Movements in the forex markets remain relatively limited and indecisive. There were little reaction to the steep decline in US stocks overnight, which is followed by broad based weakness in Asia. For now, Dollar, Yen and Kiwi are the firmer ones for the week. Canadian Dollar remains the worst performing as dragged down by oil prices. Euro and Swiss Franc are following. Still, most major pairs and crosses are stuck inside last week’s range, with exception of a few Loonie pairs.

Technically, Dollar’s rebound attempt is rather unconvincing for now. EUR/USD and GBP/USD are holding around 4 hour 55 EMAs which provide the support. USD/CHF and USD/JPY are holding below the same EMAs which provide resistance. USD/CAD is the larger mover but it’s limited well below 1.3259 resistance so far. Nevertheless, as stocks could be preparing itself for an extended near term selloff, we could see Dollar picking up more momentum. Let’s see.

In Asia, currently, Nikkei is down -0.38%. Hong Kong HSI is down -1.16%. China Shanghai SSE is down -0.37%. Singapore Strait Times is down -0.65%. Japan 10-year JGB yield is down -0.0040 at 0.031. Overnight, DOW dropped -2.29%. S&P 500 dropped -1.86%. NASDAQ dropped -1.64%. 10-year yield dropped -0.040 to 0.801, barely holding on to 0.8 handle.

– advertisement –

DOW lost -650 pts on triple whammy of stimulus, coronavirus and elections

US stocks were knocked down by triple whammy of stalled stimulus talks, record coronavirus infections, and election uncertainties. Traders are clearly reducing risk exposures. DOW closed down -650 pts, or -2.29%, at 27685.38. The break of 55 day EMA should now confirm rejection by 29199.35 resistance on the prior up move. Corrective pattern from 29199.35 should have started the third leg. Deeper fall is likely towards 26537.01 support for the near term. That might happen even by the end of the week if selling intensifies.

Break of 26537.01 could complete a double top reversal pattern. But we believe the key support lies in cluster at 24971.03, which is close to 25000 psychological level, and more importantly 38.2% retracement of 18213.65 to 29199.35 at 25002.81. This level is not expected to be tested before the result of the election is cleared. It’s more of an indication of overall reactions to the results. So, watch out… next week.

