nonresidential fixed investment that were partly offset by decreases in both federal and state and local government spending. Imports, which are a subtraction in the calculation of GDP, increased.

For 2021 as a whole, real GDP grew 5.8% The increase in real GDP in 2021 reflected increases in all major subcomponents, led by PCE, nonresidential fixed investment, exports, residential fixed investment, and private inventory investment. Imports increased.

US durable goods orders dropped -0.9% mom in Dec, led by transportation equipment

US durable goods orders dropped -0.9% mom, or USD -2.4B to USD 267.6B in December, worse than expectation of -0.5%. Ex-transport orders rose 0.4% mom, above expectation of 0.5% mom. Ex-defense orders rose 0.1%. Transportation equipment dropped USD -3.3B, or -3.9% mom to USD -80.1B.

US initial jobless claims dropped to 260k, matched expectations

US initial jobless claims dropped -30k to 260k in the week ending January 22, matched expectations. Four-week moving average of initial claims rose 15k to 247k.

Continuing claims rose 51k to 1675k in the week ending January 15. Four-week moving average of continuing claims dropped -11k to 1652k, lowest since August 18, 1973.

Swiss exports rose to record in 2021, US became largest buyer

Swiss trade surplus came in at CHF 3.69B in December, below expectation of CHF 5.23B. For 2021 as a whole, exports rose 15.2% to a new record high at CHF 259.5B. Imports rose 10.1% to CHF 200.8B. Trade surplus swelled to CHF 58.7B.

Also, the FOCBS said US became Switzerland’s largest buyer in 2021. Foreign trade with China rose to new high. Double-digit growth rates were observed in deliveries to Europe (+18.1%, or +21.9B) and North America (+17.0%, or +7.4B). Shipments to Asia were also up by 9.0%, or CHF 4.4B.

Germany Gfk consumer sentiment rose to -6.7, assuming pandemic to ease in spring

Germany Gfk Consumer Sentiment for February rose 0.2 pts to -6.7, better than expectation of -8.0. In January, economic expectations rose from 17.1 to 22.8. Income expectations rose from 6.9 to 16.9. Propensity to buy rose from 0.8 to 5.2.

“Despite rising incidences and inflation, consumers are once again showing some optimism at the beginning of the year. In particular, they are hoping for a slight alleviation in price trends, as in January 2022 the base effect resulting from the January 2021 reversal of the VAT cut will mitigate the inflation rate to some degree. Nevertheless, consumers price expectations remain significantly higher than in recent years.”, explains Rolf Bürkl, GfK consumer expert. “In addition, experts assume that the pandemic situation would ease in the spring, which will lead to a number of restrictions being removed.”

New Zealand CPI surges to 5.9% yoy, NZD/USD dives on risk aversion

New Zealand CPI rose 1.4% qoq in Q4, above expectation of 1.2% yoy. Annual rate accelerated from 4.9% yoy to 5.9% yoy, above expectation of 5.6% yoy. That’s the highest level in three decades since 1990.

“New Zealand is not alone, with many other OECD countries experiencing higher inflation than in recent decades,” consumers prices senior manager Aaron Beck said. “Price increases were widespread with 10 out of 11 main groups in the CPI basket increasing in the year, with only the communications group decreasing.”

