Overall market sentiment is stable, with major Asian indexes mixed, following the recovery in US stocks overnight. Yen and Dollar soften slightly after turning into consolidations, but Swiss Franc is still strong. Commodity currencies are mixed with no follow through buying with the current rebound attempt. In other markets, Gold is struggling in tight range below 1800 handle. WTI crude oil is flip-flopping around 70 handle, with no momentum for a sustainable rebound.

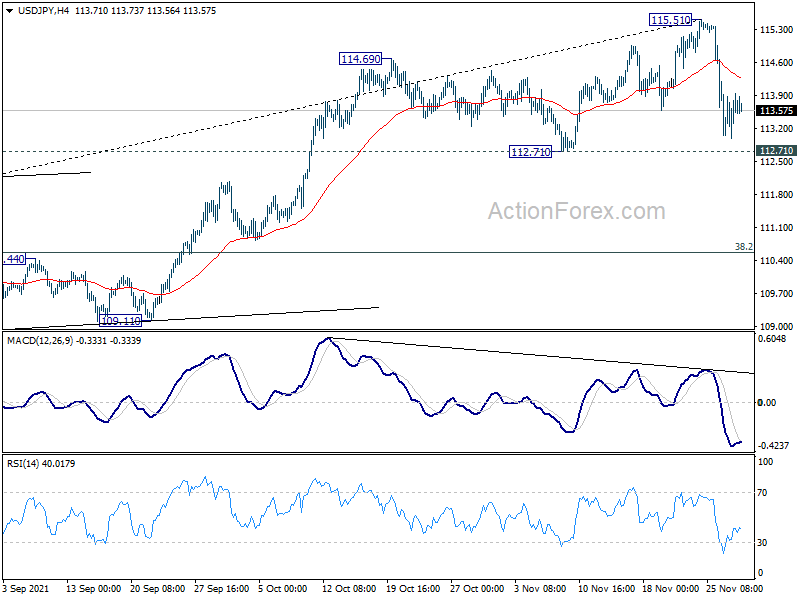

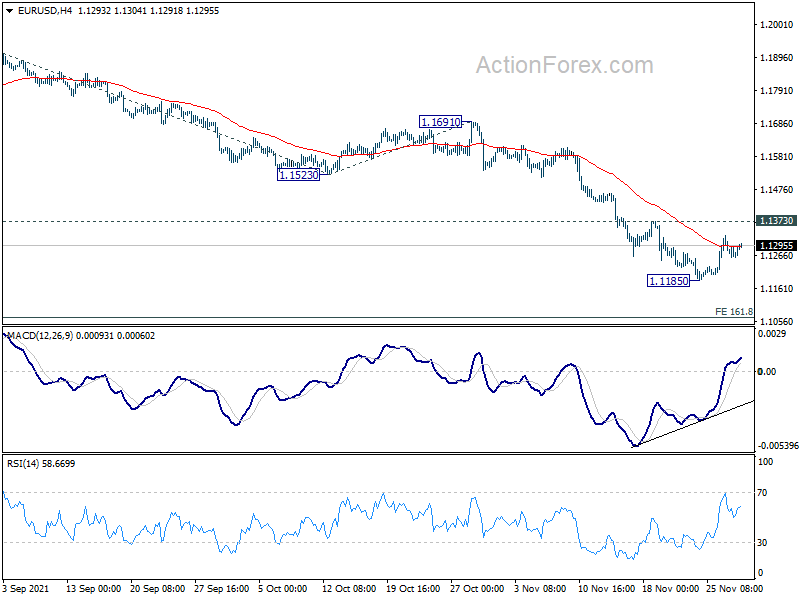

Technically, we’ll be looking at the development in both EUR/USD and USD/JPY closely. As for EUR/USD, recovery from 1.1185 remains capped below 1.1373 minor resistance, and thus keeps near term outlook bearish. However, break of 1.1373 could solidify upside momentum in Euro in crosses, in particular in EUR/GBP, EUR/CAD and EUR/AUD. Meanwhile, USD/JPY is still holding above 112.71 support. But a firm break there could prompt deeper selling in other Yen crosses.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is down -1.09%. China Shanghai SSE is up 0.23%. Singapore Strait Times is down -0.56%. Japan 10-year JGB yield is down -0.0026 at 0.072. Overnight, DOW rose 0.68%. S&P 500 rose 1.32%. NASDAQ rose 1.88%. 10-year yield rose 0.048 to 1.530.

Fed Powell: Emergence of Omicron poses downside risks to economy

In the prepared remarks for a Senate Committee hearing, Fed Chair Jerome Powell said , “the recent rise in COVID-19 cases and the emergence of the Omicron variant pose downside risks to employment and economic activity and increased uncertainty for inflation.”

“Greater concerns about the virus could reduce people’s willingness to work in person, which would slow progress in the labor market and intensify supply-chain disruptions,” he added.

Powell also reiterated, inflation is expected to “move down significantly over the next year as supply and demand imbalances abate.” However, “it now appears that factors pushing inflation upward will linger well into next year.” Also, “with the rapid improvement in the labor market, slack is diminishing, and wages are rising at a brisk pace.”

Japan industrial production rose 1.1% mom in Oct, more growth expected in Nov and Dec

Japan industrial production rose 1.1% mom in October, below expectation of 1.8% mom. That’s nonetheless the first rise in four months.

The seasonally adjusted index of production at factories and mines stood at 90.5 against the 2015 base of 100. The index of industrial shipments increased 2.0% to 88.3 while that of inventories was up 0.8% at 98.9.

The Ministry of Economy, Trade and Industry expects industrial production to grow 9.0% mom in November and then 2.1% mom in December.

Unemployment rate dropped from 2.8% to 2.7% in October, better than expectation of 2.8%.

