Sterling is heavily sold off today as risk of no-deal Brexit is increasing with no major breakthrough in the never-ending negotiations. It’s even unsure if talks will be concluded today, or continues till Wednesday. An European Commission spokesman even refused to “speculate on a last chance date” for the negotiations. Australian Dollar is following as the second weakest as China’s blame on Australia as a possible original of the coronavirus heightens tensions further. Swiss Franc is currently the strongest one followed by Euro and Yen. Dollar is mixed for now.

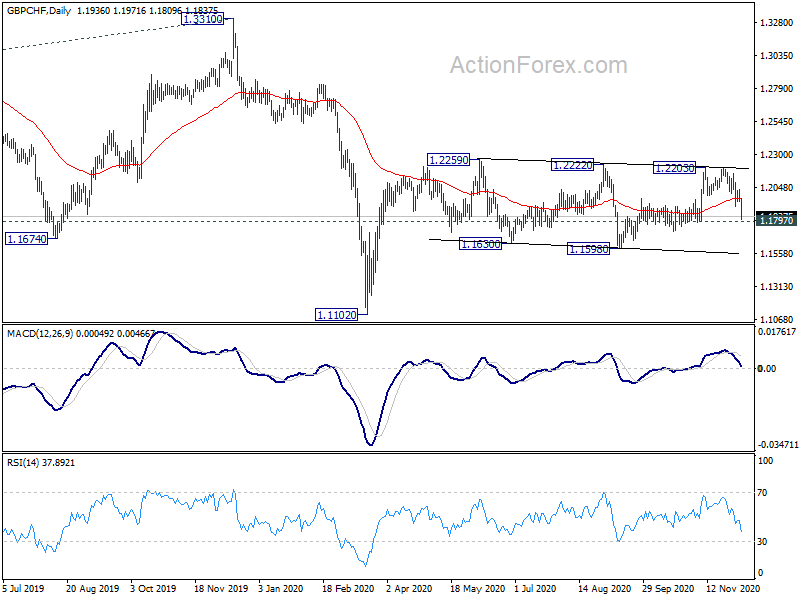

Technically, GBP/CHF and EUR/CHF should be watched in the coming days on market reactions to the Brexit talks. As for GBP/CHF, break of 1.1797 support could prompt downside acceleration towards the lower end of the medium term range at 1.1598. On the other hand, firm break of 1.1079 support in EUR/CHF would extend the consolidation pattern form 1.0915 with another falling leg towards 1.0661 support. Both would mean risk aversion on the European side.

In Europe, currently, FTSE is up 0.23%. DAX is down -0.37%. CAC is down -0.80%. German 10-year yield is down -0.0348 at -0.578. Earlier in Asia, Nikkei dropped -0.76%. Hong Kong HSI dropped -1.23%. China Shanghai SSE dropped -0.81%. Singapore Strait Times dropped -0.51%. Japan 10-year JGB yield dropped -0.0010 to 0.026.

Eurozone Sentix rose to -2.7, vaccines boost many expectations indices to record highs

Eurozone Sentix Investor Confidence improved to -2.7 in December, up from -10.0, much better than expectation of -11.9. That’s also the highest level since February. Current situation rose from -32.3 to -30.3, highest since March. Expectation index jumped from 15.3 to 29.3, highest since April, 2015.

Sentix noted: “The Corona crisis year 2020 will end with a bang, which will set several exclamation marks for the global economy. In our December results, we have a series of all-time highs (!) in the expectation components of various world economic regions. Hopes for an early use of vaccines are fuelling the fantasy that the economy in 2021 will recover more clearly than previously expected from the consensus.”

- Germany’s overall index rose from 1.3 to 6.9, highest since May 2019. Current situation rose slightly from -17.5 to -17.3, highest since March. Expectations rose from 22.0 to 34.3, an all time high.

- US overall index rose from 4.8 to 9.1, highest since February. Current situation dropped from -10.5 to -11.8. Expectations rose from 21.3 to 32.3, an all time high.

- Japan overall index rose from 6.1 to 14.5, highest since October 2018. Current situation rose from -8.3 to -2.3, highest since Feb. Expectations rose from 31.5 to 32.8, an all time high.

Germany industrial production rose 3.2% in Oct, but Ifo said expectations deteriorated

Germany industrial production rose 3.2% mom in October, above expectation of 1.8% mom. Production was down -3.0% yoy on the same month a year ago. Compared with February, before coronavirus restrictions, production was down -4.9%.

However, separately released, Ifo said the industrial production expectations for the coming months have deteriorated, falling to 5.5 pts in November. “The consumer-oriented industries in particular are catching their breath, while the pharma industry is seeing a surge,” says ifo expert Klaus Wohlrabe.

Also released, Swiss foreign currency reserves rose to CHF 876B in November.

China’s export rose 21.1% yoy in Nov, imports rose 4.5%, trade surplus at USD 75.4B

In November, in USD term, China’s export rose 21.1% yoy to USD 268.1B. Imports rose 4.5% yoy to USD 192.7B. Trade surplus came in at USD 75.4B, up from October’s USD 58.4B, above expectation of USD 53.8B. Year-to-date, exports rose only 2.5% yoy while imports dropped -1.6% yoy. Year-to-date trade surplus was at USD 460B.

- Year-to-date, total trade with EU rose 3.5% yoy to USD 581B. Exports rose 5.7% yoy to USD 351B. Imports rose 0.2% yoy to USD 231B. Trade surplus was at USD 120B.

- Year-to-date, total trade with US rose 5.8% yoy to USD 524B. Exports rose 5.7% yoy to USD 406B. Imports rose 6.1% yoy to USD 118B. Trade surplus was at USD 288B

- Year-to-date, total trade with Australia dropped -0.9% to USD 153B. Exports rose 9.4% yoy to USD 48B. Imports dropped -4.9% yoy to USD 105B. Trade deficits was at USD -57B.