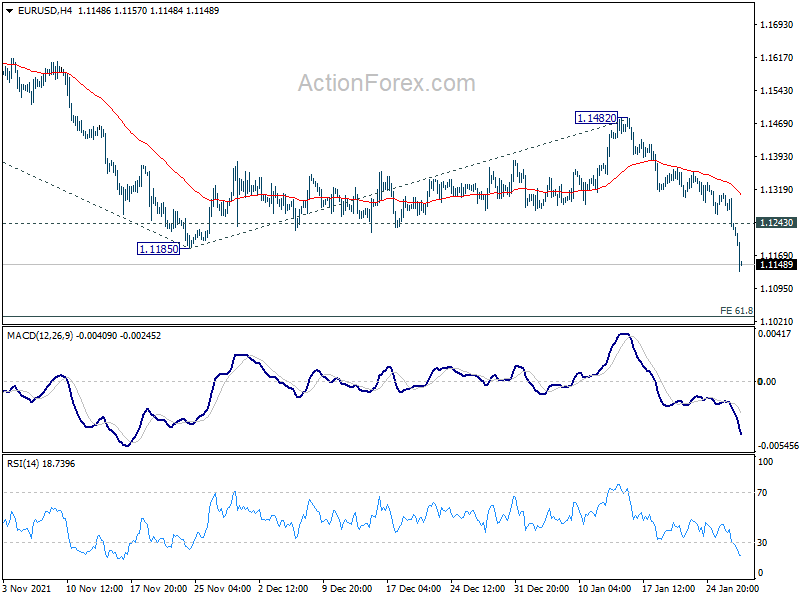

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1216; (P) 1.1263; (R1) 1.1291; More…

EUR/USD’s break of 1.1185 support confirms resumption of whole down trend from 1.2348. Intraday bias stays on the downside for 61.8% projection of 1.1908 to 1.1185 from 1.1482 at 1.1035. Break will target 100% projection at 1.0759. On the upside, above 1.1243 minor resistance will turn intraday bias neutral first. but recovery should be limited well below 1.1482 resistance to bring down trend resumption.

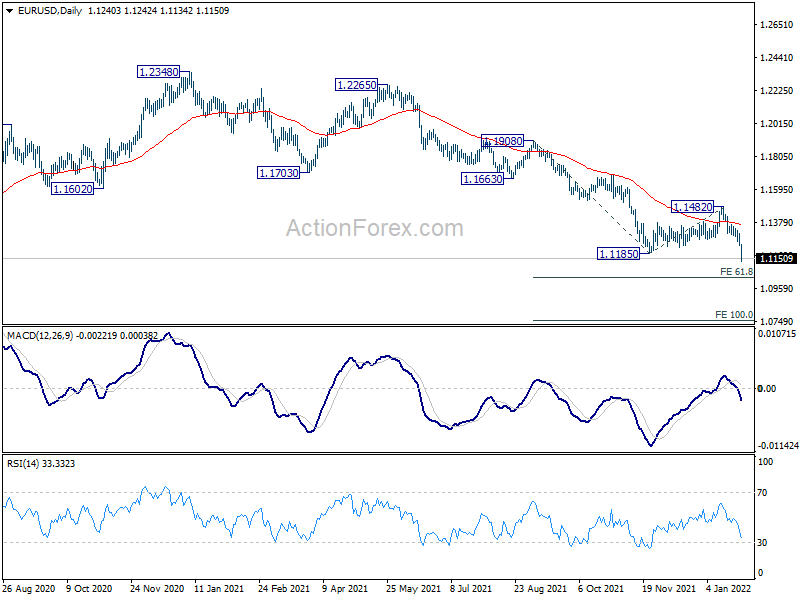

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1482 resistance holds. Next target would be 1.0635 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 1.40% | 1.20% | 2.20% | |

| 21:45 | NZD | CPI Y/Y Q4 | 5.90% | 5.60% | 4.90% | |

| 23:30 | AUD | Westpac Leading Index M/M Dec | 0.00% | 0.10% | 0.20% | |

| 00:30 | AUD | Import Price Index Q/Q Q4 | 5.80% | 1.40% | 5.40% | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Feb | -6.7 | -8 | -6.8 | -6.9 |

| 07:00 | CHF | Trade Balance (CHF) Dec | 3.69B | 5.23B | 6.16B | 6.10B |

| 13:30 | USD | Initial Jobless Claims (Jan 21) | 260K | 260K | 286K | 290K |

| 13:30 | USD | GDP Annualized Q4 P | 6.90% | 5.60% | 2.30% | |

| 13:30 | USD | GDP Price Index Q4 P | 6.90% | 6.00% | 6.00% | |

| 13:30 | USD | Durable Goods Orders Dec | -0.90% | -0.50% | 2.60% | |

| 13:30 | USD | Durable Goods Orders ex Transportation Dec | 0.40% | 0.50% | 0.90% | |

| 15:00 | USD | Pending Home Sales M/M Dec | -0.20% | -2.20% | ||

| 15:30 | USD | Natural Gas Storage | -205B | -206B |