As DOW hit another record with strong rise overnight, team risk-on is extending the lead over team risk-off in the currency markets. New Zealand Dollar is having a mild upper hand over Australian, Canadian and Sterling for now. But the Loonie is trying to catch up with rising oil price. On the other hand, after heavy selling Swiss Franc and Yen are still having no sign of recovery yet. Dollar and Euro are only better than the two weakest.

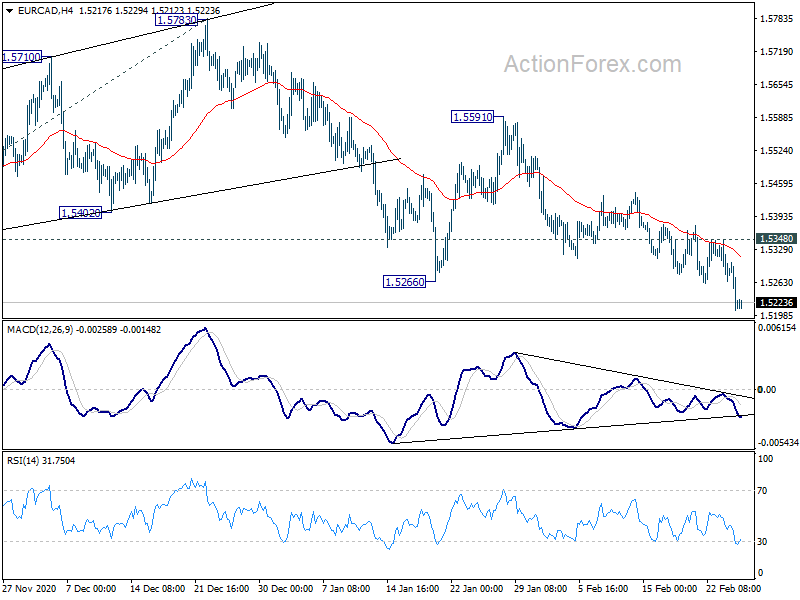

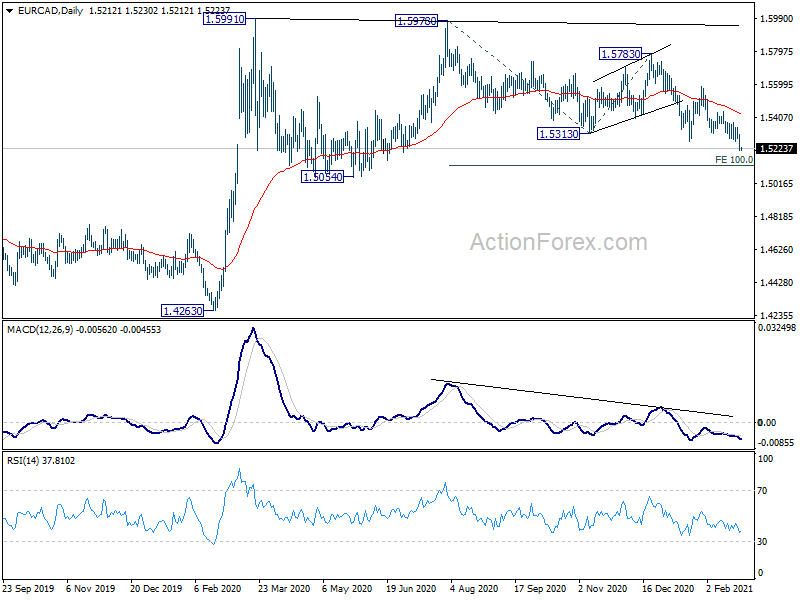

Technically, one development to note is that Canadian Dollar’s buying appears to be finally taking off. USD/CAD’s accelerating down, breaking 1.25 handle. It’s on track to 61.8% projection of 1.3389 to 1.2588 from 1.2880 at 1.2385. EUR/CAD is also accelerating downwards for 100% projection of 1.5978 to 1.5313 from 1.5783 at 1.5118.