Australia AiG services rose to 52.9, but new orders slowed

Australia AiG Performance of Services Index rose 1.5 pts to 52.9 in November, highest since November 2019. Looking at some details, sales rose 5.1 pts to 54.7. Employment rose 3.3 to 56.4. But new orders dropped -1.0 to 51.9. Growth was seen in four sectors while retail trade and hospitality was the only sector that continued to contract.

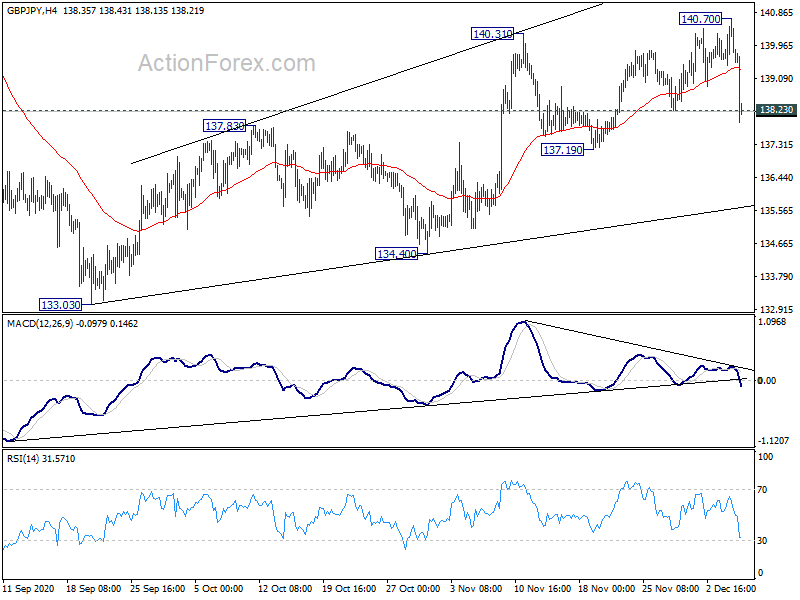

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.41; (P) 140.06; (R1) 140.63; More…

GBP/JPY’s break of 138.23 support argues that corrective rise from 133.03 has completed, on bearish divergence condition in 4 hour MACD. The pattern from 142.71 might be starting another falling leg. Intraday bias is back on the downside for 137.19 support first. Firm break there will add more credence to this bearish case and target 133.03/134.40 support zone. This will remain the favored case as long as 140.70 resistance holds, in case of recovery.

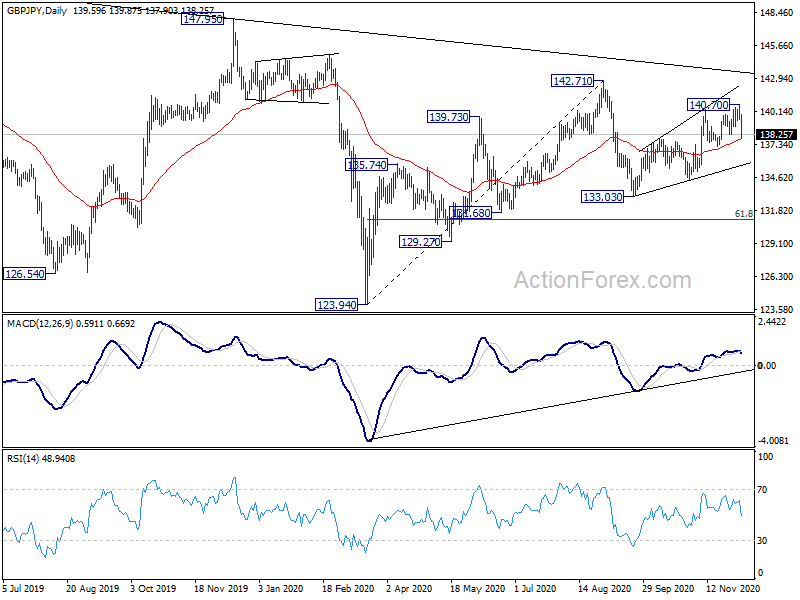

In the bigger picture, rise from 123.94 is seen as a rising leg of the sideway consolidation pattern from 122.75 (2016 low). As long as 147.95 resistance holds, an eventual downside breakout remains in favor. However, firm break of 147.95 will raise the chance of long term bullish reversal. Focus will then be turned to 156.59 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Nov | 52.9 | 51.4 | ||

| 2:00 | CNY | Trade Balance (CNY) Nov | 507B | 373B | 402B | |

| 2:00 | CNY | Exports (CNY) Y/Y Nov | 14.90% | 7.60% | ||

| 2:00 | CNY | Imports (CNY) Y/Y Nov | -0.80% | 0.90% | ||

| 2:00 | CNY | Trade Balance (USD) Nov | 75.4B | 53.8B | 58.4B | |

| 2:00 | CNY | Exports (USD) Y/Y Nov | 21.10% | 11.40% | ||

| 2:00 | CNY | Imports (USD) Y/Y Nov | 4.50% | 4.70% | ||

| 5:00 | JPY | Leading Economic Index Oct P | 93.80% | 93.40% | 92.50% | |

| 7:00 | EUR | Germany Industrial Production M/M Oct | 3.20% | 1.80% | 1.60% | |

| 8:00 | CHF | Foreign Currency Reserves (CHF) Nov | 876B | 871B | 872B | |

| 9:30 | EUR | Eurozone Sentix Investor Confidence Dec | -2.7 | -11.9 | -10 | |

| 15:00 | CAD | Ivey PMI Nov | 54.5 |