Yen trades broadly overnight on strong risk appetite, with NASDAQ and S&P 500 closing at new record highs. And it remains generally soft in Asian session. Some selling in seen in Australian Dollar after RBA minutes, but loss is very limited. Other commodity currencies are indeed trying to firm up, which helps floor the Aussie. Meanwhile, Dollar and Swiss Franc are soft together with Yen too.

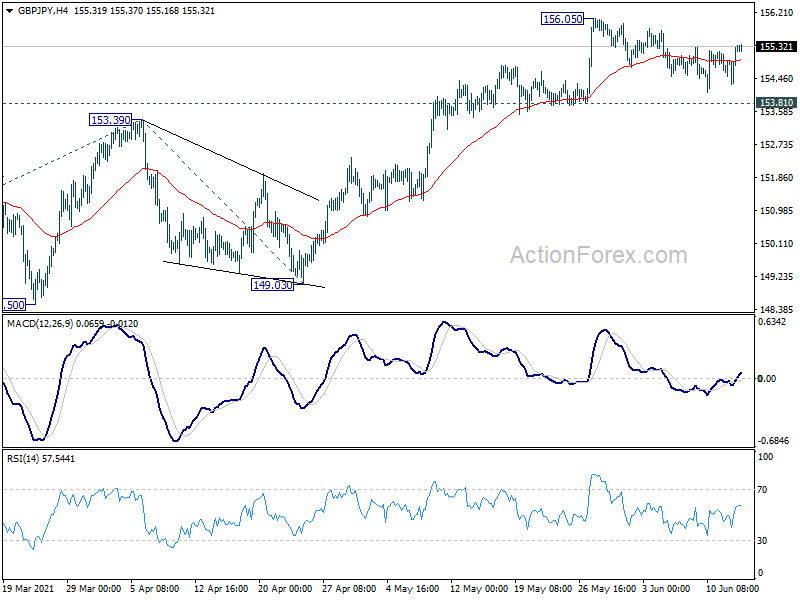

Technically, a focus now is on whether the up trend in stocks would extended and even accelerate, and the subsequent reactions in Yen. EUR/JPY and GBP/JPY rebounded comfortably ahead of 132.51 and 153.81 support levels respectively. Both crosses might now be heading back to 134.11 and 156.05 highs. Break there will resume medium term up trends.

In Asia, at the time of writing, Nikkei is up 1.00%. Hong Kong HSI is down -0.76%. China Shanghai SSE is down -0.90%. Singapore Strait Times is up 0.77%. Japan 10-year JGB yield is up 0.0048 at 0.045. overnight, DOW dropped -0.25%. SP500 rose 0.18%. NASDAQ rose 0.74%. 10-year yield rose 0.039 to 1.501.

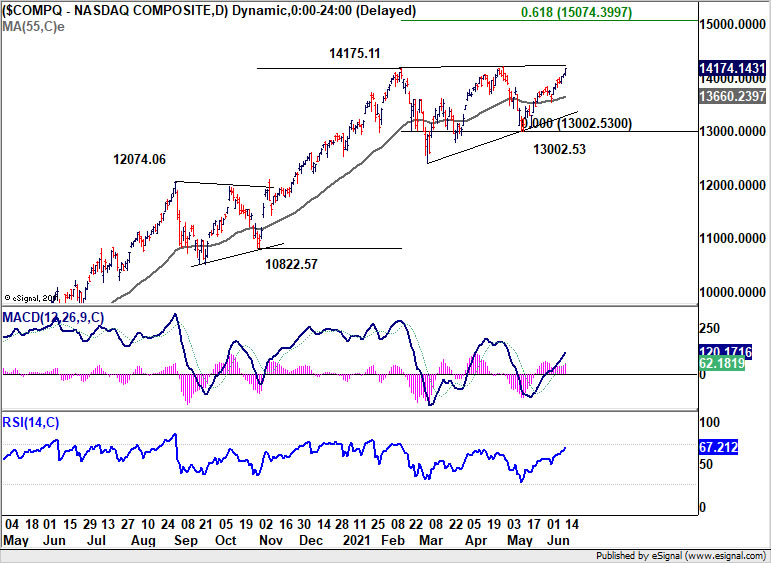

NASDAQ closed at record, heading to 15000 next

Both NASDAQ and S&P 500 closed at new record highs overnight. NASDAQ’s consolidation form 14175.11 should have completed at 13002.52, and the long term up trend should be resuming. Based on yesterday’s strong close, buying momentum might accelerate further this week, subject to reactions to FOMC statement and projections. We’re now looking at next medium term target at 61.8% projection of 10822.57 to 14175.11 from 13002.53 at 15074.39. In any case, outlook will stay bullish as long as 55 day EMA (now at 13660.23) holds.

