Yen extended rebound in European session following the sharp fall in benchmark Germany yield. But struggling to extend gain as markets enter into US session. Overall markets are mixed as investors are probably turning cautious ahead tomorrow’s FOMC policy decision. As for today, Aussie remains the worst performing one after post RBA selloff, followed by Kiwi, and Swiss Franc. On the other hand, Yen is strongest, followed by Dollar and then Euro.

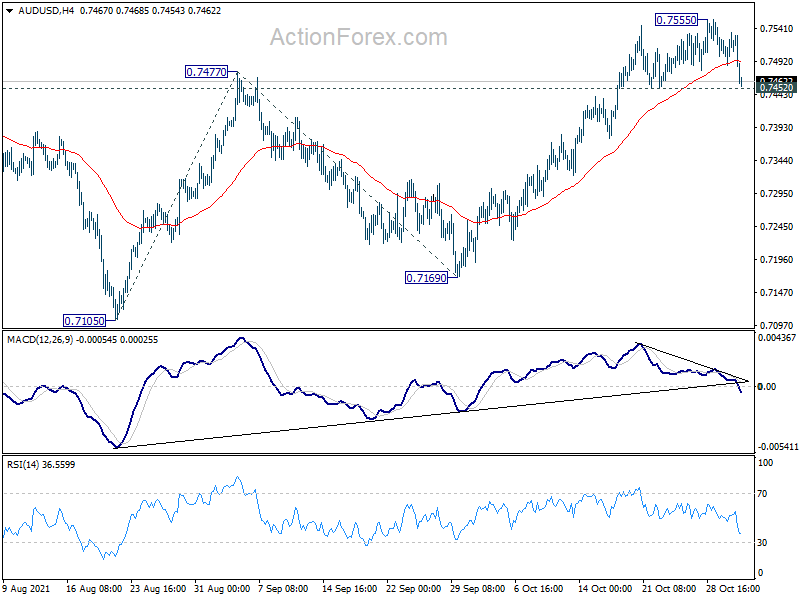

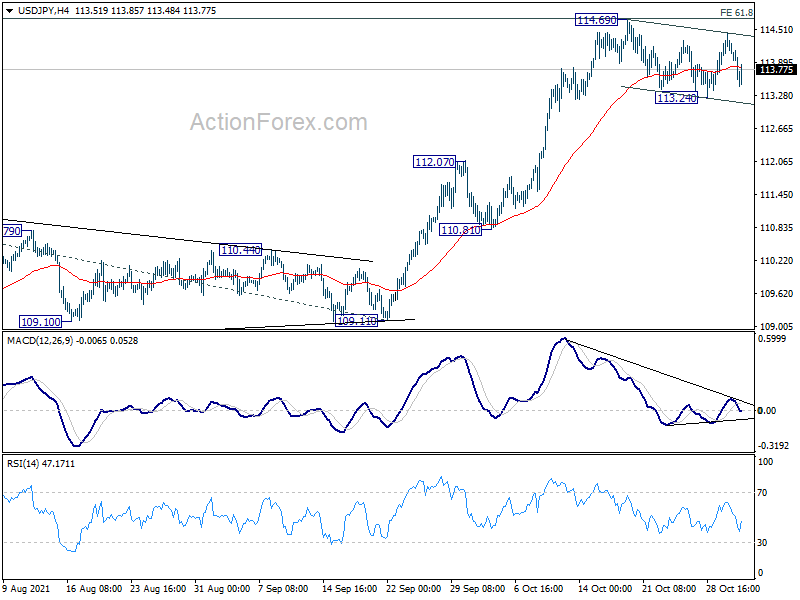

Technically, we’d pay attention to whether Aussie’s selloff would extend further. AUD/USD is currently pressing 0.7452 minor support while AUD/JPY is pressing 84.59. Break of these levels will extend the near term correction lower. However, rebound from current levels would keep the consolidations brief, with breaks of 0.7555 and 86.24 highs sooner rather than later.

In Europe, at the time of writing, FTSE is down -0.52%. DAX is up 0.70%. CAC is up 0.27%. Germany 10-year yield is down -0.047 at -0.146. Earlier in Asia, Nikkei dropped -0.43%. Hong Kong HSI dropped -0.22%. China Shanghai SSE dropped -1.10%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield dropped -0.0125 to 0.084.

Eurozone PMI manufacturing finalized at 58.3, worsening supply chain situation

Eurozone PMI Manufacturing was finalized at 58.3 in October, slightly down from September’s 58.6. But that’s still the lowest level since February. Readings of individual states remained generally strong: Netherlands at 62.5, Ireland at 62.1, Italy at 61.1, Austria at 60.0, Greece at 58.9, Germany at 57.8. Spain at 57.4, France at 53.6.

Chris Williamson, Chief Business Economist at IHS Markit said: “Eurozone manufacturers reported a worsening of the supply chain situation in October, which curbed production growth sharply during the month… These shortages have… pushed inflationary pressures to new survey highs, raising further questions about just how transitory the recent spike in inflation will be. Business confidence also lost some ground to hit a one-year low in October, as increasing numbers of producers grew concerned about the supply situation and the impact of rising costs and prices, adding to the indications that manufacturers face some challenging months ahead.”

