Canadian Dollar rises in early US session after stronger than expected retail sales data. Sterling is also firm after strong PMIs. But Euro had little reaction to the solid PMI data. Instead, the common currency seems to be reacting to ECB President Christine Lagarde’s comment that accommodative policies remain necessary for months to come. Euro is currently the weakest one for today, followed by Swiss Franc, and then Dollar.

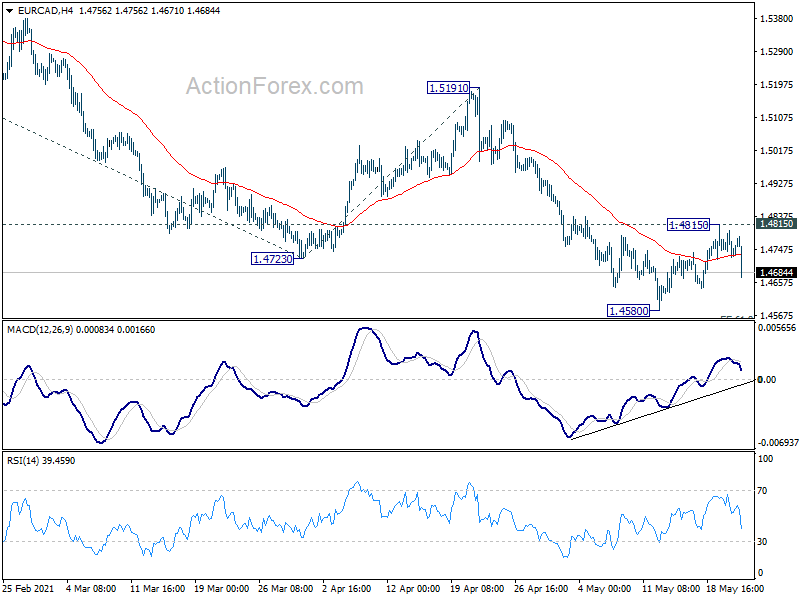

Technically, EUR/CAD’s sharp fall suggests that recovery from 1.4580 has completed, even though it was slightly stronger than expected. Focus is now back on 1.4580 low. Break will resume larger down trend. USD/CAD is also back under pressure, and sustained trading below 1.2061 cluster support will carry larger bearish implications. Deeper fall could then seen in USD/CAD for 1.1816 projection level next.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is up 0.33%. CAC is up 0.51%. Germany 10-year yield is down -0.026 at -0.131. Earlier in Asia, Nikkei rose 0.78%. Hong Kong HSI rose 0.03%. China Shanghai SSE dropped -0.58%. Singapore Strait Times rose 0.26%. Japan 10-year JGB yield dropped -0.001 to 0.083.

Canada retail sales rose 3.6% mom in March, up in 10 of 11 subsectors

Canada retail sales rose 3.6% mom in March, to CAD 57.6B, above expectation of 2.3% mom. Ex-auto sales rose 4.3% mom, above expectation of 4.0% mom too. Sales increased in 10 of 11 subsectors, representing 79.1% of retail trade. For Q1, sales were up 1.8%, the third quarterly increase.

Advance estimates indicates that retail sales dropped -5.1% mom in April. This unofficial estimate was calculated based on responses received from 46% of companies surveyed.

Eurozone PMI composite rose to 56.9, a 39-month high

Eurozone PMI Manufacturing edged down to 62.8 in May, down from 62.9, above expectation of 62.4. But PMI Services surged to 55.1, up from 50.2, above expectation of 52.0, a 35-month high. PMI Composite rose to 56.9, up from 53.8, a 39-month high.

Chris Williamson, Chief Business Economist at IHS Markit said: “Demand for goods and services is surging at the sharpest rate for 15 years across the eurozone as the region continues to reopen from covid-related restrictions. Virus containment measures have been eased in May to the lowest since last October, facilitating an especially marked improvement in service sector business activity, which has been accompanied by yet another near-record expansion of manufacturing.

“Growth would have been even stronger had it not been for record supply chain delays and difficulties restarting businesses quickly enough to meet demand, especially in terms of re-hiring. The shortfall of business output relative to demand is running at the highest in the survey’s 23-year history.

“This imbalance of supply and demand has put further upward pressure on prices. How long these inflationary pressures persist will depend on how quickly supply comes back into line with demand, but for now the imbalance is deteriorating, resulting in the highest-ever price pressures for goods recorded by the survey and rising prices for services.”

France PMI Manufacturing rose to 59.2 in May, up from 58.9, above expectation of 59.2. PMI Services surged to 56.6, up from 50.3, above expectation of 53.0. PMI Composite rose to 57.0, up from 51.6, hitting a 10-month high.