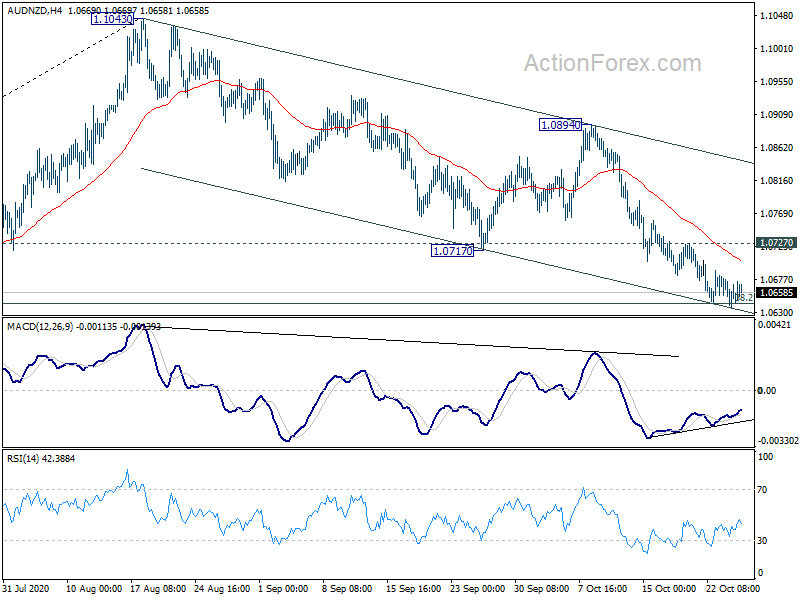

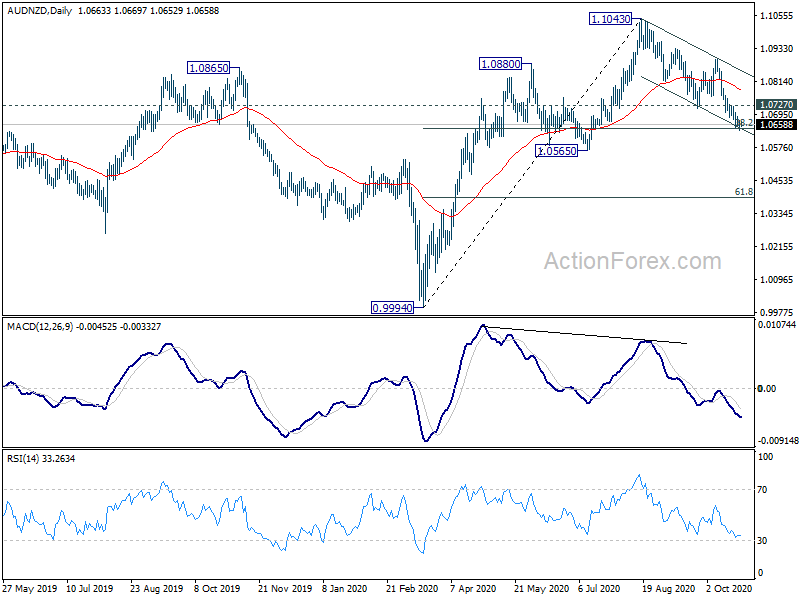

AUD/NZD hits correction target, takes a breather before next move

AUD/NZD could be an interesting cross to note in the upcoming two weeks. Risk markets are now preparing for the next move after US election. The development in the cross would provide the guidance on which currency to move “faster” next. Additionally, how RBA is going to fulfil market expectations of easing on November 3, also next week, would be another factor.

The corrective fall from 1.1043 has hit target of 38.2% retracement of 0.9994 to 1.1043 at 1.0642. Downside momentum is diminishing as seen in 4 hour MACD, and we’d not anticipate any reacceleration for now. Sustained break of 1.0565 key support would indicate completion of the whole three-wave rebound from 0.9994 to 1.1043. That will open up deeper fall back to 61.8% retracement at 1.0395 and below. Nevertheless, break of 1.0727 will be the first sign of bottoming and will retain near term bullishness, with a retest on 1.1043 resistance in the cards.

New Zealand trade deficit widened to NZD -1B in Sep

New Zealand goods exports dropped NZD -350m, or -8.0% yoy to NZD 4.0B in September. Goods imports also dropped NZD -643m, or -11.0% yoy, to NZD 5.0B. Trade deficit came in at NZD -1017m, narrowed from August’s NZD -282m, largely inline with expectations. Imports from all top trading partners decline, including China, EU, Australia, US and Japan. Exports to all top trading partners also declined, except to US.

For the quarter, exports rose 0.7% qoq to NZD 14.8B in Q3. Imports rose 3.3% qoq to NZD 13.6B. Trade balance for Q3 was a surplus of NZD 1.2B.

Looking ahead

Eurozone M3 and UK CBI realized sales will be released in European session. But focuses will be mainly on US data, including durable goods orders, house price indices and consumer confidence.

