Sterling rises broadly today as UK Prime Minister Boris Johnson said he’s “hopeful” and “very optimistic ” to end pandemic restrictions on June 21, based on the “one-way road to freedom” roadmap unveiled yesterday. Canadian Dollar is Dollar is following as second strongest, with a little help from oil prices. Swiss Franc and Yen are currently the weakest for today, feeling the pressure from persistent strength in yield. Dollar’s decline slowed mildly, as markets await Fed Chair Jerome Powell’s testimony, with some attention on his comments on inflation and surging yields.

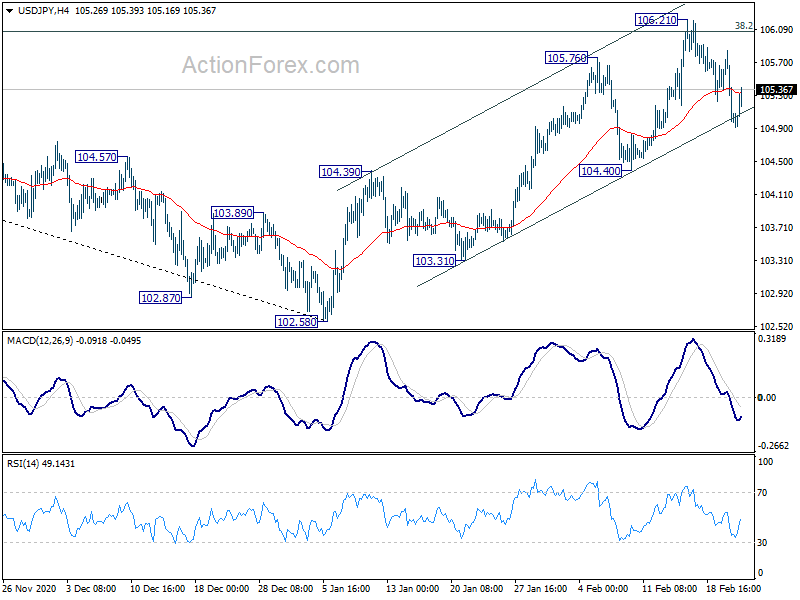

Technically, after breaching near term channel briefly, USD/JPY bends up wards and is now back above 105 handle. The pair’s reaction to Powell could help gauge the next move in reaction to Powell. In particular, a break of 104.40 support would confirm near term bearish reversal in USD/JPY and add to selling pressure elsewhere.

In Europe, currently, FTSE is down -0.07%. DAX is down -0.95%. CAC is up 0.03%. Germany 10-year yield is up 0.037 at -0.299. Earlier in Asia, Hong Kong HSI rose 1.03%. China Shanghai SSE dropped -0.17%. Singapore Strait Times rose 0.33%. Japan was on holiday.

Eurozone CPI finalized at 0.9% yoy, EU at 1.2% yoy

Eurozone CPI was finalized at 0.9% yoy in January, up from December’s -0.3% yoy. The highest contribution came from services (+0.65%), followed by non-energy industrial goods (+0.37%), food, alcohol & tobacco (+0.30%) and energy (-0.41%).

EU CPI was finalized at 1.2% yoy, up from 0.3% yoy. The lowest annual rates were registered in Greece (-2.4%), Slovenia (-0.9%) and Cyprus (-0.8%). The highest annual rates were recorded in Poland (3.6%), Hungary (2.9%) and Czechia (2.2%). Compared with December, annual inflation fell in three Member States, remained stable in six and rose in eighteen.

From Swiss: PPI came in at 0.3% mom, -2.1% yoy in January, versus expectation of 0.1% mom, -2.7% yoy.

UK claimant count dropped -20k Jan, unemployment edged up to 5.1 in Dec

UK claimant count dropped -20k in January, versus expectation of 35k rise. Total claimant count was relatively unchanged at 2.6m, which was still 109.4% above March 2020’s level.

Unemployment rate edged up to 5.1% in the three months to December, up from 5.0%, matched expectations. Total actually weekly hours worked rose 53.7 million hours, or 5.8%, to 978.7 million. Average earnings excluding bonus rose 4.1% 3moy, above expectation of 4.0%. Average earnings including bonus rose 4.7% 3moy, above expectation of 4.2% 3moy.

Australia goods exports dropped -9% mom in Jan, imports down -10% mom

Australia exports of goods dropped -9% mom to AUD 32.1B in January. The decline was led by 10% mom fall in export of metalliferous ores. Imports of goods also dropped -10% mom to AUD 23.4B, driven by -23% mom fall in road vehicles imports. Trades surplus narrowed slightly to AUD 8.75B, down from AUD 9.18B.