In Asia, currently, Nikkei is up 1.53%. Hong Kong HSI is up 1.97%. China Shanghai SSE is up 0.93%. Singapore Strait Times is up 1.54%. Japan 10-year JGB yield is up 0.015 at 0.138. Overnight, DOW rose 1.35%. S&P 500 rose 1.14%. NASDAQ rose 0.99%. 10-year yield rose 0.027 to 1.389, after hitting as high as 1.435.

DOW hits new record on Fed Powell assurance, NASDAQ also rebounds

DOW surged to new record high overnight as markets took Fed Chair Jerome Powell’s message from the semiannual testimony clearly. That is, Fed is in no way near stimulus exit. The economy is “a long way” from Fed’s employment and inflation targets. He reiterated that Fed “will not tighten monetary policy solely in response to a strong labor market”. Additionally, Fed aims to “achieve inflation moderately above 2% for some time”.

DOW closed up 424.51 pts or 1.35% at 31961.86. Recent up trend has resumed with strong range breakout. For now, near term outlook will remain bullish as long as 31158.76 support holds. Up trend from 18213.65 should target 61.8% projection of 18213.65 to 29199.35 from 26143.77 at 32932.93.

NASDAQ also rose 132.7 pts or 0.99% to close at 13597.96. The rebound came after drawing support from 12985.05 earlier in the week. Note that NASDAQ has indeed led DOW in closing equivalent target at 14184.12 (61.8% projection of 6631.42 to 12074.06 from 10822.57 at 14186.12), earlier in the month. Hence, we might not see NASDAQ following DOW for a new high in the current move, and retake the lead. Let’s see.

Fed Clarida: Prospects have brightened and downside risks diminished

Fed Vice Chair Richard Clarida said in a speech, there have been some weaker than expected data in recent months. Services spending remained “well below pre-pandemic levels”. Improvement tin labor markets has “slowed notably”, with “true unemployment rate” closer to 10% level. Core PCE inflation was just running at 1.5%.

There were also some encouraging data as retail sales “stepped up considerably” in January. Housing sector has “more than fully recovered from the down turn”. Business investment and manufacturing production have “rebounded robustly”.

Overall, vaccine developments, and the new fiscal relief measures indicated that “the prospects for the economy in 2021 and beyond have brightened and the downside risk to the outlook has diminished.”

New Zealand ANZ business confidence dropped to 7, overshoot in demand dissipating

New Zealand ANZ Business Confidence dropped to 7.0 in February, down from December’s 9.4, and preliminary reading of 11.8. Confidence was highest in retails at at 15.6, followed by construction at 12.9, services at 10.8 and manufacturing at 3.6. Agriculture confidence was at -38.1.

Own Activity Outlook rose to 21.3, up from 21.7, vs prelim. 22.3. Activity was highest in construction at 41.9, followed by services at 24.7, retail at 13.3, manufacturing at 10.7 and agriculture at 0.

ANZ said, “overshoot in demand resulting from the disruptions of 2020 is beginning to dissipate, and we expect the economy to go broadly sideways for a while as it digests the national income hit from the decimated tourism industry and as the housing market cools to something more sustainable.”

From Australia, private capital expenditure rose 3.0% in Q4 versus expectation of 0.6%.

Looking ahead

Germany Gfk consumer confidence, Eurozone M3 money supply and confidence indicators will be featured in European session. Later in the day, US will releases Q4 GDP revision, jobless claims, durable goods orders and pending home sales.