Germany PMI Manufacturing dropped -64.0 in May, down from 66.2, below expectation of 65.8. PMI Services jumped to 52.8, up from 49.9, above expectation of 52.0. PMI Composite rose to 56.2, up from 55.8.

Bundesbank: German services second should increase again significantly

Germany’s Bundesbank said in its monthly report, “as soon as the corona protective measures are gradually loosened, activity in the service areas affected should increase again significantly.”

Also, “as in the summer quarter of 2020, private consumption should recover quickly as soon as the restrictions are broadly and sustainably withdrawn”.

“The industry is benefiting from strong demand, even if production is likely to be slowed down by bottlenecks in preliminary products in the near future,” it added.

UK PMI composite rose to new record, an unprecedented growth spurt

UK PMI Manufacturing jumped to 66.1 in May, up from 60.9, well above expectation of 60.0. That’s another record high since 1992. PMI Services rose to 61.8, up from 61.0, below expectation of 62.0. But that’s still a 91-month high. PMI Composite Rose to 62.0, up from 60.7, record high since 1998.

Chris Williamson, Chief Business Economist at IHS Markit, said: “The UK is enjoying an unprecedented growth spurt as the economy reopens. Factory orders are surging at a record pace as global demand for goods continues to revive, and the service sector is reporting near-record growth as the opening up of the economy allows more businesses to trade. Business confidence has meanwhile hit an all-time high as concerns about the impact of the pandemic continue to fade…

“A direct consequence of demand running ahead of supply was a steep rise in prices, hinting strongly that consumer price inflation has much further to rise after lifting to 1.5% in April. However, the inflationary spike could prove temporary, as many of the price hikes have reflected surcharges on shipping and other shortage-related issues emanating from the pandemic. As these constraints ease, price pressures should abate, but there remains a great deal of uncertainty as to how long it will take for global business and trade to return to normal functioning, especially if new virus variants appear.”

UK retail sales jumped 9.2% mom in Apr on re-opening

UK retail sales grew sharply by 9.2% mom in April, well above expectation of 4.0% mom. Ex-fuel sales jumped 9.0% om, also above expectation of 4.0% mom. The strong growth reflected effect of easing of coronavirus restrictions, including the re-opening of all non-essential retail from 12 April in England and Wales and from 26 April in Scotland.

Japan CPI core unchanged at -0.1% yoy, CPI core-core turned negative to -0.2% yoy

Japan CPI core (all item less fresh food), was unchanged at -0.1% yoy in April, better than expectation of -0.2% yoy. Headline all item CPI dropped to -0.4% yoy, down from -0.2% yoy. CPI core-core (all item ex fresh food and energy), turned negative to -0.2% yoy, down form 0.3% yoy.

Nevertheless, analysts saw the drop in inflation as being almost entirely due to the -26.5% plunge in mobile phone charges. That already lowed -0.5% off core CPI.

Japan PMI composite back in contraction, but firms not discouraged by virus resurgence

Japan PMI manufacturing dropped to 52.5 in May, down from 53.6, below expectation of 53.8. PMI Services dropped notably to 45.7, down from 49.5. PMI Composite dropped to 48.1, down from 51.0, back in contraction again.

Usamah Bhatti, Economist at IHS Markit, said: “Flash PMI data indicated that activity at Japanese private sector businesses saw a renewed reduction in May. Output fell at the quickest pace for four months, while the contraction in new business inflows was the fastest since February. Survey members widely attributed the deterioration in business conditions to a resurgence in COVID-19 cases and the reimposition of state of emergency measures.

“Positively, private sector firms were not discouraged from further increasing capacity, as employment levels rose for the fourth consecutive month. This was despite another sharp rise in input costs across the Japanese private sector.

“Disruption to short-term activity is likely to remain until the latest wave of COVID-19 infections passes and restrictions enacted under state of emergency laws are lifted. However, Japanese private sector companies were optimistic that business conditions would improve in the year ahead, albeit to a lesser extent than that seen in April. Positive sentiment stemmed from the expectation that the currently sluggish vaccine rollout would gather pace and aid in the submission of the pandemic, in turn triggering a recovery in demand in both domestic and external markets.”

Australia PMI manufacturing hit another record, services edged down

Australia PMI Manufacturing rose to 59.9 in May, up from 59.7, hitting another record high since May 2016. PMI Services dropped to 58.2, down from 58.8. PMI Composite also dropped slightly to 58.1, down from 58.9.

Jingyi Pan, Economics Associate Director at IHS Markit, said: “Australia’s private sector growth eased from April’s survey record. That said, growth remained sharp to affirm the continued improvement in economic conditions following the easing of COVID-19 restrictions.

“Export orders notably continued to improve, reflecting the robust external demand despite concerns of rising COVID-19 cases in the region. In turn, this filtered through to the labour market with employment improving at the fastest pace in the survey’s five-year history.