Germany PMI Manufacturing was finalized at 57.8 in October, down from September’s 58.4, lowest level in nine months. Markit said that material shortages restrained output and new orders. Surging input costs drove record rise in factory gate charges. There was further slowdown in job creation as optimism waned.

France PMI Manufacturing was finalized at 53.6 in October, down from September’s 55.0, hitting the lowest level since January. Markit said output level declined as firms struggled to secure necessary materials. Demand conditions showed signs of weakening amid supply constraints. Lead times lengthened at near-record pace and cost inflation were at decade high.

Swiss CPI rose to 1.2% yoy in Oct, retail sales rose 2.5% yoy in Sep

Swiss CPI came in at 0.3% mom, 1.2% yoy in October, above expectation of 0.1% mom, 1.1% yoy. Annual rate also accelerated from September’s 0.9% yoy. The 0.3% increase compared with the previous month is due to several factors including rising prices for heating oil. Gas also recorded a price increase, as did fuel. In contrast, prices for salads and fruiting vegetables decreased.

Retail sales rose 2.5% yoy in September, above expectation of 1.4% yoy.

RBA abandons yield curve control, hints on earlier hike

RBA kept cash rate target unchanged at 0.10% as widely expected today. The asset purchase program, however, will continue at AUD 4B per week until at least February 2022. However, without much surprise, it discontinue 0.10% target for April 2024 government bonds, effectively abandoning yield curve control.

As for forward guidance, RBA maintain that cash rate won’t be raised until actual inflation is “sustainably within the 2 to 3 per cent target range”. But now, it forecasts inflation to be no higher than 2.50% at the end of 2023, hinting that rate hike could come earlier than that.

In the new economic projection, RBA expects GDP growth to b 3% in 2021, 5.50% in 2022, and 2.50% in 2023. Unemployment rate is expected to trend lower to 4.25% at the end of 2022 and 4.00% at the end of 2023. Inflation is projected to be at 2.25% over 2021 and 2022, and pick up to 2.20% over 2023.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.81; (P) 114.13; (R1) 114.31; More…

USD/JPY is staying in range of 113.24/114.69 and intraday bias remains neutral first. On the upside, firm break of 114.69 will resume the larger up trend to 100% projection of 102.58 to 111.65 from 109.11 at 118.18 next. Break of 113.24 will bring deeper pull back, but downside should be contained above 112.07 resistance turned support to bring rebound.

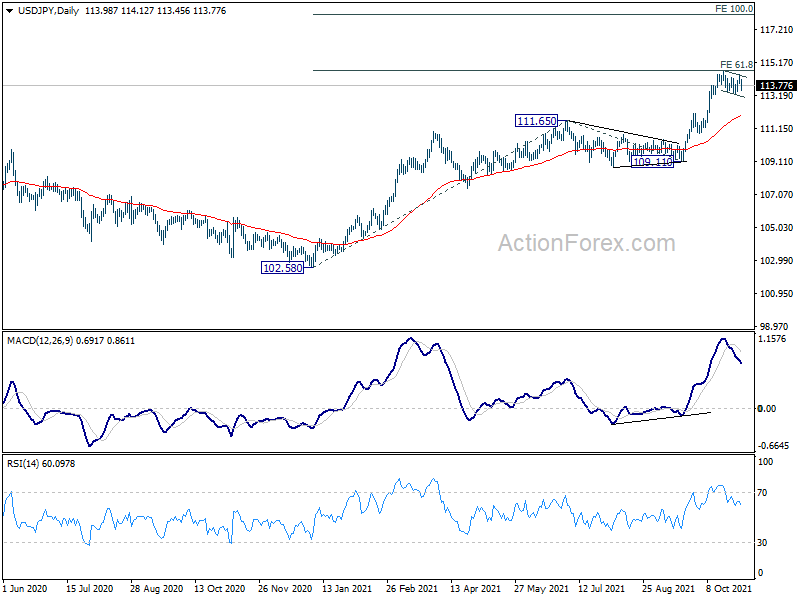

In the bigger picture, corrective decline from 118.65 (2016 high) should have completed at 101.18 already. Rise from the 102.58 is seen as the third leg of the up trend from 101.18. Next target is 114.54 resistance and then 118.65 high. This will now be the preferred case as long as 109.11 support hold, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Sep | -1.90% | 3.80% | ||

| 23:50 | JPY | Monetary Base Y/Y Oct | 9.90% | 12.30% | 11.70% | |

| 23:50 | JPY | BoJ Minutes | ||||

| 03:30 | AUD | RBA Rate Decision | 0.10% | 0.10% | 0.10% | |

| 07:30 | CHF | Real Retail Sales Y/Y Sep | 2.50% | 1.40% | 0.50% | 0.80% |

| 07:30 | CHF | CPI M/M Oct | 0.30% | 0.10% | 0.00% | |

| 07:30 | CHF | CPI Y/Y Oct | 1.20% | 1.10% | 0.90% | |

| 08:45 | EUR | Italy Manufacturing PMI Oct | 61.1 | 59.7 | 59.7 | |

| 08:50 | EUR | France Manufacturing PMI Oct F | 53.6 | 53.5 | 53.5 | |

| 08:55 | EUR | Germany Manufacturing PMI Oct F | 57.8 | 58.2 | 58.2 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Oct F | 58.3 | 58.5 | 58.5 | |

| 12:30 | CAD | Building Permits M/M Sep | 4.30% | 2.20% | -2.10% |