China PMI manufacturing rose to 50.1, non-manufacturing dropped to 52.3

China official PMI Manufacturing rose from 49.2 to 50.1 in November, above expectation of 49.6. PMI Non-Manufacturing dropped from 52.4 to 52.3, below expectation of 53.0. PMI Composite rose from 50.8 to 52.2.

“A series of policy measures to ensure energy supply and stabilize market prices have borne some fruits. The tight supply of electricity eased while prices of some raw materials dropped significantly in November,” said Zhao Qinghe, a senior NBS statistician.

New Zealand ANZ business confidence finalized at -16.4 in Nov

New Zealand ANZ business confidence was finalized at -16.4 in November, down from October’s -13.4. Own activity outlook dropped from 21.7 to 15.0. Looking at some more details, export intentions rose from 8.6 to 9.5. Investment intentions rose from1 3.8 to 16.3. Employment intentions rose from 10.9 to 15.8. Cost expectations rose from 87.2 to 88.7. Pricing intentions rose from 65.5 to 66.5. Inflation expectations rose from 3.45% to 4.24%.

From Australia, private sector credit rose 0.5% mom in October, versus expectation of 0.6% mom. Building permits dropped -12.9% mom, versus expectation of -2.0% mom. Current account surplus rose to AUD 23.9B in Q3, below expectation of AUD 27.8B.

Looking ahead

France GDP, Germany unemployment, Eurozone CPI flash and Swiss KOF will be released in European session. Later in the day, Canada will also released GDP. US will release house price index, Chicago PMI and consumer confidence.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1263; (P) 1.1289; (R1) 1.1320; More…

Intraday bias in EUR/USD remains neutral as consolidation from 1.1185 is extending. With 1.1373 resistance intact, further decline is still in favor. On the downside, break of 1.1185 will resume the larger down trend to 161.8% projection of 1.1908 to 1.1523 from 1.1691 at 1.1068 next. However, firm break of 1.1373 will indicate short term bottoming and turn bias back to the upside for stronger rebound.

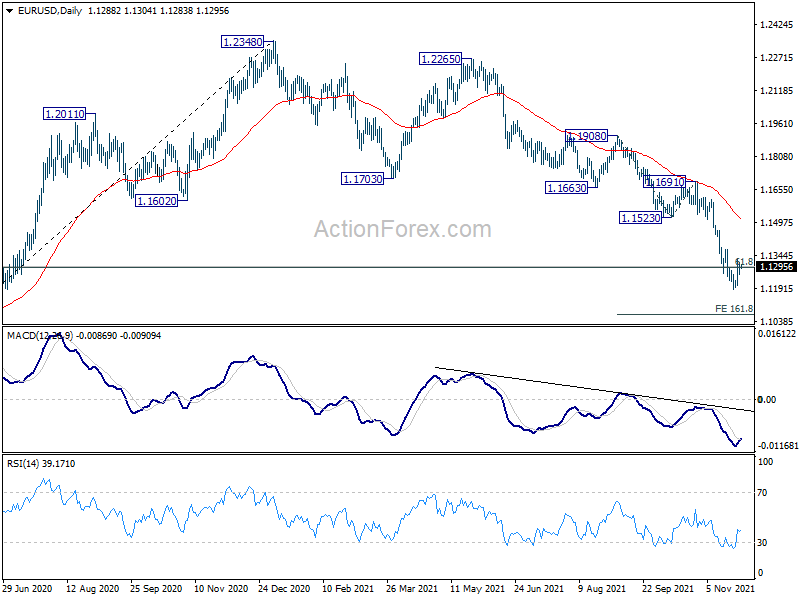

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1703 support turned resistance holds. Sustained break of 61.8% retracement of 1.0635 to 1.2348 at 1.1289 would pave the way back to 1.0635.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Oct | 2.70% | 2.80% | 2.80% | |

| 23:50 | JPY | Industrial Production M/M Oct P | 1.10% | 1.80% | -5.40% | |

| 00:00 | NZD | ANZ Business Confidence Nov F | -16.4 | -18.1 | ||

| 00:30 | AUD | Current Account Balance (AUD) Q3 | 23.9B | 27.8B | 20.5B | 22.9B |

| 00:30 | AUD | Private Sector Credit M/M Oct | 0.50% | 0.60% | 0.60% | |

| 00:30 | AUD | Building Permits M/M Oct | -12.90% | -2.00% | -4.30% | -3.90% |

| 01:00 | CNY | Manufacturing PMI Nov | 50.1 | 49.6 | 49.2 | |

| 01:00 | CNY | Non-Manufacturing PMI Nov | 52.3 | 53 | 52.4 | |

| 05:00 | JPY | Housing Starts Y/Y Oct | 5.20% | 4.30% | ||

| 07:45 | EUR | France Consumer Spending M/M Oct | 0.30% | -0.20% | ||

| 07:45 | EUR | France GDP Q/Q Q3 | 3.00% | 3.00% | ||

| 08:00 | CHF | KOF Leading Indicator Nov | 109 | 110.7 | ||

| 08:55 | EUR | Germany Unemployment Change Nov | -20K | -39K | ||

| 08:55 | EUR | Germany Unemployment Rate Nov | 5.40% | |||

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | 4.40% | 4.10% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov P | 2.30% | 2.00% | ||

| 13:30 | CAD | GDP M/M Sep | 0.10% | 0.40% | ||

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Sep | 20.00% | 19.70% | ||

| 14:00 | USD | Housing Price Index M/M Sep | 1.20% | 1.00% | ||

| 14:45 | USD | Chicago PMI Nov | 67.2 | 68.4 | ||

| 15:00 | USD | Consumer Confidence Nov | 110.8 | 113.8 |