“The outlook for activity over the coming year remained optimistic, particularly in the service sector in May. Ongoing supply-chain disruptions, however, continued to impact private sector firms, pushing up input cost inflation and thereby output prices.”

Australia retail sales rose 1.1%, or AUD 350.2m, in April, above expectation of 0.5% mom. Annually, sales rose 25.1% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2187; (P) 1.2208; (R1) 1.2247; More….

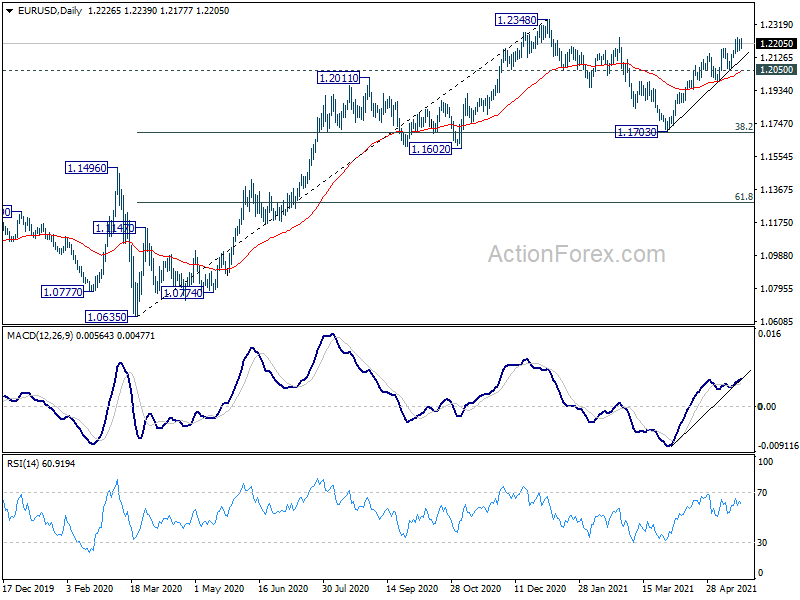

EUR/USD failed to break through 1.2244 temporary top and retreats notably. Intraday bias remains neutral and further rise is still expected as long as 1.2050 support holds. On the upside, break of 1.2244 will target a test on 1.2348 high. Decisive break there should confirm resumption of up trend from 1.0635. Next target is 1.2555 key long term resistance zone. However, break of 1.2050 will delay the bullish case. Intraday bias will be turned back to the downside to extend the consolidation pattern from 1.2348 with another falling leg.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI May P | 59.9 | 59.7 | ||

| 23:00 | AUD | Services PMI May P | 58.2 | 58.8 | ||

| 23:01 | GBP | GfK Consumer Confidence May | -9 | -13 | -15 | |

| 23:30 | JPY | National CPI Core Y/Y Apr | -0.10% | -0.20% | -0.10% | |

| 00:30 | JPY | Manufacturing PMI May P | 52.5 | 53.8 | 53.6 | |

| 01:30 | AUD | Retail Sales M/M Apr P | 1.10% | 0.50% | 1.30% | |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Apr | 9.00% | 4.00% | 4.90% | 4.60% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Apr | 37.70% | 31.40% | 7.90% | |

| 06:00 | GBP | Retail Sales M/M Apr | 9.20% | 4.00% | 5.40% | 5.10% |

| 06:00 | GBP | Retail Sales Y/Y Apr | 42.40% | 36.50% | 7.20% | |

| 07:15 | EUR | France Manufacturing PMI May P | 59.2 | 58.1 | 58.9 | |

| 07:15 | EUR | France Services PMI May P | 56.6 | 53 | 50.3 | |

| 07:30 | EUR | Germany Manufacturing PMI May P | 64 | 65.8 | 66.2 | |

| 07:30 | EUR | Germany Services PMI May P | 52.8 | 52 | 49.9 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May P | 62.8 | 62.4 | 62.9 | |

| 08:00 | EUR | Eurozone Services PMI May P | 55.1 | 52 | 50.5 | |

| 08:30 | GBP | Manufacturing PMI May P | 66.1 | 60 | 60.9 | |

| 08:30 | GBP | Services PMI May P | 61.8 | 62 | 61 | |

| 12:30 | CAD | Retail Sales M/M Mar | 3.60% | 2.30% | 4.80% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Mar | 4.30% | 4.00% | 4.80% | |

| 13:45 | USD | Manufacturing PMI May P | 60.4 | 60.5 | ||

| 13:45 | USD | Services PMI May P | 64.6 | 64.7 | ||

| 14:00 | USD | Existing Home Sales M/M Apr | 6.08M | 6.01M | ||

| 14:00 | EUR | Eurozone Consumer Confidence May P | -6.8 | -8.1 |