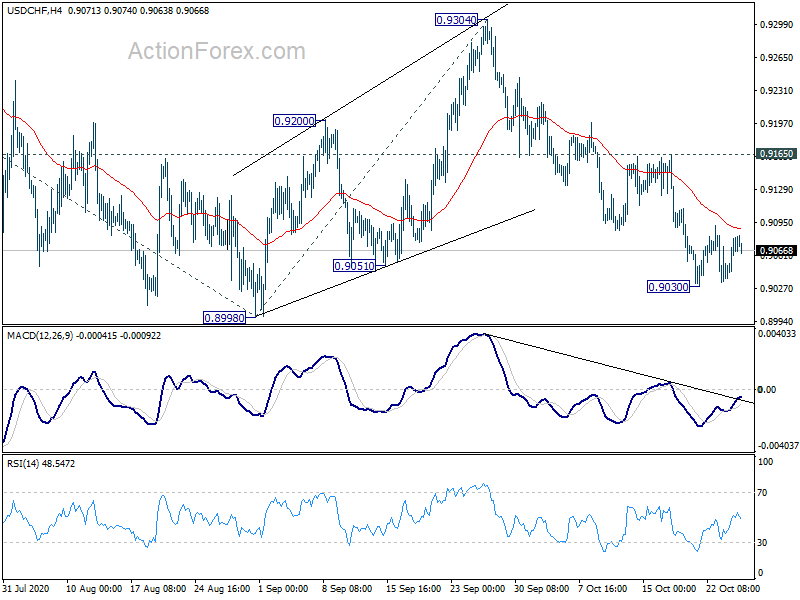

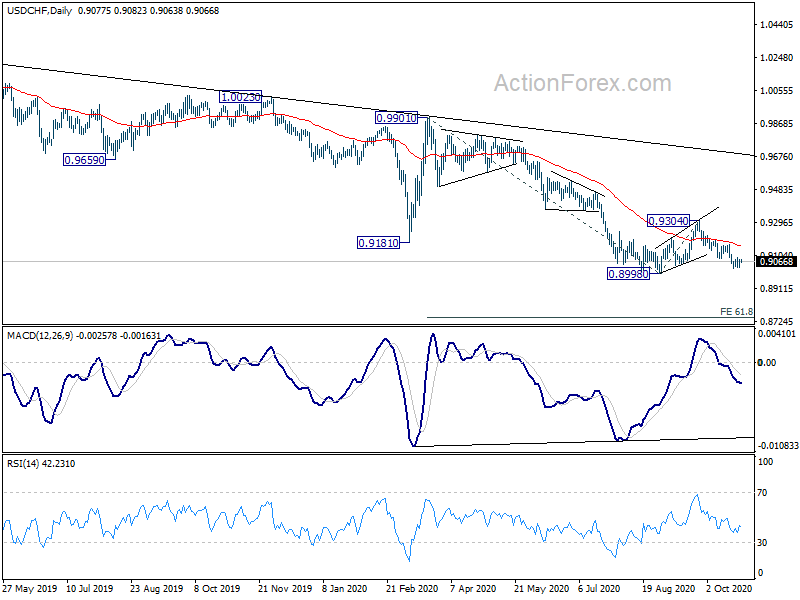

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9052; (P) 0.9066; (R1) 0.9093; More…

USD/CHF is staying in consolidation form 0.9030 temporary low. Intraday bias remains neutral first. In case of another recovery, upside should be limited below 0.9165 resistance. On the downside, break of 0.9030 will target 0.8998 low first. Firm break there will resume larger down trend to 61.8% projection of 0.9901 to 0.8998 from 0.9304 at 0.8746. However, break of 0.9165 will invalidate this bearish view and turn bias back to the upside for 0.9304 resistance.

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 high). There is no clear sign of completion yet. On resumption, next target will be 138.2% projection of 1.0342 to 0.9186 from 1.0237 at 0.8639. Nevertheless, strong break of 0.9304 resistance will be an early sign of trend reversal and turn focus back to 0.9901 key resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -1017M | -1015M | -353M | -282M |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | 9.60% | 9.50% | ||

| 11:00 | GBP | CBI Realized Sales Oct | -2 | 11 | ||

| 12:30 | USD | Durable Goods Orders Sep | 1.10% | 0.50% | ||

| 12:30 | USD | Durable Goods Orders ex Transport Sep | 0.40% | 0.60% | ||

| 13:00 | USD | S&P/CS Composite-20 Y/Y Aug | 3.80% | 3.90% | ||

| 13:00 | USD | Housing Price Index M/M Aug | 0.60% | 1.00% | ||

| 14:00 | USD | Consumer Confidence Oct | 101.9 | 101.8 |