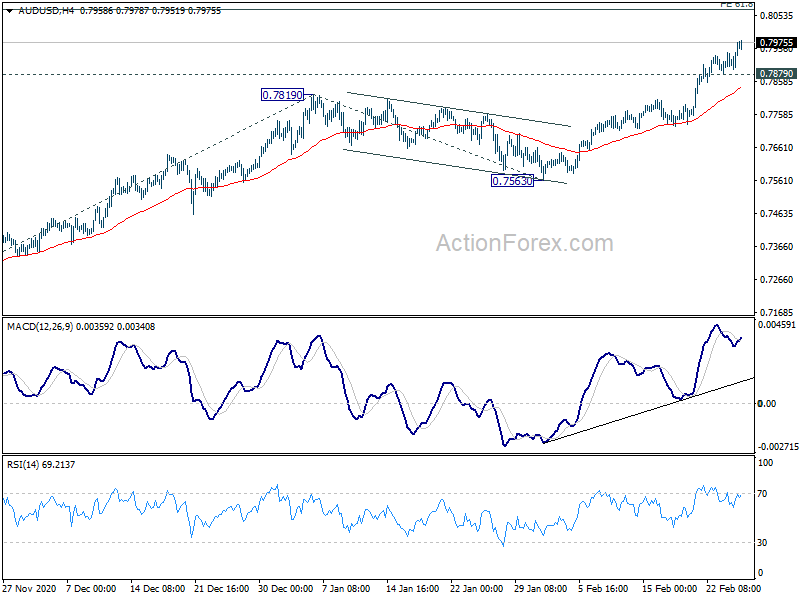

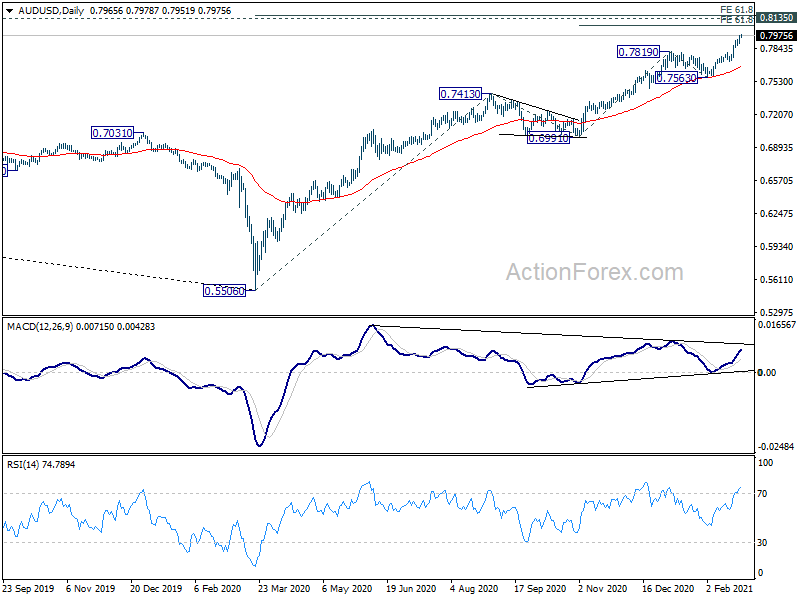

AUD/USD Daily Report

Daily Pivots: (S1) 0.7919; (P) 0.7946; (R1) 0.7997; More…

AUD/USD is regaining upside momentum and intraday bias stays on the upside. Current up trend from 0.5506 in on track to 61.8% projection of 0.6991 to 0.7819 from 0.7563 at 0.8075. We’d pay attention to the reaction to 0.8135 long term resistance. On the downside, break of 0.7879 minor support will turn intraday bias neutral and bring some consolidations first.

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | NZD | ANZ Business Confidence Feb F | 7 | 11.8 | 11.8 | |

| 0:30 | AUD | Private Capital Expenditure Q4 | 3.00% | 0.60% | -3.00% | |

| 7:00 | EUR | Germany Gfk Consumer Confidence Mar | -14 | -15.6 | ||

| 9:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 12.50% | 12.30% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Feb | 92.3 | 91.5 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Feb | -4.5 | -5.9 | ||

| 10:00 | EUR | Eurozone Business Climate Feb | -0.34 | -0.27 | ||

| 10:00 | EUR | Eurozone Services Sentiment Feb | -18.3 | -17.8 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -14.8 | -14.8 | ||

| 13:30 | USD | Initial Jobless Claims (Feb 19) | 820K | 861K | ||

| 13:30 | USD | GDP Annualized Q4 P | 4.10% | 4.00% | ||

| 13:30 | USD | GDP Price Index Q4 P | 2.00% | 2.00% | ||

| 13:30 | USD | Durable Goods Orders Jan | 1.10% | 0.50% | ||

| 13:30 | USD | Durable Goods Orders ex Transportation Jan | 0.70% | 1.10% | ||

| 15:00 | USD | Pending Home Sales M/M Jan | 0.20% | -0.30% | ||

| 15:30 | USD | Natural Gas Storage | -237B |