Dollar’s rally continues to make progress, one step at a time. Solid job report overnight helped lift the greenback through near term resistance against Euro and Yen. Nevertheless, reaction in stocks were subdued. Focus will now turn to ISM manufacturing today for more inspirations. Meanwhile, commodity currencies and Swiss Franc are currently the weakest for the weak. In particular, Aussie is shrugging off some solid manufacturing and trade data.

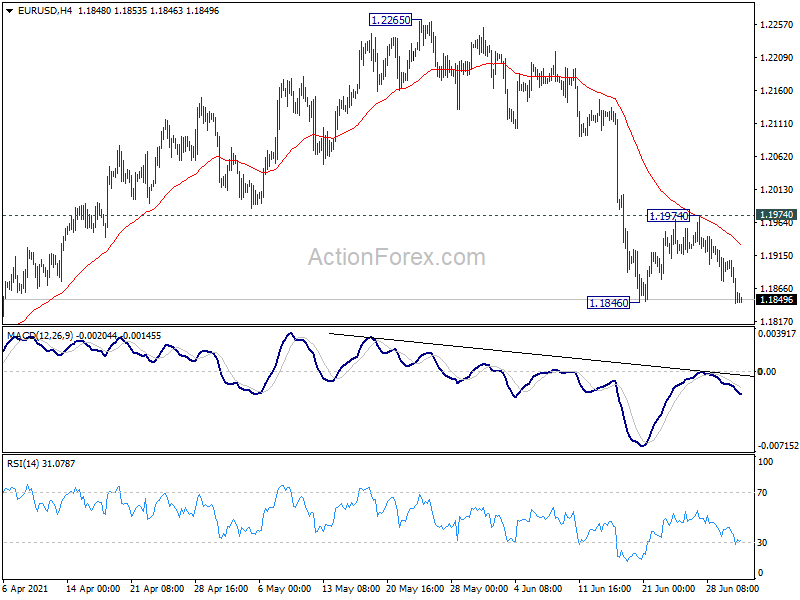

Technically, EUR/USD’s breach of 1.1846 suggests fall resumption towards 1.1703 support. USD/JPY also breaks 111.10 resistance to resume recent rally. Focus now turns to 0.7476 support in AUD/USD and 1.3785 support in GBP/USD. Break of these level should seal the case for more rally in Dollar. NZD/USD could also take on 0.6921 support soon. Break there will resume whole corrective pattern from 0.7463 to 100% projection of 0.7463 to 0.6942 from 0.7315 at 0.6794.

In Asia, at the time of writing, Nikkei is down -0.44%. Hong Kong and China are on holiday. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is down -0.0091 at 0.050. Overnight, DOW rose 0.61%. S&P 500 rose 0.13%. NASDAQ dropped -0.17%. 10-year yield dropped -0.037 to 1.443.

Australia trade surplus widened to AUD 9.68B, AiG manufacturing rose to record 63.2

Australia goods and services exports rose 6% mom or AUD 2443m to AUD 42.23B in May. Goods and services rose 3% mom or AUD 919m to AUD 32.55B. Trade surplus widened to AUD 9.68B, up from AUD 8.16B, smaller than expectation of AUD 10.50B.

AiG Performance of Manufacturing Index rose to new record high at 63.2 in June, up from 61.8. That’s also the ninth consecutive month of rise. Looking at some more details, production dropped -3.8 to 60.7. Employment dropped -1.0 to 60.3. New orders jumped 5.7 to 70.6. Supplier deliveries rose 6.7 to 58.3. Exports rose 11.3 to 60.2. Input prices dropped -3.3 to 78.8. Selling prices rose 5.3 to 63.6.

Japan Tankan large manufacturing rose index to 14 in Q2, highest since 2018

Japan Tankan large manufacturing index rose to 14 in Q2, up from 5, missed expectation of 15. That’s the best level since 2018, and the fourth straight quarter of improvement. Large manufacturing output rose to 13, up from 4, below expectation of 18. Non-manufacturing index rose to 1, up from -1, below expectation of 3. Non-manufacturing outlook rose to 3, up from -1, missed expectation of 8. Large all industry capex rose 9.6%, above expectation of 7.2%.

“Exports and output continue to improve, which is helping sentiment improve for most manufacturing sectors. The auto sector, however, saw sentiment worsen due to shortages in semiconductor chips,” a BOJ official said at a briefing.

Japan PMI manufacturing finalized at 52.4 in June, strong optimism

Japan PMI Manufacturing was finalized at 52.4 in June, down from May’s 53.0. Markit said output and new orders both rose at softest rates for five months. Input prices rose at fastest pace in over 10 years. Optimism was strongest on record.

Usamah Bhatti, Economist at IHS Markit, said: “Japanese manufacturers commented that the degree of optimism regarding the outlook for output over the coming 12 months strengthened in June. Confidence about the outlook reached the highest level since the series began in July 2012, as hopes of an end to the pandemic gathered pace. This is broadly in line with the IHS Markit forecast for industrial production to grow 8.8% in 2021, though this does not fully recoup losses from the pandemic.”