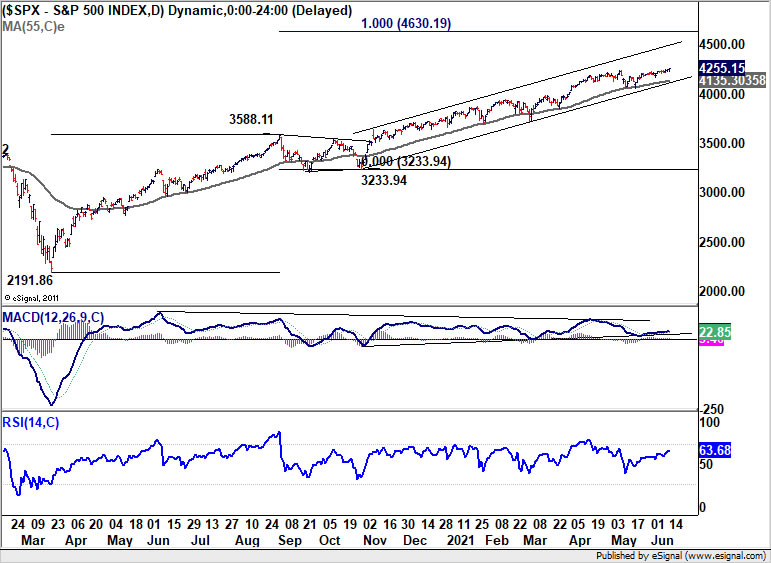

As for S&P 500, it’s staying healthily in medium term up trend, well inside channel and above rising 55 day EMA. Outlook will also stay bullish as long as 55 day EMA (now at 4135.30) holds. Next target is 100% projection of 2191.86 to 3588.11 from 3233.94 at 4630.19.

RBA discussed four options on bond purchases

RBA reiterated in the June minutes that it will make the decision on 3-year yield target and government bond purchase program at the July meeting. It emphasize “a return to full employment as a priority for monetary policy that would assist with achieving the inflation target”.

It will consider whether to extend the 3-year yield target from April 2024 bond to November 2024 bond. A key considering would be the prospect of having inflation sustainably within the 2-3% target rate some time in 2024.

Four options regarding future bond purchases after completion of the second AUD 100B of purchases in early September were discussed. The options included ceasing the purchases, repeating the AUD 100 purchases for another 6 months, scaling back the amount or spreading over a longer period, and moving to an approach where pace of purchases is reviewed more frequently.

Also from Australia, house price index rose 5.4% qoq in Q1, slightly below expectation of 5.5% qoq.

Looking ahead

UK employment data, Germany CPI, Eurozone trade balance and Swiss SECO economic forecasts will be released in European session. Major focuses will be on the batch of US data, including retail sales, PPI, Empire state manufacturing, industrial production, business inventories and NAHB housing index.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 154.62; (P) 154.99; (R1) 155.64; More…

GBP/JPY rebounds notably but stays below 156.05 resistance. Intraday bias remains neutral first. Further rise is in favor with 153.81 support intact. On the upside, break of 156.05 will resume larger up trend for 61.8% projection of 133.03 to 153.39 from 149.03 at 161.61. On the downside, firm break of 153.81 will indicate short term topping and turn bias back to the downside for deeper pull back, to 55 day EMA (now at 152.88) first.

In the bigger picture, rise from 123.94 is seen as the third leg of the pattern from 122.75 (2016 low). Focus is now on 156.59 resistance (2018 high). Sustained break there should confirm long term bullish trend reversal. Next target is 61.8% retracement of 195.86 (2015 high) to 122.75 at 167.93. On the downside, break of 149.03 support is needed to be the first sign of completion of the rise from 123.94. Otherwise, outlook will remain bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | House Price Index Q/Q Q1 | 5.40% | 5.50% | 3.00% | |

| 1:30 | AUD | RBA Minutes | ||||

| 4:30 | JPY | Tertiary Industry Index M/M Apr | -0.40% | 1.10% | ||

| 6:00 | GBP | Claimant Count Change May | -15.1K | |||

| 6:00 | GBP | Claimant Count Rate May | 7.20% | |||

| 6:00 | GBP | ILO Unemployment Rate (3M) Apr | 4.70% | 4.80% | ||

| 6:00 | GBP | Average Earnings Excluding Bonus 3M/Y Apr | 5.30% | 4.60% | ||

| 6:00 | GBP | Average Earnings Including Bonus 3M/Y Apr | 4.90% | 4.00% | ||

| 6:00 | EUR | Germany CPI M/M May F | 0.50% | 0.50% | ||

| 6:00 | EUR | Germany CPI Y/Y May F | 2.50% | 2.50% | ||

| 7:00 | CHF | SECO Economic Forecasts | ||||

| 9:00 | EUR | Eurozone Trade Balance (EUR) Apr | 15.2B | 13.0B | ||

| 12:15 | CAD | Housing Starts s.a Y/Y May | 271K | 269K | ||

| 12:30 | USD | Empire State Manufacturing Index Jun | 22.5 | 24.3 | ||

| 12:30 | USD | Retail Sales M/M May | -0.40% | 0.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M May | 0.50% | -0.80% | ||

| 12:30 | USD | PPI M/M May | 0.60% | 0.60% | ||

| 12:30 | USD | PPI Y/Y May | 6.40% | 6.20% | ||

| 12:30 | USD | PPI Core M/M May | 0.50% | 0.70% | ||

| 12:30 | USD | PPI Core Y/Y May | 3.70% | 4.10% | ||

| 13:15 | USD | Industrial Production M/M May | 0.70% | 0.70% | ||

| 13:15 | USD | Capacity Utilization May | 75.10% | 74.90% | ||

| 14:00 | USD | Business Inventories Apr | -0.10% | 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Jun | 83 | 83 |