“The decline in metalliferous ores was driven by a decline in the quantity of iron ore exported in January. Despite the decline, exports of Metalliferous ores are the second highest on record behind December 2020,” Head of International Statistics at the ABS, Andrew Tomadini said. “A drop in global car manufacturing is leading to supply shortages, with the imports of road vehicles from Japan and Thailand, Australia’s two largest road vehicle source countries, driving the decline in January imports”.

New Zealand retail sales dropped -2.7% qoq in Q4

New Zealand retail sales dropped -2.7% qoq in Q4, below expectation of -0.5% qoq. Ex-auto sales dropped -3.1% qoq, versus expectation of -0.6% qoq. That same after strong rebound of 27.8% qoq in retail sales in Q3.

Nevertheless, comparing to Q4 2019, total value of retail sales rose 4.9% yoy. Total volume of sales rose 4.8% yoy. 13 of the 16 regions showed higher sales values.

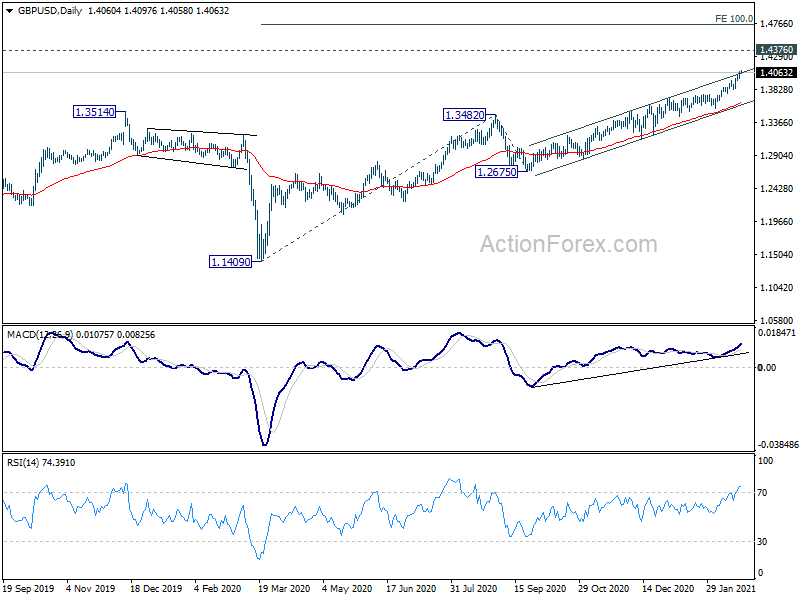

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3999; (P) 1.4043; (R1) 1.4104; More….

Intraday bias in GBP/USD remains on the upside at this point. Current rally is part of the up trend from 1.1409. Next target is 1.4376 long term resistance next. On the downside, break of 1.3979 minor support will turn intraday bias neutral, and bring consolidations, before staging another rally.

In the bigger picture, rise from 1.1409 medium term bottom is in progress. Further rally would be seen to 1.4376 resistance and above. Decisive break there will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. On the downside, break of 1.3482 resistance turned support is needed to be first indication of completion of the rise. Otherwise, outlook will stay cautiously bullish even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q4 | -2.70% | -0.50% | 28.00% | 27.80% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | -3.10% | -0.60% | 24.10% | 23.90% |

| 7:00 | GBP | Claimant Count Change Jan | -20K | 35K | 7K | |

| 7:00 | GBP | Claimant Count Rate Jan | 7.20% | 7.40% | 7.30% | |

| 7:00 | GBP | ILO Unemployment Rate (3M) Dec | 5.10% | 5.10% | 5.00% | |

| 7:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | 4.10% | 4.00% | 3.60% | |

| 7:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | 4.70% | 4.20% | 3.60% | 3.70% |

| 7:30 | CHF | Producer and Import Prices M/M Jan | 0.30% | 0.10% | 0.50% | |

| 7:30 | CHF | Producer and Import Prices Y/Y Jan | -2.10% | -2.70% | -2.30% | |

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 0.90% | 0.90% | 0.90% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 1.40% | 1.40% | 1.40% | |

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Dec | 8.60% | 9.10% | ||

| 14:00 | USD | Housing Price Index M/M Dec | 1.00% | 1.00% | ||

| 15:00 | USD | Consumer Confidence Feb | 90.2 | 89.3 |