China Caixin PMI manufacturing dropped to 51.3, gradually returned to normal

China Caixin PMI Manufacturing dropped to 51.3 in June, down from 52.0, below expectation of 51.8. Markit noted increase in output was softest for 15 months. Total new order growth slowed as export sales stagnated. Employment continued to inc rea sew while cost pressures eased.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, the manufacturing sector continued to stably expand in June, despite the impact of the pandemic…. The manufacturing sector has gradually returned to normal. In the second half of this year, the low base effect from last year will weaken. Inflationary pressure, coupled with the economic slowdown, is still a serious challenge for China.”

Looking ahead

The economic calendar is rather busy today. To be featured in European session include Germany retail sales; Swiss retail sales, CPI and PMI; Eurozone PMI manufacturing final and unemployment rate; and UK PMI manufacturing final.

Later in the day, US will release jobless claims, ISM manufacturing and construction spending.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1834; (P) 1.1871; (R1) 1.1898; More…

EUR/USD’s breach of 1.1846 support suggests that fall from 1.2265 is resuming. Intraday bias is back on the downside, such fall is seen as the third leg of the consolidation pattern from 1.2348. Deeper decline would be seen back to 1.1703 support. On the upside, break of 1.1974 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

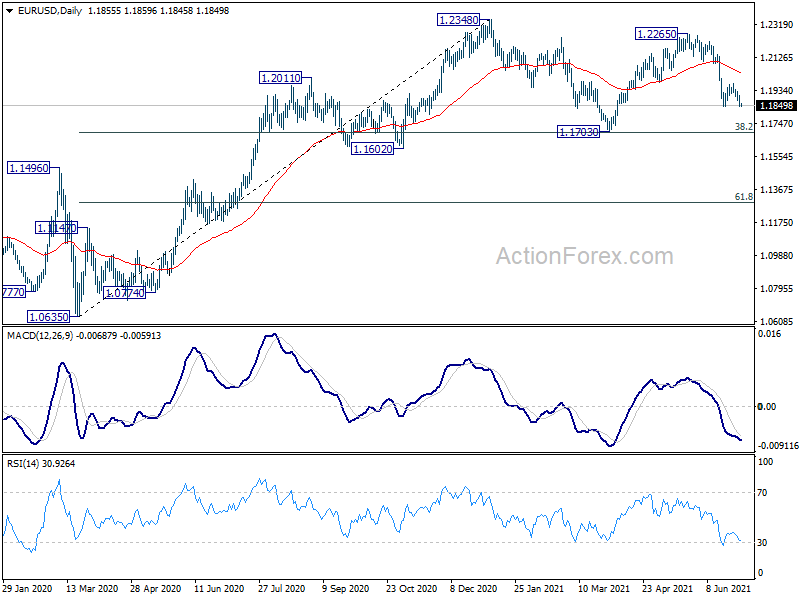

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair. However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Mfg Index Jun | 63.2 | 61.8 | ||

| 22:45 | NZD | Building Permits M/M May | -2.80% | 4.80% | 5.10% | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 14 | 15 | 5 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | 13 | 18 | 4 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q2 | 1 | 3 | -1 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q2 | 3 | 8 | -1 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 9.60% | 7.20% | 3.00% | |

| 00:30 | JPY | Manufacturing PMI Jun F | 52.4 | 51.5 | 51.5 | |

| 01:30 | AUD | Trade Balance (AUD) May | 9.68B | 10.50B | 8.03B | 8.16B |

| 01:45 | CNY | Caixin Manufacturing PMI Jun | 51.3 | 51.8 | 52 | |

| 06:00 | EUR | Germany Retail Sales M/M May | 5.00% | -5.50% | ||

| 06:30 | CHF | Real Retail Sales Y/Y May | 35.70% | |||

| 06:30 | CHF | CPI M/M Jun | 0.20% | 0.30% | ||

| 06:30 | CHF | CPI Y/Y Jun | 0.70% | 0.60% | ||

| 07:30 | CHF | SVME PMI Jun | 70.2 | 69.9 | ||

| 07:45 | EUR | Italy Manufacturing PMI Jun | 62.2 | 62.3 | ||

| 07:50 | EUR | France Manufacturing PMI Jun F | 58.6 | 58.6 | ||

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 64.9 | 64.9 | ||

| 08:00 | EUR | Italy Unemployment May | 10.70% | 10.70% | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 63.1 | 63.1 | ||

| 08:30 | GBP | Manufacturing PMI Jun | 64.2 | 64.2 | ||

| 09:00 | EUR | Eurozone Unemployment Rate May | 8.00% | 8.00% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Jun | -93.80% | |||

| 12:30 | USD | Initial Jobless Claims (Jun 25) | 382K | 411K | ||

| 13:45 | USD | Manufacturing PMI Jun F | 62.6 | 62.6 | ||

| 14:00 | USD | ISM Manufacturing PMI Jun | 61.5 | 61.2 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 89.8 | 88 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 50.9 | |||

| 14:00 | USD | Construction Spending M/M May | 0.40% | 0.20% | ||

| 14:30 | USD | Natural Gas Storage | 55B |